Investing can feel complicated from the outside, but building an investment portfolio is simpler than most people think. At its core, a portfolio is just a thoughtful mix of assets — put together so that your money works for you across different market conditions, not just when one asset class is in favour.

This guide walks Kenyan, African, and global beginner investors through what an investment portfolio actually is, why diversification reduces risk, and the step-by-step process for building one that matches your goals, timeline, and risk tolerance. Before you commit a single shilling, make sure the foundation is in place: a clear budget, a fully funded emergency fund, and high-interest debt under control. Serrari’s guide to the financial triangle shows you exactly why these come first.

Markets move fast; don’t get left behind. Pair the Serrari Group Market Index with a curated Serrari Marketplace and the comprehensive Wealth Builder Course to ensure you have the data — and the skills — to act on it.

What Is an Investment Portfolio?

An investment portfolio is a deliberate collection of different assets — stocks, bonds, real estate, money market funds, ETFs, and sometimes alternatives — held together to reach a specific set of financial goals. The key word is deliberate. A portfolio is not a random pile of holdings; it is a designed mix where every asset plays a role. For a foundational read, see Serrari’s Investing Explained: a beginner’s guide to growing wealth and the deeper dive on investment and capital allocation.

A Simple Example: USD 10,000 Portfolio

Imagine you have $10,000 to invest. A balanced, beginner-friendly portfolio might look like this:

| Asset Class | Weight | Amount (USD 10k) | Role in the Portfolio |

| Stocks / Equities | 50% | $5,000 | Long-term growth engine — companies you believe will compound over years |

| Bonds (T-Bills / T-Bonds) | 30% | $3,000 | Stable income and ballast when markets fall |

| Real Estate / REIT | 15% | $1,500 | Inflation hedge via property and rental income |

| Money Market Fund | 5% | $500 | Liquidity buffer and cash management |

Why this works:

- Diversification — your money is spread across different assets that behave differently under the same conditions

- Complementary risks — some holdings are safer, others have higher growth potential

- Goal alignment — together the mix can fund retirement, a property purchase, or children’s education over time

Why Diversification and Allocation Matter

Two ideas do most of the heavy lifting in portfolio design: diversification and asset allocation.

Diversification reduces risk

When one investment stumbles, others in the portfolio can cushion the blow. A diversified portfolio rarely has a catastrophic year, even if individual holdings do. That smoother ride matters because behaviour — staying invested through downturns — is the biggest driver of long-term returns.

Asset allocation drives most of the outcome

Decades of research show that the mix of asset classes you choose explains far more of your returns than the specific stocks or funds you pick. Get the allocation right first; the details come second. For Kenyan and diaspora investors, the Kenyan Economic & Market Outlook and the Global Markets Outlook from Serrari Analysis are good starting points for understanding the current macro backdrop.

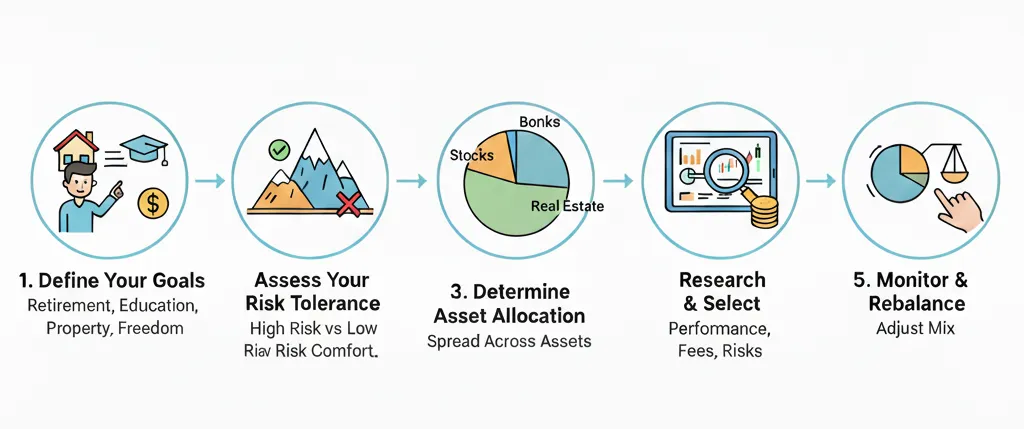

How to Build an Investment Portfolio in 5 Steps

1. Define your goals

Write down what you are investing for and when you will need the money: retirement in 30 years, a property deposit in 5 years, children’s education in 10. Each goal has a different time horizon, which should drive how aggressive the portfolio can be.

2. Assess your risk tolerance

Some investors sleep soundly through a 30% drawdown; others panic at a 5% dip. Be honest. A portfolio you cannot stick with during a bear market is worse than a lower-return portfolio you can.

3. Determine your asset allocation

Decide the target weights across stocks, bonds, real estate, and cash. A simple rule of thumb for beginners is to match the portfolio to your risk profile:

| Risk Profile | Stocks | Bonds | Real Estate | Cash / MMF | Best For |

| Conservative | 20% | 55% | 10% | 15% | Capital preservation, near-retirement, short horizon |

| Balanced | 50% | 30% | 15% | 5% | Mid-career, 5–15 year horizon, steady growth |

| Growth | 75% | 10% | 10% | 5% | Young investors, 15+ year horizon, higher risk tolerance |

4. Research and select investments

Within each asset class, compare options on historical performance, fees, liquidity, management track record, and underlying risks. Practical Kenyan starting points include:

- How Treasury Bonds work in Kenya and the Treasury Bonds Kenya FAQs for the bond sleeve

- Kenya Money Market Fund yield comparator for the cash/liquidity sleeve

- How to access global index funds from Kenya for global equity diversification

- How to invest in Kenya from abroad for diaspora investors

Compare products side-by-side on the Serrari Marketplace before committing money.

5. Monitor and rebalance

Markets move, and over time your portfolio drifts away from its target weights. Review at least annually (quarterly is better) and rebalance — trim what has grown too large and top up what has lagged — to keep the risk profile intact. Build a single view with Serrari’s guide to the personal finance dashboard.

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Serrari Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder Guide turns these insights into a professional-grade strategy.

Tips for Long-Term Portfolio Success

- Automate contributions: Set a standing order on payday so you pay yourself first — consistency beats timing.

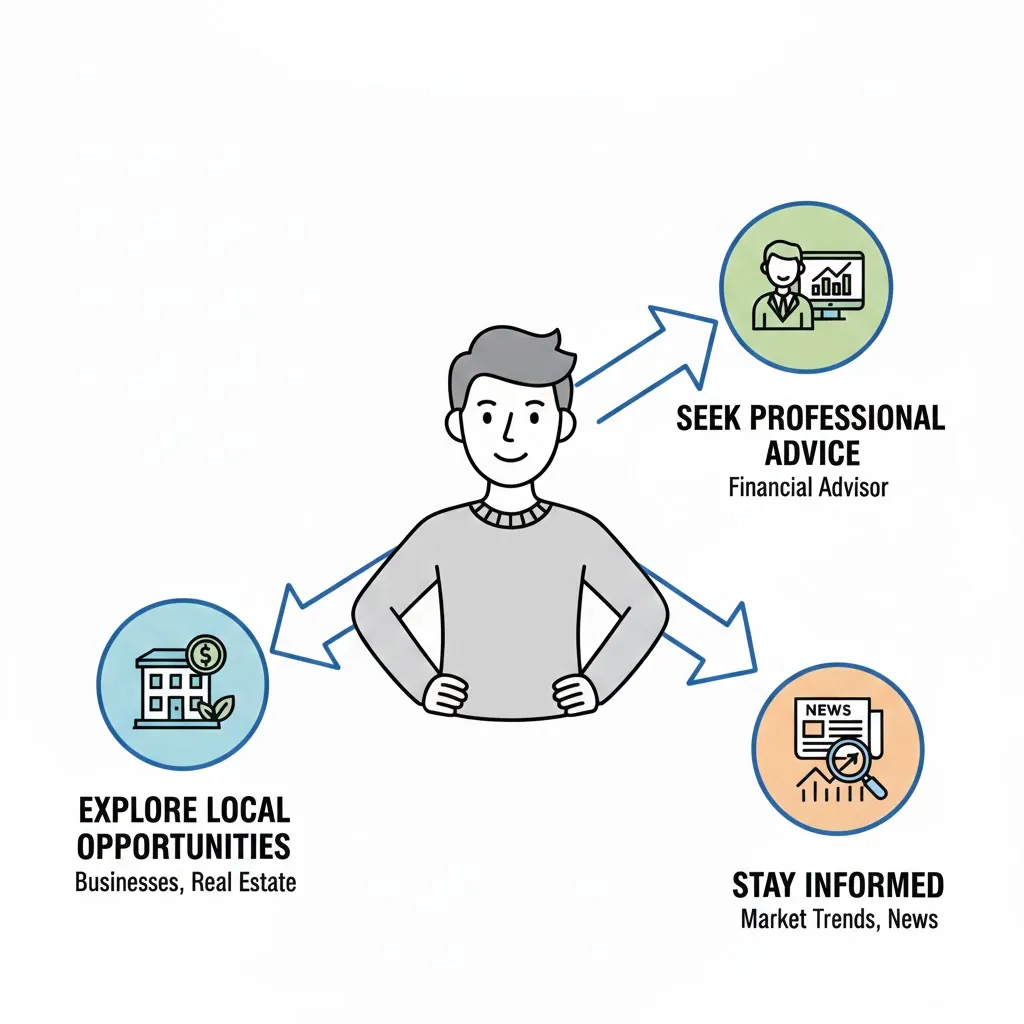

- Explore local and regional opportunities: Well-chosen NSE stocks, T-Bills, T-Bonds, REITs, and money market funds can anchor an African investor’s portfolio.

- Go global where it counts: Global index funds spread risk across currencies and economies — a crucial complement to local holdings.

- Keep fees low: Over 20+ years, a 1% annual fee difference can consume a quarter of your returns.

- Seek professional advice: Serrari Advisory can tailor the portfolio to your goals, tax situation, and risk profile.

- Stay informed: Track macro trends, regulatory changes, and sector rotations without reacting to every headline.

Common Portfolio Mistakes to Avoid

- Investing before you have an emergency fund. Build your safety net first so you never have to sell investments in a down market to cover an unexpected bill.

- Chasing last year’s winners. The best-performing asset class this year is often a poor predictor of next year.

- Over-concentration in one stock, sector, or country — especially your employer’s stock.

- Ignoring fees and tax efficiency.

- Checking the portfolio daily. Volatility feels worse than it is; daily checking breeds panic selling.

Key Takeaways

- A portfolio diversifies risk and increases growth potential when constructed intentionally.

- Asset allocation drives most of your long-term returns — not individual picks.

- Building a portfolio is a step-by-step process, not a one-time event.

- Regular monitoring, periodic rebalancing, and informed decisions compound into real wealth.

Remember: investing wisely today can help secure a prosperous future tomorrow. The timeless wealth lessons from Buffett, Munger, and Dalio all converge on the same point — consistent behaviour beats clever strategy.

FAQ: Investment Portfolios for Beginners

What is the simplest investment portfolio for a beginner?

A three-fund portfolio — one global equity fund, one local or regional bond fund, and a money market fund for liquidity — is often enough. Start there, automate contributions, and add complexity only when you understand why. The Investing Explained beginner’s guide walks through the basics.

How much money do I need to start investing?

Much less than most people think. In Kenya, you can enter Treasury Bonds from KSh 50,000, money market funds from as little as KSh 100–1,000, and many unit trusts from KSh 1,000. See the Kenya Money Market Funds comparator for current yield and minimum-entry details.

How do I know my risk tolerance?

Ask yourself: if my portfolio dropped 30% next year, would I (a) add more at discount prices, (b) hold and wait, or (c) sell to stop the bleeding? A/B answers suggest higher risk tolerance; C suggests a conservative or balanced allocation. Also factor in your time horizon — longer horizons justify more equity.

Should Kenyan investors hold international assets?

Yes, in moderation. Global diversification reduces country-specific risk and gives you exposure to sectors (technology, global consumer brands) underrepresented locally. See Serrari’s guide on accessing global index funds from Kenya for practical pathways.

How often should I rebalance my portfolio?

Once or twice a year is enough for most investors, or when any asset class drifts more than 5–10 percentage points from its target. Rebalancing forces you to sell high and buy low by design.

Can I manage my own portfolio or should I use an advisor?

Both paths work. If your situation is straightforward, a simple self-managed portfolio on the Serrari Marketplace can do the job. If you have complex income streams, cross-border assets, or a business, Serrari Advisory offers personalised guidance.

What is the difference between saving and investing?

Saving protects money you need soon; investing grows money you will need later. Both belong in a complete plan. Serrari’s guide on the difference between saving, investing, and insurance breaks this down clearly.

Stay Connected, Keep Growing

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the curated Wealth Builder Guide.

Stay connected to what truly matters. Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter on the Serrari Group homepage.

Growth opens doors. Advance your career through professional programs on Serrari Ed, including ACCA prep courses and the Financial Literacy special offer — designed to move you forward with confidence.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}