The U.S. housing market suggests a decade of slower home-price appreciation as higher borrowing costs and affordability challenges reshape buyer expectations. While homeownership is still expected to generate long-term wealth, economists believe gains will be significantly lower than those experienced during the post-pandemic housing boom.

The U.S. housing sector is entering a new phase after years of rapid appreciation that significantly increased household wealth. Economists now project a more moderate growth environment, driven by elevated mortgage rates, higher home prices, and shifting affordability dynamics. Although homeowners are still expected to build wealth over time, the pace of gains is likely to be much slower than during the previous decade.

According to projections from Moody’s Analytics, national home prices are expected to grow at an average annual rate of approximately 2.1% between 2026 and 2035. This represents a notable slowdown from the roughly 5% annual appreciation recorded over the last decade, based on S&P CoreLogic Case-Shiller data.

Key Overview

- Moody’s Analytics projects U.S. home prices to grow by an average of 2.1% annually between 2026 and 2035.

- This is significantly lower than the approximately 5% annual home-price appreciation recorded over the past decade.

- Higher home prices and mortgage rates of around 6% to 7% are reducing affordability for many buyers.

- Economists believe these affordability challenges will limit the likelihood of another pandemic-era housing boom.

- Fannie Mae’s housing experts also forecast modest home-price growth of approximately 2.2% annually through 2028.

Why the U.S. Housing Market Is Slowing

The slowdown reflects a combination of affordability pressures and higher financing costs. During the pandemic, historically low interest rates helped fuel a surge in housing demand. Mortgage rates frequently fell below 3%, enabling buyers to borrow larger amounts at lower monthly costs.

Today, the situation is very different. The average 30-year fixed mortgage rate has remained well above pandemic-era levels, generally ranging between 6% and 7%. According to Freddie Mac data, the average rate stood at 5.98% in late February 2026 before rising to 6.53% by the end of May.

These higher borrowing costs have significantly affected affordability. Even modest increases in mortgage rates can substantially increase monthly payments, limiting purchasing power and reducing the number of qualified buyers entering the market.

As a result, the u.s housing market is experiencing slower demand growth despite continued interest from prospective homeowners.

Homeowners Still Expected to Build Wealth

While slower appreciation may disappoint some buyers hoping for rapid gains, homeownership remains a powerful wealth-building tool.

Bankrate calculations cited in recent reports show that a buyer purchasing a $500,000 home with a 10% down payment and a 6.5% mortgage could still accumulate approximately $234,000 in housing wealth over a 10-year period, even if annual home-price growth averages only 2.1%.

This highlights an important reality: real estate wealth is often built gradually rather than through short-term market surges. Long-term homeowners continue to benefit from principal repayment, property appreciation, and equity accumulation over time.

For many households, homeownership remains one of the most significant pathways to building financial security, even during periods of slower growth.

Recent U.S. Housing Market Trends Show Cooling Prices

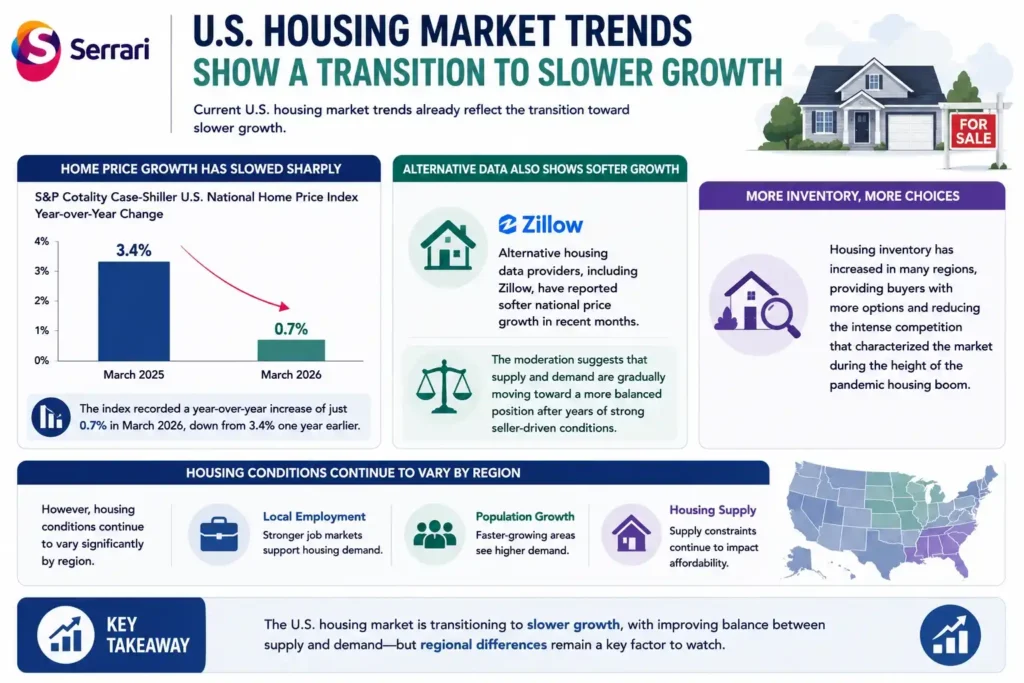

Current U.S. housing market trends already reflect the transition toward slower growth.

The S&P Cotality Case-Shiller U.S. National Home Price Index recorded a year-over-year increase of just 0.7% in March 2026. This marked a sharp decline from the 3.4% growth rate recorded one year earlier.

Alternative housing data providers, including Zillow, have also reported softer national price growth in recent months. The moderation suggests that supply and demand are gradually moving toward a more balanced position after years of strong seller-driven conditions.

Housing inventory has also increased in many regions, providing buyers with more options and reducing the intense competition that characterized the market during the height of the pandemic housing boom.

However, housing conditions continue to vary significantly by region. Local employment conditions, population growth, and housing supply constraints remain key factors influencing individual markets.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

The Impact of the U.S. Housing Market Mortgage Rates

One of the most important drivers of future housing performance will be the U.S. housing market mortgage rates.

Mortgage rates directly influence affordability because they determine the size of monthly loan payments. When rates rise, buyers either face higher payments or must reduce their home purchase budgets.

For example, a one-percentage-point increase in mortgage rates can add hundreds of dollars to monthly payments on a typical home loan. This effect often causes demand to cool quickly, particularly among first-time buyers.

Economists believe that any meaningful decline in mortgage rates could help stabilize housing activity. Lower rates would improve affordability, encourage more buyers to enter the market, and potentially support moderate price growth.

However, if rates remain elevated for an extended period, housing demand could continue to face pressure despite a relatively healthy labor market.

Economic Conditions Will Shape Future Demand

Broader economic conditions remain closely linked to housing activity.

April labor market data showed that non-farm payrolls increased by 115,000 jobs, while the unemployment rate stood at 4.3%. Average hourly earnings also rose by 3.6% over the previous 12 months.

These indicators suggest that the economy continues to generate employment and wage growth, supporting household purchasing power. Although demand has slowed compared to previous years, it has not disappeared entirely.

Housing-related spending continues to account for approximately 15% to 18% of U.S. gross domestic product and remains a major component of household wealth. Because of this, changes in home prices and borrowing costs can significantly influence consumer spending and overall economic activity.

If job growth remains steady and mortgage rates gradually ease, the U.S. housing market could stabilize without becoming a major drag on economic growth.

Conclusion

The U.S. housing market appears set for a decade of slower but steadier growth. Moody’s Analytics projects annual home-price appreciation of around 2.1% through 2035, reflecting the impact of higher mortgage rates and ongoing affordability challenges.

While homeowners may no longer experience the rapid wealth gains seen during the pandemic-era housing boom, real estate continues to offer long-term wealth-building opportunities. The market’s future trajectory will largely depend on mortgage rates, labor market strength, and regional supply conditions, making patience and long-term planning increasingly important for buyers and investors alike.

FAQs

1. Why is the U.S. housing market expected to slow down?

Higher home prices, elevated mortgage rates, and affordability challenges are reducing demand and limiting future home-price growth.

2. What home-price growth is forecast between 2026 and 2035?

Moody’s Analytics projects average national home-price growth of approximately 2.1% annually during that period.

3. Are mortgage rates still affecting housing demand?

Yes. Mortgage rates between 6% and 7% have significantly increased borrowing costs, reducing affordability for many buyers.

4. Can homeowners still build wealth despite slower price growth?

Yes. Long-term homeowners can still accumulate substantial equity through mortgage repayment and moderate property appreciation over time.

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}