Recent Kenya bank lending data from the Central Bank of Kenya (CBK) shows banks are becoming more selective in how they deploy credit despite improving liquidity levels. While lending to trade, financial services, and households increased during the first quarter of 2026, lenders remained cautious toward sectors such as real estate, reflecting ongoing concerns about asset quality and economic risks.

Key Overview

- Total banking sector assets increased by 3.8% to KSh 8.73 trillion in the three months to March 2026.

- Deposits also grew 3.8% to KSh 6.51 trillion.

- Gross loans expanded 1.9% to KSh 4.45 trillion.

- Loans as a share of assets declined from 51.9% to 51.0%, indicating slower credit growth relative to asset expansion.

- About 86% of banks reported improved liquidity positions.

- 27% of banks preferred private-sector lending as their primary use of excess liquidity.

- Trade recorded the highest level of easing in credit standards, with 24% of lenders reporting more accommodative lending conditions.

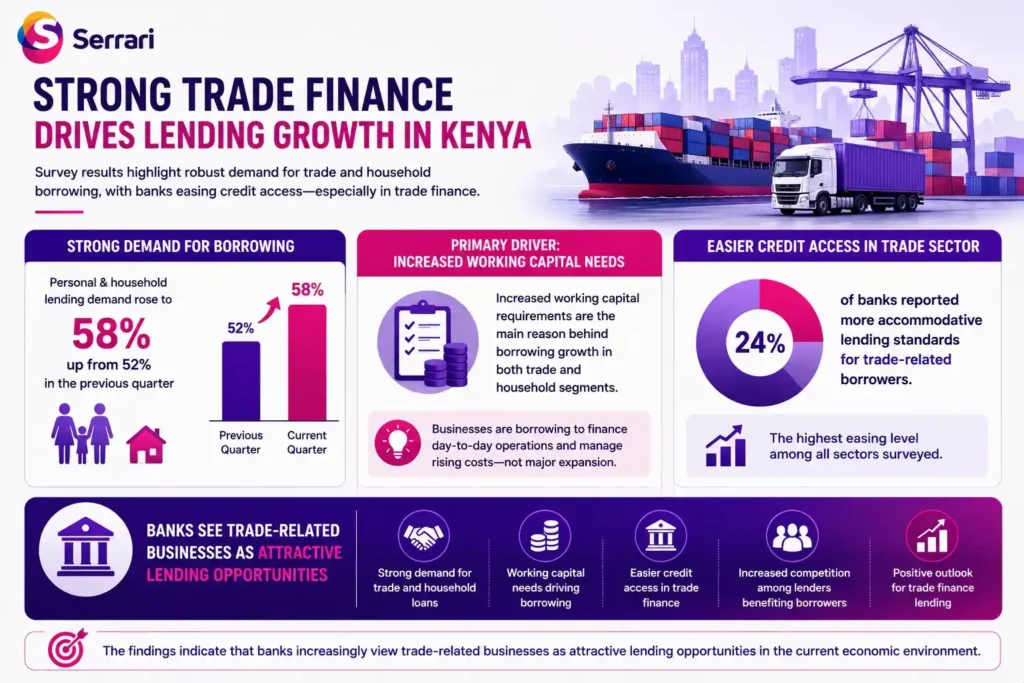

- Personal and household lending demand increased to 58%, up from 52% in the previous quarter.

- The gross non-performing loan ratio rose to 15.6% from 15.4%.

- Real estate faced the highest level of credit tightening, with 30% of lenders reporting stricter lending standards.

Kenya Bank Lending Trends Reflect Strong Liquidity and Cautious Growth

The latest Central Bank of Kenya survey reveals evolving Kenya bank lending trends as financial institutions balance strong liquidity positions with concerns over rising non-performing loans and sector-specific risks.

The survey, covering 39 lenders, shows that Kenya’s banking industry entered 2026 with stronger balance sheets, higher deposits, and improved liquidity. However, banks remain cautious in extending credit aggressively, particularly to sectors perceived as carrying elevated risks.

While borrowing activity has increased across several industries, lenders are carefully managing exposure as bad loans continue to grow faster than overall credit expansion.

The result is a banking sector that appears willing to lend but remains highly selective about where that lending occurs.

Banking Sector Assets and Deposits Continue Growing

The latest data highlights continued growth across the Kenyan banking sector.

Total banking sector assets increased by 3.8% during the first quarter of 2026, reaching KSh 8.73 trillion. Deposits also expanded by 3.8%, rising to KSh 6.51 trillion.

The growth in deposits has strengthened liquidity across the industry, giving banks greater flexibility in allocating funds and supporting future lending opportunities.

According to the survey, 86% of banks reported improved liquidity positions. The increase was largely driven by stronger deposit inflows, maturing government securities, and successful loan recoveries.

This improved liquidity environment has reduced reliance on interbank borrowing and strengthened the industry’s overall financial position.

Commercial Bank Loans Kenya Continue to Expand

Growth in commercial bank loans Kenya remained positive during the quarter despite ongoing economic challenges.

Gross loans increased by 1.9% to reach KSh 4.45 trillion. The expansion was primarily driven by increased lending to financial services, households, and the energy and water sectors.

However, loan growth lagged behind overall asset growth. Loans accounted for 51.0% of total assets in March compared to 51.9% three months earlier.

This decline suggests banks are accumulating assets faster than they are deploying capital through lending activities.

The trend reflects a cautious approach as lenders seek to balance growth opportunities with risk management considerations.

Trade Finance Kenya Emerges as a Key Growth Area

One of the most notable developments in the survey was the strength of trade finance Kenya lending activity.

Trade and personal household borrowing recorded some of the strongest demand levels during the quarter. According to the survey, personal and household lending demand rose to 58%, up from 52% in the previous quarter.

Importantly, increased working capital requirements were identified as the primary driver behind borrowing growth in both trade and household segments.

This suggests that many businesses are borrowing to finance day-to-day operations and manage rising costs rather than fund major expansion projects.

Competition among lenders also contributed to easier credit access in the trade sector. Approximately 24% of banks reported more accommodative lending standards for trade-related borrowers, the highest easing level among all sectors surveyed.

The findings indicate that banks increasingly view trade-related businesses as attractive lending opportunities in the current economic environment.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Bank Credit Standards Remain Mostly Stable

Overall bank credit standards remained broadly unchanged across the 11 sectors covered by the CBK survey.

However, competition among lenders appears to be influencing lending decisions. Around 34% of surveyed banks indicated that competition from other financial institutions contributed to some easing of credit standards.

Banks are actively seeking quality borrowers while attempting to maintain prudent risk management practices.

The selective easing of lending requirements reflects a balancing act between supporting credit growth and protecting balance sheets from future loan losses.

As economic activity improves and liquidity remains strong, competition for creditworthy customers could continue influencing lending strategies throughout the year.

Real Estate Lending Kenya Faces Increased Caution

Despite stronger lending activity in some sectors, real estate lending Kenya continues to face significant caution from lenders.

The survey found that approximately 30% of banks tightened lending standards for real estate borrowers, the highest tightening level recorded among all sectors.

Building and construction, as well as tourism and hospitality, also experienced increased scrutiny, with 24% of lenders reporting tighter credit conditions.

The cautious stance toward real estate likely reflects concerns about market conditions, repayment risks, and the broader challenges facing the property sector.

Banks appear increasingly selective when evaluating real estate projects and borrowers, preferring to limit exposure to segments perceived as carrying elevated credit risk.

This cautious approach contrasts sharply with the more accommodative treatment observed in trade-related lending.

Rising Non-Performing Loans Remain a Concern

One factor influencing lending behavior is the continued deterioration in asset quality.

The gross non-performing loan ratio increased to 15.6% in March 2026 from 15.4% in December 2025. During the quarter, bad loans increased by 3.4%, significantly outpacing overall loan growth of 1.9%.

The increase indicates that banks are still accumulating problematic loans even as borrowing activity begins to recover.

This trend may help explain why lenders are expanding credit cautiously despite having substantial liquidity available.

Financial institutions remain focused on balancing growth objectives with the need to manage credit risk effectively.

Profits Come Under Pressure

While balance sheet growth remained strong, profitability faced modest pressure.

Quarterly profit before tax declined slightly to KSh 83.5 billion from KSh 83.9 billion in the previous quarter.

The decline was driven by a combination of rising operating expenses and lower income. Industry expenses increased by KSh 5.2 billion, while income declined by KSh 1.7 billion.

Although the reduction was relatively small, it highlights the challenges banks face in maintaining profitability amid changing economic conditions and rising credit risks.

Conclusion

The latest Kenya bank lending trends reveal a banking sector characterized by strong liquidity, moderate credit growth, and selective risk-taking. While trade and household lending continue to expand, banks remain cautious toward sectors such as real estate and construction.

Improved deposit growth and stronger liquidity positions provide lenders with ample capacity to support future borrowing. However, rising non-performing loans and weaker profitability are encouraging a measured approach to credit expansion. As competition intensifies and economic conditions evolve, lending decisions are likely to remain focused on balancing growth opportunities with prudent risk management.

FAQs

1. What are the latest Kenya bank lending trends?

Kenya bank lending trends show moderate credit growth alongside strong liquidity across the banking sector. While loans increased by 1.9% during the first quarter of 2026, banks remain cautious due to rising non-performing loans and sector-specific risks. Lending growth has been strongest in trade, financial services, and household borrowing.

2. Why are banks increasing lending to the trade sector?

Trade-related businesses are experiencing increased working capital requirements, creating stronger demand for financing. In addition, competition among banks has encouraged some lenders to ease credit standards for trade borrowers. This has made trade one of the most active sectors for credit growth during the period covered by the CBK survey.

3. Why are banks cautious about real estate lending in Kenya?

Many lenders remain concerned about risks within the real estate sector, leading to tighter lending standards. Approximately 30% of banks reported stricter requirements for real estate borrowers, the highest level of tightening among all sectors surveyed. Concerns about repayment capacity and market conditions continue to influence lending decisions.

4. How has liquidity changed in the Kenyan banking sector?

Liquidity has improved significantly across the industry, with 86% of surveyed banks reporting stronger liquidity positions. Increased deposits, maturing government securities, and successful loan recoveries contributed to the improvement. As a result, many banks now have excess liquidity available for lending and investment opportunities.

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}