The latest RBI fixed deposit rules proposals could significantly change how banks price large deposits while improving transparency for depositors. The Reserve Bank of India’s draft amendments would allow banks greater flexibility to offer differentiated rates on bulk deposits based on liquidity needs, while introducing more consistent disclosure requirements across the banking sector.

Key Overview

- The Reserve Bank of India has released draft amendments relating to fixed deposits and bulk deposits.

- Public feedback on the proposals is open until June 20, 2026.

- Banks may be allowed to offer different rates on bulk deposits depending on liquidity and funding needs.

- The proposed framework is linked to the Liquidity Coverage Ratio (LCR) requirements.

- The changes would apply to domestic rupee and non-resident rupee bulk deposits.

- The RBI aims to improve transparency and consistency in deposit rate disclosures.

- Scheduled banks currently offer FD rates ranging from 2.50% to 8.10%.

- Small finance banks continue to provide the highest fixed deposit returns.

- Public sector banks generally offer rates between 6.45% and 6.75%.

- Major private banks typically offer rates ranging from 6.45% to 6.80%.

RBI FD Interest Rate Rules Could Increase Competition for Deposits

The proposed RBI FD interest rate rules could bring significant changes to India’s deposit market by giving banks greater flexibility in pricing large deposits while enhancing transparency for depositors.

The Reserve Bank of India recently released draft amendment directions that would allow banks to offer different interest rates on bulk deposits depending on their liquidity and funding requirements. At the same time, the proposals seek to establish greater consistency in how deposit rates are disclosed to customers.

Although the primary focus is on large depositors, industry observers believe the changes could have wider implications for the broader fixed deposit market over time.

The draft proposals are currently open for public consultation until June 20, 2026, after which the RBI will decide whether and how the amendments will be implemented.

RBI Fixed Deposit Rules Focus on Greater Flexibility

The proposed RBI fixed deposit rules aim to provide banks with more freedom in managing their funding strategies.

Under the draft amendments, banks would be allowed to offer differentiated interest rates on bulk deposits based on applicable run-off rates under the Liquidity Coverage Ratio framework.

The RBI stated that banks should have the flexibility to determine deposit pricing according to their individual liquidity requirements and funding conditions.

This represents a shift from a more uniform approach toward one that allows institutions to respond more effectively to changing market circumstances.

The regulator believes this flexibility could improve liquidity management while helping banks attract deposits more efficiently when needed.

The proposal would apply to both domestic rupee bulk deposits and non-resident rupee bulk deposits.

Bulk Deposit Rates May Become More Dynamic

One of the most significant aspects of the proposals involves bulk deposit rates.

Bulk deposits typically represent large-value deposits made by corporations, institutions, and high-net-worth customers. Because these deposits can have a substantial impact on bank liquidity positions, banks often manage them differently from retail deposits.

The RBI’s proposed framework would allow institutions to offer different rates based on factors such as liquidity requirements and funding objectives.

As a result, interest rates on large deposits may become more dynamic and responsive to market conditions.

Banks experiencing stronger funding needs may choose to offer more attractive rates, while institutions with ample liquidity could maintain lower pricing.

This increased flexibility could intensify competition among banks seeking to attract large depositors.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

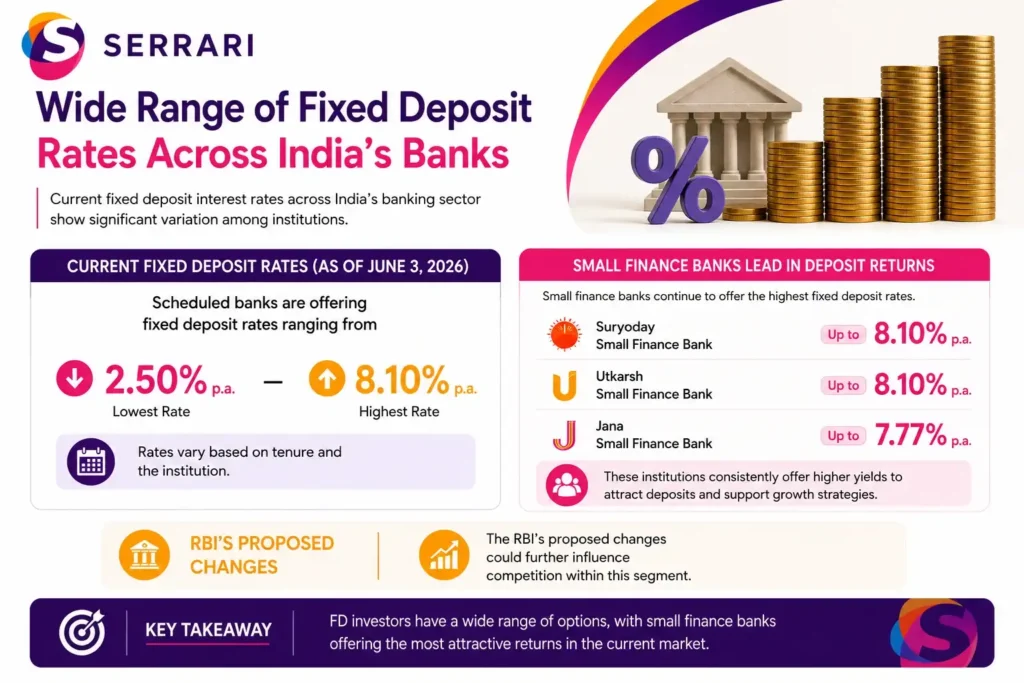

Fixed Deposit Interest Rates Remain Competitive

Current fixed deposit interest rates across India’s banking sector already reflect considerable variation among institutions.

As of June 3, 2026, scheduled banks were offering fixed deposit rates ranging from approximately 2.50% to 8.10% annually, depending on tenure and institution.

Small finance banks continue to lead the market in terms of deposit returns.

Suryoday Small Finance Bank and Utkarsh Small Finance Bank currently offer rates of up to 8.10%, while Jana Small Finance Bank provides rates reaching 7.77%.

These institutions have consistently offered higher yields to attract deposits and support growth strategies.

The RBI’s proposed changes could further influence competition within this segment.

Bank Deposit Rates India Show Significant Variation

The latest bank deposit rates India data highlights substantial differences between institutions.

Among private-sector lenders, banks such as IDFC FIRST Bank, Bandhan Bank, DCB Bank, Yes Bank, CSB Bank, RBL Bank, and Tamilnad Mercantile Bank currently offer rates exceeding 7% on selected deposit tenures.

In contrast, larger public sector banks generally provide lower rates.

State Bank of India, Bank of Baroda, Punjab National Bank, and Canara Bank typically offer fixed deposit returns ranging between 6.45% and 6.75%.

Major private-sector institutions such as HDFC Bank, ICICI Bank, Axis Bank, and Kotak Mahindra Bank offer rates largely within the 6.45% to 6.80% range.

These differences demonstrate the importance of comparing deposit products before making investment decisions.

Indian Banking Regulations Seek Greater Transparency

Beyond pricing flexibility, the draft amendments also focus on strengthening transparency within Indian banking regulations.

The RBI stated that one of the key objectives of the proposals is to promote uniformity in the disclosure of deposit interest rates.

Clearer disclosure standards would make it easier for customers to compare products across institutions and understand the rates being offered.

Transparency plays an important role in ensuring efficient competition and informed decision-making within financial markets.

For depositors, improved disclosure practices could simplify the process of identifying attractive fixed deposit opportunities.

The initiative also aligns with broader regulatory efforts aimed at strengthening consumer protection and financial market transparency.

Term Deposit Rules Could Influence Future Competition

The proposed changes to term deposit rules may have broader implications for the banking industry.

By allowing greater flexibility in pricing bulk deposits, banks could become more active in competing for institutional and large-value funds.

This competition may indirectly influence retail deposit markets as institutions adjust overall funding strategies.

Some analysts believe the changes could encourage banks to develop more innovative deposit products and pricing structures.

Others suggest that stronger competition for deposits could ultimately benefit savers by supporting more attractive interest rates.

While the final impact will depend on how banks respond, the proposals represent a meaningful shift in deposit market regulation.

What It Means for Ordinary Savers

Although the proposed amendments primarily target large deposits, ordinary savers may also benefit over time.

Increased competition among banks could improve deposit pricing across various customer segments.

Greater transparency in rate disclosures would also make it easier for retail investors to compare products and identify the most competitive offerings.

As banks gain more flexibility in managing liquidity and funding, they may develop additional savings and fixed deposit products tailored to different customer needs.

While the immediate effects may be concentrated in the bulk deposit market, broader market dynamics could eventually influence retail deposit rates as well.

Conclusion

The proposed RBI FD interest rate rules represent an important step toward greater flexibility and transparency in India’s deposit market. By allowing banks to offer differentiated rates on bulk deposits while improving disclosure standards, the RBI aims to strengthen liquidity management and promote more efficient competition.

Although the changes are primarily designed for large deposits, they could ultimately benefit the broader banking sector and ordinary savers through enhanced competition and clearer information. As the consultation process continues through June 20, 2026, market participants will be closely watching how the final framework takes shape.

FAQs

1. What changes has the RBI proposed for fixed deposits?

The RBI has proposed allowing banks greater flexibility to offer different interest rates on bulk deposits based on their liquidity and funding requirements. The regulator also wants to improve transparency by introducing more uniform disclosure standards for deposit rates across the banking sector.

2. What are bulk deposits?

Bulk deposits are typically large-value deposits placed by institutions, corporations, or high-net-worth individuals. Because these deposits can significantly affect a bank’s liquidity position, they are often managed differently from regular retail deposits and may be subject to specialized pricing structures.

3. Will ordinary fixed deposit investors be affected?

While the proposals are primarily focused on bulk deposits, ordinary savers could benefit indirectly. Increased competition among banks and improved transparency may help depositors compare products more easily and potentially access more attractive fixed deposit rates over time.

4. Which banks currently offer the highest FD rates in India?

Small finance banks currently offer some of the highest fixed deposit returns. Suryoday Small Finance Bank and Utkarsh Small Finance Bank offer rates of up to 8.10%, while Jana Small Finance Bank offers rates reaching 7.77%, according to data available as of June 2026.

Sources: MSN, Times of India, Upstox

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}