Statutory payments are benefits and contributions required by law not optional extras. They exist to protect you when life happens: illness, injury, childbirth, job loss, old age, and more. Across Africa, and particularly in Kenya, understanding what is deducted from your payslip (and why) is one of the fastest upgrades you can make to your financial literacy.

This guide explains what statutory payments are, why they matter, the main types you will encounter, and the specific Kenyan framework NSSF, SHIF/SHA, PAYE, the Affordable Housing Levy, and WIBA. For the deepest reference, Serrari’s advice on statutory payments in Kenya and critical statutory payments and deductions in Kenya are the anchor resources.

Markets move fast; don’t get left behind. Pair the Serrari Group Market Index with a curated Serrari Marketplace and the comprehensive Wealth Builder Course to make sure you have the data — and the skills — to act on what you see.

What Are Statutory Payments?

Statutory payments are mandatory contributions or benefits that employers must make under national labour laws. They support employees during key life events — illness, injury, parental leave, unemployment, retirement — and fund the wider social protection system that backs workers and their families.

In simple terms: they are the legal workplace benefits that protect you when life happens. Some are paid by the employer, some by the employee, and many are matched between the two.

Why Statutory Payments Matter

Across Africa, statutory payments deliver five outcomes that private savings alone cannot:

- Income during difficult times — illness, injury, maternity, or job loss

- Protection from sudden hardship for workers and their dependants

- Fair labour standards enforced through national law

- Reduced income inequality through pooled social funds

- Long-term financial security via retirement and disability benefits

They act as a social safety net — but they are not a substitute for personal planning. See Serrari’s financial triangle and financial safety net guide for how statutory cover, private insurance, savings, and investments work together.

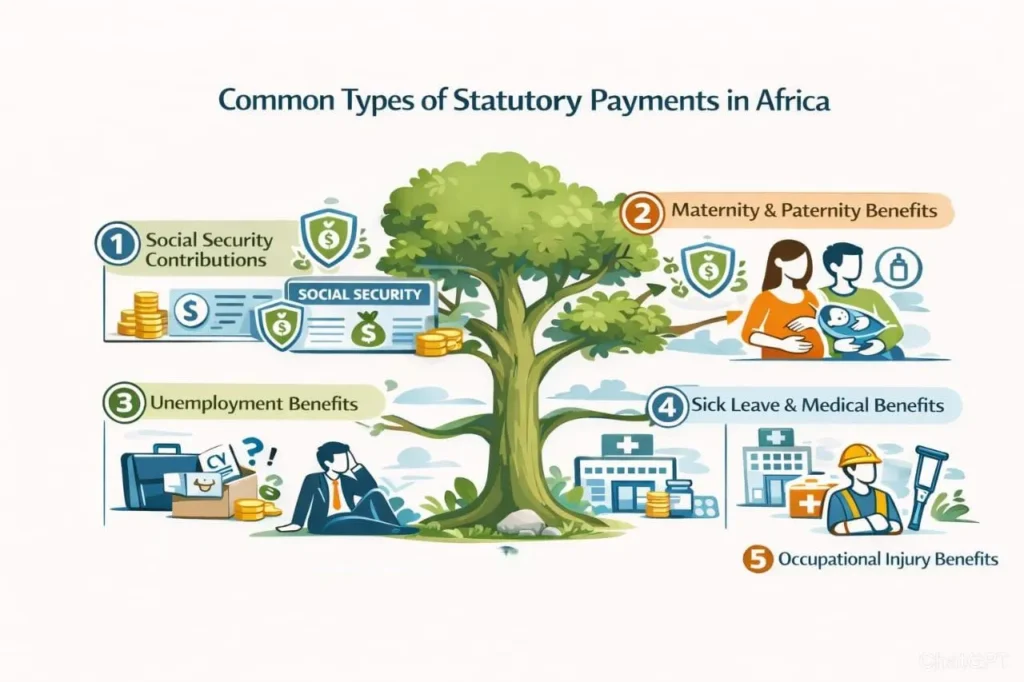

Common Types of Statutory Payments in Africa

Rules differ by country, but six categories appear consistently across the continent:

1. Social Security Contributions

Both employer and employee contribute, typically funding retirement pensions, disability benefits, and survivors’ benefits. In Kenya, this is driven by the National Social Security Fund (NSSF), with matched 6% employee and 6% employer contributions on pensionable pay, remitted monthly by the 15th.

For informal-sector and diaspora workers, NSSF’s Haba Haba plan offers flexible contributions. Most serious earners top up NSSF with a private pension — see Serrari’s best private pension fund in Kenya.

2. Maternity and Paternity Benefits

Paid leave for parents around childbirth and early childcare promotes family welfare and work-life balance. In Kenya, maternity leave is typically three months fully paid, and paternity leave two weeks — subject to the Employment Act. These are employer-paid benefits, not deductions.

3. Unemployment and Severance Benefits

Where an employee is dismissed involuntarily, statutory service pay (in jurisdictions where it applies) and NSSF portability provide temporary support while the worker finds new employment.

4. Sick Leave and Medical Benefits

Employees can take time off due to illness without losing income, and medical benefits cover doctor visits, hospitalisation, and medication. In Kenya, the Social Health Insurance Fund (SHIF), administered by the Social Health Authority (SHA), has replaced NHIF with a percentage-of-income model. See Serrari’s what is SHA and how is it different from NHIF and the detailed how much do I pay for SHA in Kenya.

5. Occupational Injury Benefits

If a worker is injured on the job, occupational injury cover pays for medical expenses, rehabilitation, and disability compensation. In Kenya this is provided under the Work Injury Benefits Act (WIBA), with the premium carried entirely by the employer.

6. Income Tax (PAYE) and Housing Levy

Pay As You Earn (PAYE) is the progressive income tax withheld at source and remitted to the Kenya Revenue Authority. Kenya also operates the Affordable Housing Levy — a 1.5% matched deduction upheld by the High Court — which funds the government’s affordable housing programme. See Serrari’s coverage of the Affordable Housing Levy introduction, the court ruling upholding the tax, and the latest collections data at KSh 26.8B. For rolling KRA tax rule updates, see KRA draft tax rules.

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Serrari Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder Course turns these insights into a professional-grade strategy.

Kenya’s Statutory Deductions at a Glance

Below is a current snapshot of the main employer and employee statutory contributions in Kenya. Confirm exact bands and thresholds against the latest KRA and SHA guidelines before payroll processing.

| Deduction | Employee Share | Employer Share | What It Covers |

| NSSF (Pension) | 6% of pensionable pay | 6% of pensionable pay | Retirement savings, disability, and survivors’ benefits — remitted monthly by the 15th |

| SHIF / SHA (Health) | 2.75% of gross pay (min ≈ KSh 300) | Employer facilitates | Kenya’s Social Health Insurance Fund under SHA — covers inpatient, outpatient, emergency & chronic care |

| Affordable Housing Levy | 1.5% of gross pay | 1.5% of gross pay | Funds the affordable housing programme; matched contribution upheld by the High Court |

| PAYE (Income Tax) | Progressive — 10% to 35% | Employer remits to KRA | Pay As You Earn income tax, withheld at source and remitted monthly to KRA |

| WIBA (Work Injury) | None | Employer-paid premium | Work Injury Benefits Act cover — medical, rehabilitation, and disability compensation for on-the-job injuries |

| NITA Levy | None | KSh 50 / employee / month | National Industrial Training Authority levy; funds workforce training and reimbursement |

For the full contribution mechanics, including who collects and remits what, see Serrari’s advice on statutory payments in Kenya, critical statutory payments and deductions in Kenya, and the update on SHA collections via the National Treasury.

Which Benefit Covers Which Life Event?

| Life Event | Benefit Category | Usual Source (Kenya) |

| Retirement | Social security / pension | NSSF + private pension top-ups |

| Illness or hospitalisation | Sick leave + medical cover | SHIF (via SHA) + employer sick-leave policy |

| Maternity / Paternity | Maternity & paternity leave | Statutory leave under Employment Act — paid by employer |

| On-the-job injury | Occupational injury cover | WIBA insurance (employer-paid) |

| Job loss | Severance / unemployment support | Statutory service pay (where applicable) + NSSF portability |

| Death / disability | Survivors’ and disability benefits | NSSF survivors’ benefits + life insurance where held |

Where statutory cover is thin, private products fill the gap. For private layers, explore Serrari’s guides on insurance and risk protection and risk management tools, plus financial risk management for employers.

Know Your Rights as an Employee

Every country has specific statutory requirements. As an employee or employer, you should be able to answer five questions at any time:

- What benefits am I entitled to?

- What are the contribution percentages for me and my employer?

- What are the eligibility conditions?

- How do I claim benefits when I need them?

- Where can I check that deductions are being remitted correctly?

Employers are legally required to comply with these rules and keep employees informed. For Kenyan employees, your payslip should clearly break down PAYE, NSSF, SHIF/SHA, and the Housing Levy. If anything is missing or unclear, ask — and escalate if necessary.

For Employers: Compliance and Cash Flow

Statutory payments are a compliance obligation and a cash-flow line item. Three practical habits keep SMEs out of trouble:

- Remit on time: most deductions (NSSF, PAYE, SHIF, Housing Levy) are due monthly — missing deadlines triggers penalties and interest

- Reconcile monthly: match payroll, bank remittances, and KRA/NSSF/SHA returns to avoid gaps

- Budget for the full employer cost: gross salary + NSSF 6% + Housing Levy 1.5% + WIBA + NITA levy is the real cost of hiring

Pair compliance with smart business planning using Serrari’s For Small Business hub and the wider financial risk management framework.

Turning Statutory Cover Into a Real Safety Net

Statutory benefits are the floor, not the ceiling. Three layers usually deliver the full protection most households need:

- Layer 1 — Statutory: NSSF pension, SHIF health, WIBA injury cover, statutory leave

- Layer 2 — Emergency liquidity: 3–6 months of essential expenses in a high-yield MMF, following the emergency fund simple guide

- Layer 3 — Private protection and growth: life, health, and disability insurance on top of SHIF; a private pension alongside NSSF; long-term investment and capital allocation that outruns inflation

Automate the private layers with Pay Yourself First, and track every moving piece on a single personal finance dashboard.

The Bigger Picture

Statutory payments are far more than payroll deductions. They are legal protections designed to promote dignity, stability, and economic fairness across every sector of the economy. Understanding them helps you:

- Protect your income

- Plan realistically for retirement, illness, and family events

- Advocate for your rights at work

- Make informed employment decisions when comparing offers and total compensation

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

FAQ: Statutory Payments in Kenya and Africa

How much is deducted from my salary in Kenya for statutory payments?

For a typical employee, the main deductions are PAYE (progressive 10–35% based on income bands), NSSF (6%), SHIF/SHA (2.75%, minimum ≈ KSh 300), and the Affordable Housing Levy (1.5%). Your employer matches NSSF and the Housing Levy, and also pays WIBA and NITA levies. For a worked breakdown, see Serrari’s advice on statutory payments in Kenya.

What’s the difference between NHIF and SHA/SHIF?

NHIF has been replaced by the Social Health Authority (SHA), which administers the Social Health Insurance Fund (SHIF). Contributions are now income-based (2.75% of gross pay, minimum around KSh 300) and cover a wider range of outpatient, inpatient, and chronic care. Serrari’s what is SHA and how is it different from NHIF walks through the key changes.

Is the Affordable Housing Levy optional?

No. The levy is a mandatory 1.5% of gross pay for employees, matched by a 1.5% employer contribution. Kenya’s High Court upheld its validity, and collections have crossed KSh 26.8 billion.

Do statutory benefits replace the need for private insurance or a private pension?

No. Statutory cover is a floor. Most people complement it with private health insurance, life cover, and a private pension — especially to protect income, dependants, and lifestyle in retirement. See Serrari’s insurance and risk protection and best private pension fund in Kenya.

How do Kenyans in the diaspora contribute to NSSF?

Through flexible voluntary products like NSSF’s Haba Haba plan, which allows small, regular contributions from overseas. For tax context on diaspora earnings, see Treasury targets diaspora with new tax rules.

What happens if my employer doesn’t remit statutory deductions?

Employers who fail to remit statutory deductions face penalties and interest, and can be compelled to pay arrears. Employees should verify contributions through official NSSF, SHA, and KRA portals, and escalate missing remittances to the relevant regulator. Keeping your own payslip records is the first line of defence.

Are business owners and sole proprietors required to contribute?

Business owners typically contribute both as employers (for their staff) and as individuals (PAYE on any employment income). Sole proprietors and self-employed professionals can contribute voluntarily to NSSF and register for SHIF, and are liable for income tax under KRA rules. A good accountant or Serrari Advisory engagement is worth the cost.

Stay Connected, Keep Growing

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the curated Wealth Builder Guide.

Stay connected to what truly matters. Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter on the Serrari Group homepage.

Growth opens doors. Advance your career through professional programs on Serrari Ed, including ACCA prep courses and the Financial Literacy special offer — designed to move you forward with confidence.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}