Global food commodity prices edged lower for a second consecutive month in June, offering limited relief after the benchmark climbed to a three-year high earlier in 2026.

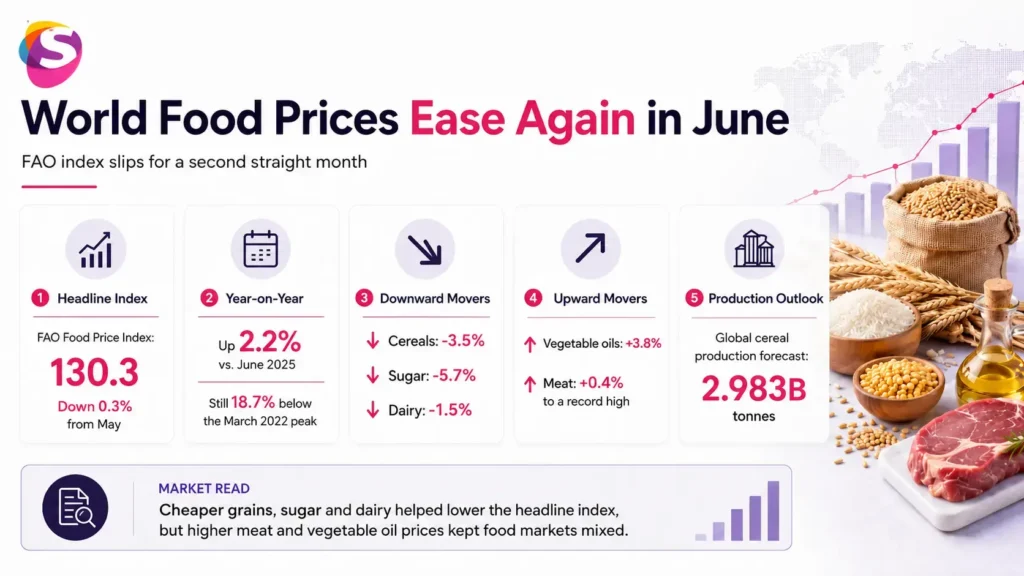

The FAO Food Price Index averaged 130.3 points, down 0.3% from May, as falling cereal, sugar and dairy prices outweighed higher vegetable oil and meat costs. The index remained 2.2% above its level a year earlier but was still 18.7% below the record reached in March 2022.

The latest global food price data reveal a sharply divided market. Wheat and maize prices fell as harvests advanced and supply expectations improved, while meat prices reached a new record and vegetable oils rebounded.

Key Overview

- Food Price Index: 130.3 points in June.

- Monthly change: Down 0.3%.

- Annual change: Up 2.2%.

- Cereals: Down 3.5%.

- Sugar: Down 5.7%.

- Dairy: Down 1.5%.

- Vegetable oils: Up 3.8%.

- Meat: Up 0.4% to a record high.

- 2026 cereal forecast: 2.983 billion tonnes.

Grain Prices Lead the Global Decline

Cereals provided the strongest downward pressure on the overall food index.

The cereal price benchmark fell 3.5% from May as both wheat and maize quotations weakened. World wheat prices declined 4.4%, helped by rapid harvesting and strong supply prospects in the Black Sea region.

The decline came despite concerns over weaker production prospects in Australia and the United States. A stronger U.S. dollar and softer energy prices also added downward pressure.

Maize prices fell even faster, dropping 6.2% as South American supply prospects improved. Lower crude oil prices also reduced support from biofuel demand.

Rice moved in the opposite direction. The global rice index rose 3.2% as demand for Indica varieties strengthened in Asia and higher transport and production costs supported prices.

The mixed performance highlights the growing importance of regional supply conditions. Strong wheat and maize harvest prospects are easing pressure in major markets, while individual crops remain exposed to demand shifts and weather risks.

Sugar Falls as Brazil Shifts More Cane to Production

Sugar recorded the largest monthly decline among the major food categories.

Prices fell 5.7% as lower ethanol prices in Brazil encouraged mills to allocate more sugarcane to sugar production rather than fuel.

A weaker Brazilian real also supported strong exports, adding more supply to the international market.

However, the decline was partly restrained by concerns over El Niño. The weather pattern could affect output in major producers such as India and Thailand during the 2026/27 season.

The sugar market therefore reflects a wider tension across agricultural commodities: current supplies are helping to lower prices, but future production remains vulnerable to changing weather conditions.

Meat Prices Hit a New Record

While several major food categories became cheaper, meat prices continued to rise.

The meat price index increased 0.4% in June to a new record high, driven mainly by poultry.

International poultry quotations rose amid strong global import demand and tighter domestic availability following earlier production adjustments.

Ovine meat prices also increased, while pig and bovine meat prices declined.

The record illustrates why a falling headline food index does not necessarily mean lower costs across all food categories. Consumers and importers remain exposed to very different price pressures depending on the commodity.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Vegetable Oils Rebound on Biofuel Demand

Vegetable oil prices rose 3.8% after declining in May.

The increase was driven by palm and rapeseed oil, while sunflower oil prices remained broadly stable and soyoil weakened.

Palm oil prices were supported by expectations of tighter exports from Indonesia as domestic biodiesel demand absorbed more feedstock.

Rapeseed oil prices also climbed because of strong biofuel demand and unfavourable weather affecting planting conditions in Australia and Canada.

The rebound shows how energy markets remain closely linked to food prices. When demand for biofuels strengthens, edible oils can become more valuable as industrial feedstocks, tightening supply available for food markets.

Global Cereal Harvest Still Near Historic Highs

Despite weather concerns, global cereal supplies remain relatively strong.

The latest cereal supply forecast puts 2026 production at 2.983 billion tonnes. That would be 1.9% below the record set in 2025 but still the second-largest harvest in history.

Coarse grain production is expected to remain close to last year’s level, supported by stronger maize prospects in Argentina, Brazil, China and Zambia.

Wheat output is forecast to fall 4.3% to 806.5 million tonnes, partly because of weaker prospects in Australia.

Rice production is also expected to decline 1.8% from the previous season’s record.

Even so, global cereal stocks are projected at 957.8 million tonnes by the end of the 2026/27 seasons, leaving the stock-to-use ratio broadly stable at 32%.

El Niño Remains the Main Threat

The decline in June prices does not remove the risks facing global food markets.

El Niño could bring drier conditions to major agricultural regions and disrupt production in crops ranging from wheat to sugar.

At the same time, geopolitical tensions, currency movements, energy prices and biofuel policies continue to influence international food costs.

For now, strong harvest progress and ample supplies are keeping the overall market relatively stable.

But the June figures show that the global food picture is far from uniform. Cheaper grains and sugar are pulling the headline index down, while record meat costs and rising vegetable oil prices continue to put pressure on specific parts of the food system.

Sources: FAO / Reuters

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}