Compound interest is often called the “miracle of money.” It turns modest, consistent savings into substantial wealth over time by paying you interest not just on your initial principal, but also on the interest that has already accumulated. Understanding and leveraging this single concept is arguably the highest-leverage idea in all of personal finance — for Kenyan, African, and global investors alike.

This guide unpacks the mechanics, shows what compounding looks like with real Kenyan numbers, introduces the Rule of 72 as a mental shortcut, and maps the tools you can use to put compound interest to work. For Serrari’s specific deep-dives on doubling times, see understanding the Rule of 72 to double your investment and the interactive Rule of 72 investment calculator.

Markets move fast; don’t get left behind. Pair the Serrari Group Market Index with a curated Serrari Marketplace and the comprehensive Wealth Builder Course to make sure you have the data — and the skills — to act on what you see.

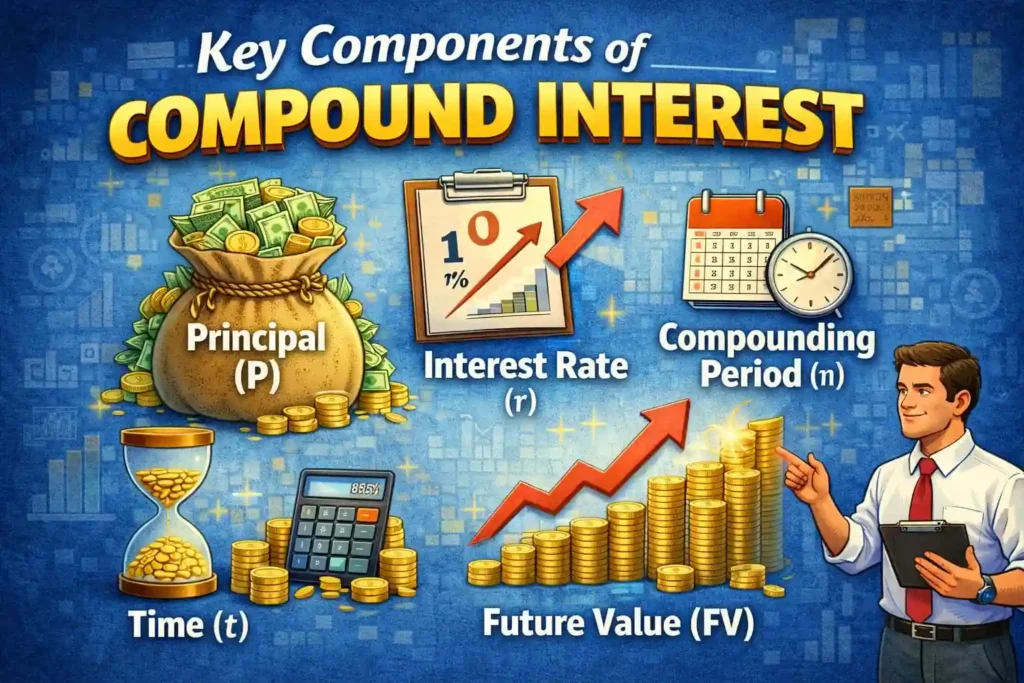

Key Components of Compound Interest

To make the most of compound interest, you need to understand five variables that drive its power:

- Principal (P): the initial amount of money you invest or save.

- Interest Rate (r): the percentage your money earns per period (usually annual).

- Time (t): how long the money is invested or allowed to compound.

- Compounding Frequency (n): how often interest is added — daily, monthly, quarterly, annually.

- Future Value (FV): the total amount your investment will grow to, including the principal and all accumulated interest.

The Compound Interest Formula

FV = P × (1 + r / n)^(n × t)

This formula shows that your money grows faster as you invest longer (larger t) and compound more frequently (larger n) — with a fixed rate doing the exponential heavy-lifting in the background.

Simple Interest vs Compound Interest

| Aspect | Simple Interest | Compound Interest |

| Calculation | Only on the original principal | On principal + accumulated interest |

| Growth pattern | Linear over time | Exponential over time |

| Formula | Interest = P × r × t | FV = P × (1 + r/n)^(n·t) |

| Effect over decades | Limited growth | Snowball effect accelerates wealth |

| Compounding frequency | Not relevant | More frequent = faster growth |

Why Compound Interest Is So Powerful

The power of compound interest compresses five ideas into one equation:

- Exponential growth: the interest you earn also earns interest, multiplying your wealth far faster than simple interest.

- Accelerated accumulation: by reinvesting earnings, your money works for you continuously, shortening the path to financial goals.

- Long-term dominance: the longer you stay invested, the more dramatic the growth. The last decade matters more than the first.

- Snowball effect: compounding starts slowly but gains momentum, creating a self-reinforcing cycle of growth.

- Financial freedom: with disciplined saving and smart investing, compounding is the engine that makes retirement and independence realistic.

Warning: compound interest is equally ruthless when it works against you. Credit cards, mobile loans, and unsecured debt compound at annualised rates of 24–100%+ in many African markets. Paying off high-interest debt before aggressive investing is almost always the right sequence.

Compound Interest in Action: A KSh 100,000 Example

Imagine you invest KSh 100,000 at a 10% annual interest rate, compounded annually, and leave it untouched:

| Year | Opening Balance (KSh) | Interest @ 10% (KSh) | Closing Balance (KSh) |

| 1 | 100,000 | 10,000 | 110,000 |

| 2 | 110,000 | 11,000 | 121,000 |

| 3 | 121,000 | 12,100 | 133,100 |

| 5 | 146,410 | 14,641 | 161,051 |

| 10 | 235,795 | 23,579 | 259,374 |

| 20 | 611,591 | 61,159 | 672,750 |

| 30 | 1,586,309 | 158,631 | 1,744,940 |

Notice how the annual interest figure grows each year. In year 1 it is KSh 10,000; by year 30 the interest alone is KSh 158,631 — more than the entire original principal. That is the snowball effect in numbers.

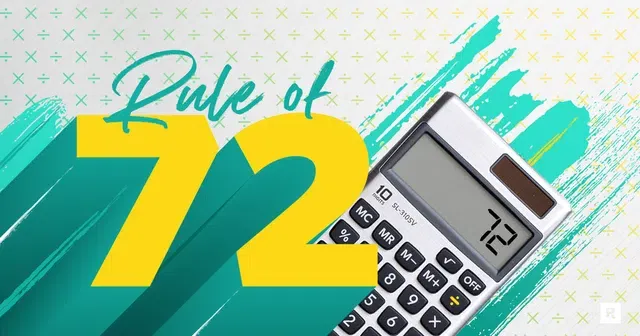

The Rule of 72: A Mental Shortcut for Doubling

The Rule of 72 is a simple arithmetic trick that estimates how long it takes for an investment (or debt) to double at a given rate of compound growth. Divide 72 by the annual rate, and you have a close approximation of the doubling period in years. Serrari’s full primer is in understanding the Rule of 72 to double your investment, with practical answers in the Rule of 72 calculator FAQs, and an interactive Rule of 72 investment calculator for your own numbers.

| Annual Return | Years to Double (Rule of 72) | Real-World Example |

| 4% | 72 ÷ 4 ≈ 18 years | Low-yield savings account |

| 8% | 72 ÷ 8 = 9 years | Blended balanced portfolio |

| 10% | 72 ÷ 10 ≈ 7.2 years | Long-run equity / diversified growth |

| 12% | 72 ÷ 12 = 6 years | Kenyan Money Market Fund yields |

| 14% | 72 ÷ 14 ≈ 5.1 years | Longer-dated Kenya T-Bonds (historical ranges) |

The rule is most accurate between 6% and 10%, but remains a useful estimate across most real-world rates. Use it as a sanity check, not a precise calculation.

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Serrari Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder Course turns these insights into a professional-grade strategy.

The Cost of Waiting: Early vs Late Starter

The single most important decision with compound interest is when you start, not how much you start with. Compare three savers who all invest KSh 10,000 per month at 10% annual compound growth:

| Investor | Contribution Plan | Total Contributed | Balance at 60 @ 10% |

| Amina — Early Starter | KSh 10,000/month from age 25 to 35, then stops | KSh 1.2M | ≈ KSh 42M+ |

| Brian — Late Starter | KSh 10,000/month from age 35 to 60 | KSh 3.0M | ≈ KSh 13M |

| Catherine — Lifetime Saver | KSh 10,000/month from age 25 to 60 | KSh 4.2M | ≈ KSh 55M+ |

Amina stopped saving at 35 after only 10 years of contributions. Brian started at 35 and saved for 25 years — and still ended up with less. The gap is compound interest rewarding time in the market. The earlier you automate contributions via Pay Yourself First, the bigger the gap works in your favour.

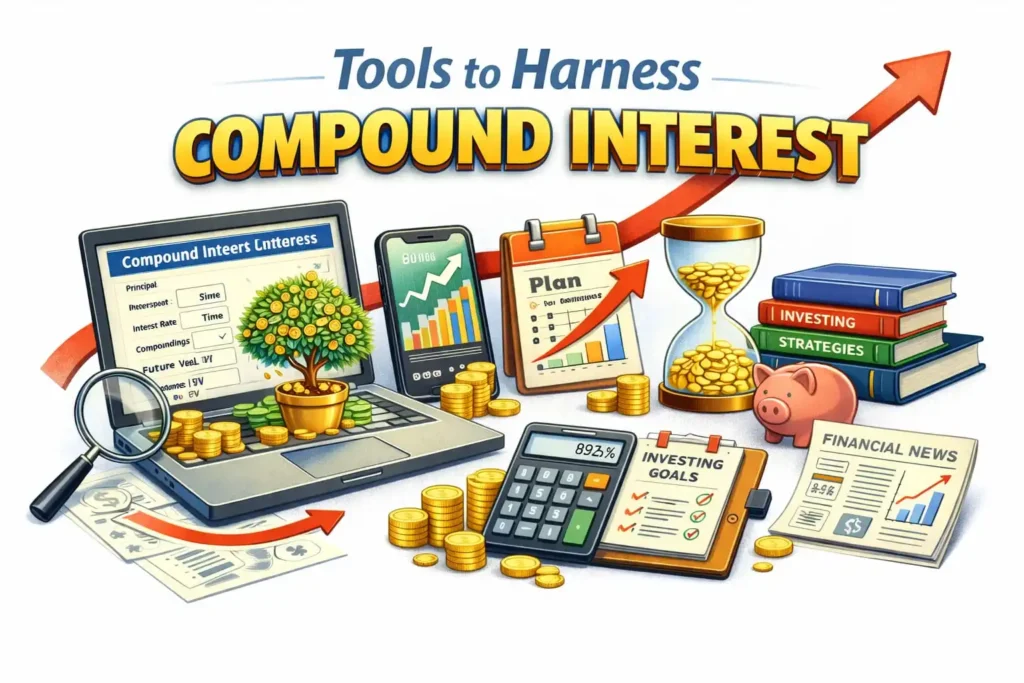

Tools to Harness Compound Interest

Compounding is not magical — it happens inside specific vehicles that reinvest earnings for you. Here is how to deploy it practically in Kenya and globally:

| Tool | How It Compounds (Kenya Context) |

| Savings accounts | Daily or monthly compounding; low yield but low risk — useful for very short-term cash only |

| Money Market Funds (MMFs) | Daily compounded yields typically 12–16% in Kenya; liquid within 1–3 business days |

| Fixed Deposits | Higher rates locked for a term; interest reinvested at maturity; ladder to reduce reinvestment risk |

| Treasury Bonds | Coupons reinvested into MMFs or more T-Bonds compound steadily; T-Bills cycle short-term cash |

| Mutual Funds & ETFs | Reinvested dividends and capital gains compound tax-efficiently inside the fund |

| Pension / Retirement accounts | Tax-relieved contributions compound over decades — one of the most powerful tools available to Kenyan earners |

| Dividend Reinvestment Plans (DRIPs) | Automatic reinvestment of stock dividends into more shares — pure compounding discipline |

| Equity portfolios | Capital appreciation plus reinvested dividends; best used over 10+ year horizons |

| REITs | Distributions reinvested; rental-income growth adds an inflation-linked kicker |

Compare yields on the Kenya Money Market Funds yield comparator, explore Treasury Bonds in Kenya and Fixed Deposit strategies for the fixed-income sleeve, Kenya’s REIT surge for real estate, and how to access global index funds from Kenya for global equity compounding. For retirement-account compounding, see Serrari’s best private pension fund in Kenya.

Compound Interest and Real Returns

Inflation is the silent enemy of compounding. A 10% nominal return in a 4.5% inflation environment is really a 5.5% real return. Serrari’s understand inflation and how to beat it and reporting on Fixed Deposit returns outpacing inflation explain why you should always think in real, not nominal, numbers when planning long horizons.

Lessons From Warren Buffett

“My wealth has come from a combination of living in America, some lucky genes, and compound interest.”

Even the world’s most celebrated investors lean on the same quiet mechanism that is available to every salaried Kenyan, Nigerian, or South African saver. The difference is not talent — it is consistency, patience, and starting early. Serrari’s pieces on the surprising golden rule of wealth and timeless wealth lessons reinforce the same point from different angles.

Takeaways: How to Put Compounding to Work

- Start early: every year you delay costs you disproportionately at the end

- Be consistent: regular automated contributions smooth out market cycles and build discipline

- Reinvest earnings: do not withdraw interest, dividends, or distributions; let them compound

- Be patient: compounding rewards decades, not months

- Avoid high-interest debt: compounding in reverse destroys wealth faster than it creates it

Protect the principal that is doing the compounding. Build a 3–6 month emergency fund and a robust financial safety net so you never have to sell compounding assets at the wrong time. Anchor the whole plan in the financial triangle and track progress on a personal finance dashboard.

Bottom Line

Compound interest is the cornerstone of wealth creation. It transforms small, consistent contributions into substantial sums over time — as long as three conditions are met: you start early, you stay invested, and you keep costs and debt under control.

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

FAQ: Compound Interest

What is the simplest way to explain compound interest?

Compound interest is interest on interest. Every period, your interest is added to the principal, and the next period’s interest is calculated on the larger balance. Over time, this snowballs into exponential growth.

What is the Rule of 72?

The Rule of 72 is a shortcut for estimating how long it takes money to double: divide 72 by the annual rate. Serrari’s Rule of 72 calculator lets you plug in your own numbers.

How often should compounding happen?

More frequent compounding (daily > monthly > annually) produces slightly larger gains at the same rate. In practice, the difference over long horizons is smaller than the impact of starting early and reinvesting consistently.

Does compound interest beat inflation?

Only if your return exceeds inflation. Focus on real (after-inflation) returns, not headline rates. See Serrari’s understand inflation and how to beat it.

Is compound interest taxed?

Interest and dividends are generally subject to withholding tax in Kenya, though rates differ by product. Retirement and tax-deferred accounts can shelter compounding from annual tax drag and are among the most effective vehicles for long-term wealth.

Can compound interest work against me?

Yes. High-interest debt such as credit cards and mobile loans compounds against you, often at rates far above any investment return. Clearing this debt is almost always the highest risk-adjusted return you can earn.

What is the single most important compounding habit?

Automating contributions. Whether through Pay Yourself First, standing orders into an MMF, or monthly pension deductions, the goal is to make compounding happen whether you think about it or not. Consistency beats cleverness.

Stay Connected, Keep Growing

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the curated Wealth Builder Guide.

Stay connected to what truly matters. Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter on the Serrari Group homepage.

Growth opens doors. Advance your career through professional programs on Serrari Ed, including ACCA prep courses and the Financial Literacy special offer — designed to move you forward with confidence.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}