FD rates India 2026 remain attractive for conservative savers, but rising inflation has reduced the visible purchasing-power cushion. A 6.50% fixed deposit gives a simple pre-tax spread of about 2.12 percentage points over June CPI inflation of 4.38%, while a 7.10% senior-citizen rate gives about 2.72 points. These are not exact real returns because they exclude tax, compounding, tenure, premature-withdrawal penalties and each household’s personal inflation basket. Investors should compare ordinary bank FDs, senior-citizen FDs, bulk deposits, non-callable deposits and higher-risk NBFC deposits before assuming the highest advertised rate is the best option.Caption: India’s fixed-deposit returns face renewed purchasing-power pressure after June CPI inflation rose above the RBI’s 4% target.

Key Overview

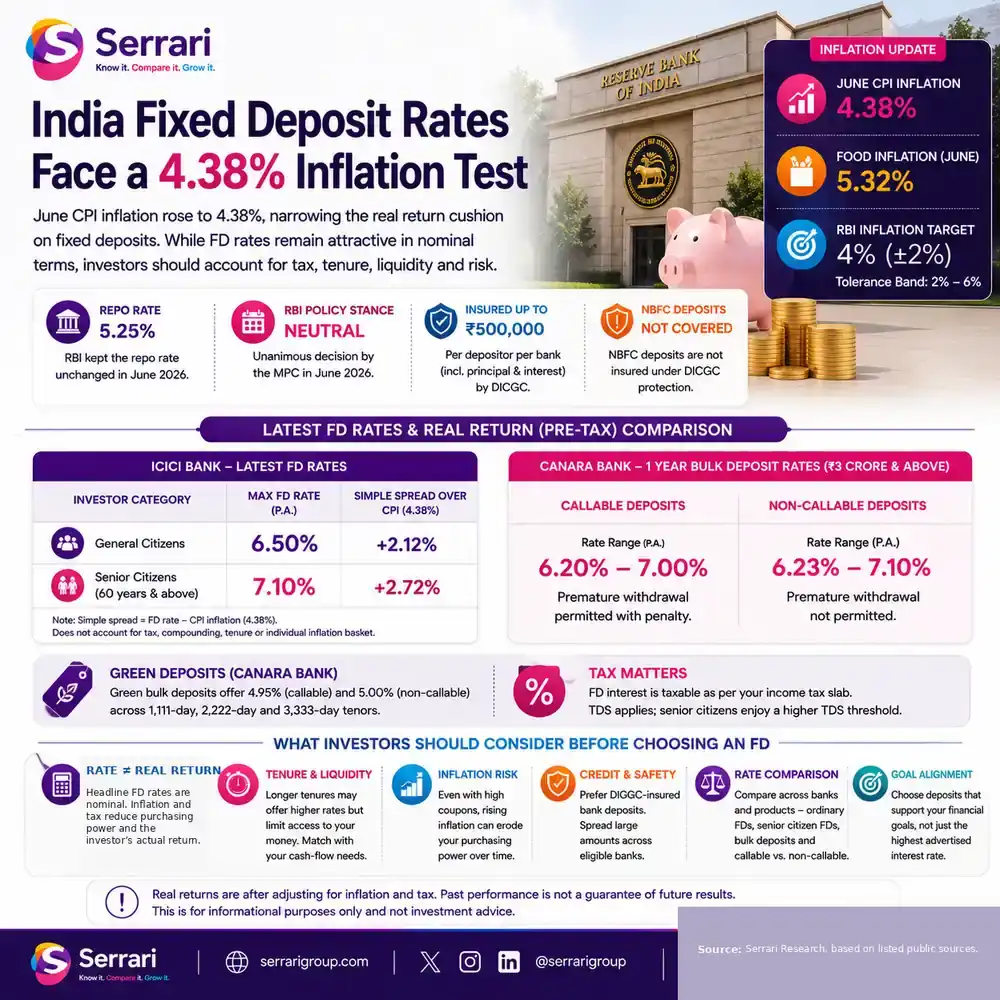

- India’s June CPI inflation rose to 4.38%, from 3.93% in May.

- June food inflation reached 5.32%.

- Inflation is above the RBI’s 4% target but still inside the 2%–6% tolerance band.

- RBI held the repo rate at 5.25% in its June 2026 monetary policy decision.

- ICICI Bank’s latest FD table offers up to 6.50% for general customers and 7.10% for senior citizens.

- DICGC insures eligible bank deposits up to ₹500,000 per depositor per bank, including principal and interest.

India Fixed Deposit Rates Face a 4.38% Inflation Test

Inflation Moves Above Target

The inflation backdrop has changed. MoSPI’s June CPI release shows year-on-year all-India CPI inflation at 4.38%, compared with 3.93% in May. Food inflation, measured by the Consumer Food Price Index, rose to 5.32%, with rural food inflation at 5.45% and urban food inflation at 5.09%.

This matters because fixed deposits are usually chosen for stability and predictable income. When inflation rises, the investor’s real purchasing-power return narrows. The deposit may still be safe in nominal rupee terms, but the goods and services that income can buy may grow more expensive.

The RBI Has Not Breached Its Band

The inflation reading is above the RBI’s 4% central target, but it has not breached the 6% upper tolerance level. RBI commentary confirms that the government renewed the 4% inflation target with a ±2% tolerance band through March 2031. That means the current inflation reading is uncomfortable for depositors, but it is still within the formal policy band. (Reserve Bank of India)

The RBI’s June policy decision also matters. The Monetary Policy Committee voted unanimously to keep the policy repo rate unchanged at 5.25% and retain a neutral stance. That means investors should not automatically assume that banks will raise FD rates immediately just because inflation moved above 4%. (Reserve Bank of India)

ICICI’s Latest Rates Show the Cushion

ICICI Bank’s latest FD page says senior citizens can earn up to 7.10% per annum, while general citizens can earn up to 6.50%. The bank also notes that FD interest payouts are subject to tax deducted at source under income-tax rules and that premature withdrawal may be paid at the rate applicable for the actual period held, after applicable penalties. (ICICI Bank)

Using the headline rates, a 6.50% deposit sits about 2.12 percentage points above June CPI inflation. A 7.10% senior-citizen deposit sits about 2.72 percentage points above CPI. But this is only a simple pre-tax comparison. A depositor in a higher tax bracket may see a much smaller after-tax cushion.

Canara Shows the Callable Trade-Off

Canara Bank’s revised bulk-deposit table, effective 13 July 2026, shows how product design changes the rate. For bulk callable deposits of ₹3 crore and above, the one-year rate ranges from 6.20% to 7.00%, depending on deposit size. For non-callable bulk deposits, one-year rates range from 6.23% to 7.10%. (Canara Bank)

That higher non-callable rate comes with a cost: liquidity. Canara states that non-callable term deposits are bulk deposits where premature withdrawal is not permitted. This is the classic fixed-income trade-off. Investors may earn a slightly better rate, but they give up access before maturity. (Canara Bank)

Green Deposits Are Not Yield Leaders

Canara’s table also shows that “green” labels do not automatically mean higher returns. Its bulk green deposits offer 4.95% for callable deposits and 5.00% for non-callable deposits across 1,111-day, 2,222-day and 3,333-day tenors. These rates are below the highest ordinary bulk-deposit rates in the same table. (Canara Bank)

This matters for investors comparing sustainability-linked or green-deposit products. The label may reflect the bank’s use of funds, but investors still need to compare rate, tenor, liquidity, tax and credit protection against ordinary deposits.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Deposit Insurance Has a Limit

DICGC deposit insurance is a key safety feature, but it has limits. DICGC says it insures deposits such as savings, fixed, current and recurring deposits, subject to exclusions. It also says each depositor in a bank is insured up to a maximum of ₹500,000 for both principal and interest held in the same right and same capacity. (dicgc.org.in)

This means a fixed deposit is not risk-free above the insured limit. It also means NBFC deposits should not be treated the same as insured bank deposits. DICGC’s guide says deposits mobilised by NBFCs are not covered under its deposit-insurance protection. (dicgc.org.in)

Tax Can Change the Answer

For many depositors, taxation is the real return test. ICICI’s FD page notes that interest earned on fixed deposits is taxable based on the investor’s income bracket, with TDS deducted when interest income crosses specified thresholds. (ICICI Bank)

This is why two investors can earn the same nominal FD rate but keep different after-tax returns. A retiree with lower taxable income may retain more of the coupon than a high-income depositor. Senior citizens may also benefit from higher advertised rates, but the after-tax outcome still depends on individual circumstances.

What Investors Should Compare

Investors should compare eight items before booking a fixed deposit: nominal rate, tenure, tax bracket, compounding frequency, payout option, premature-withdrawal penalty, DICGC coverage and whether the deposit is callable or non-callable.

They should also compare bank FDs with higher-risk NBFC deposits carefully. NBFC deposits may offer more attractive rates, but they do not carry the same DICGC protection as insured bank deposits. The extra return must compensate for the additional credit and liquidity risk.

What to Watch Next

The next RBI Monetary Policy Committee meeting is scheduled for 3–5 August 2026, and the July inflation release is expected in August. The key question is whether June’s inflation rise is temporary or the start of a more persistent move above the 4% target. RBI’s monetary-policy calendar lists the August MPC meeting dates, making that the next major policy checkpoint for savers. (Reserve Bank of India)

Economic Times has already framed the investor question around whether higher inflation could lead banks to increase FD rates, but the correct wording is possibility, not certainty. Bank deposit pricing depends on liquidity, credit demand, policy rates, competition and each bank’s balance-sheet needs. (The Economic Times)

Conclusion

India Fixed Deposit Rates still offer a visible nominal cushion over June inflation, especially for senior citizens. ICICI’s top general rate of 6.50% and senior-citizen rate of 7.10% remain above the 4.38% CPI print. But the cushion is narrower after tax, and food inflation at 5.32% may feel more relevant for many households than headline CPI.

For investors, the lesson is not to abandon fixed deposits. It is to compare the actual after-tax, after-penalty and inflation-adjusted outcome. Fixed deposits remain useful for capital stability and predictable income, but rising inflation makes product selection, tenor choice and tax planning much more important.

FAQs

1. What are India Fixed Deposit Rates right now?

India Fixed Deposit Rates vary by bank, tenure, customer category and deposit type. ICICI Bank’s updated FD page shows general customers earning up to 6.50% and senior citizens earning up to 7.10%. Canara Bank’s bulk-deposit table shows higher rates for some large deposits, but those are not directly comparable to ordinary retail FDs because they apply to bulk deposits and may differ by callable or non-callable structure.

2. How does June inflation affect FD investors?

June CPI inflation of 4.38% reduces the purchasing-power cushion from fixed deposits. A 6.50% FD gives a simple pre-tax spread of about 2.12 percentage points over inflation, while a 7.10% senior-citizen rate gives about 2.72 points. These figures are not exact real returns because they exclude taxes, compounding and household-specific inflation.

3. Will banks raise FD rates because inflation rose?

Not necessarily. Inflation above the RBI’s 4% central target may increase pressure on deposit pricing, but it does not guarantee higher FD rates. Banks consider repo-rate expectations, liquidity, loan demand, competition and funding needs before changing deposit rates. RBI also kept the repo rate unchanged at 5.25% in its June policy decision.

4. What is the DICGC deposit-insurance limit?

DICGC insures eligible bank deposits up to ₹500,000 per depositor per bank, including principal and interest held in the same right and same capacity. Covered deposits include fixed, savings, current and recurring deposits, subject to exclusions. Deposits above the limit create additional bank-credit exposure.

5. Are NBFC deposits the same as bank fixed deposits?

No. NBFC deposits and bank fixed deposits have different risk and protection profiles. DICGC’s guide states that NBFC deposits are not covered by deposit insurance. Investors comparing bank FDs and NBFC deposits should assess credit rating, issuer strength, liquidity, interest rate, tax and default risk before choosing a higher-yielding option.

Sources: MoSPI, Reserve Bank of India, ICICI Bank, Canara Bank, DICGC, Reserve Bank of India, The Economic Times

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}