Every investor learns one truth the hard way: portfolios go up and down. That is normal, not a flaw. Markets breathe with inflation and interest rates, economic expansions and slowdowns, government policies, company earnings, and even geopolitical and environmental shocks. You cannot control any of those forces. What you can control is how you prepare for them — and that preparation has a name: balancing and diversification.

This guide walks Kenyan, African, and global beginner investors through what a balanced portfolio actually is, how rebalancing keeps your risk in check, and the practical habits that separate long-term winners from reactive traders.

Markets move fast; don’t get left behind. Pair the Serrari Group Market Index with a curated Serrari Marketplace and the comprehensive Wealth Builder Course to make sure you have the data — and the skills — to act on what you see.

What Is a Balanced Portfolio?

A balanced portfolio is an investment strategy that spreads your money across different asset classes — typically stocks, bonds, real estate, and cash — to reduce risk while still pursuing steady growth. Instead of betting everything on a single company, sector, or country, you diversify so that when one part of the portfolio falls, another tends to hold up. For a foundational walk-through, see Serrari’s Investing Explained: beginner’s guide to growing wealth and the deeper dive on investment and capital allocation.

A balanced portfolio typically diversifies into:

- Stocks / equities — higher growth potential, higher volatility

- Bonds (T-Bills and T-Bonds) — lower risk and steady income. See Treasury Bonds in Kenya for details

- Real estate — inflation hedge via property and rental income

- Cash or short-term investments (MMFs, fixed deposits) — liquidity and a low-risk anchor

The goal is not the highest return at any cost. The goal is the right mix between growth and stability for your circumstances.

Simple Example: Balancing KSh 1,000,000

The same KSh 1,000,000 can be shaped into very different portfolios depending on the investor. Three common profiles:

Option 1: Conservative Investor

Prefers lower risk, typically close to retirement or with short-term goals. Target: 70% Bonds / 30% Stocks. Expect moderate returns, low volatility, and more stability through market stress.

Option 2: Growth Investor

Young, long-term focused, comfortable with risk and large drawdowns. Target: 70% Stocks / 30% Bonds. Expect higher long-run returns, bigger swings, and better compounding over 15–30 years.

Option 3: Balanced Investor

Wants a middle ground — steady growth without extreme volatility. Target: 60% Bonds / 40% Stocks (or 50/50). Expect controlled risk, consistent income, and a smoother ride.

Sample Allocations in Kenyan Shillings

| Investor Profile | Stocks | Bonds | Cash/MMF | Expected Experience |

| Conservative (KSh 1,000,000) | 30% — KSh 300,000 | 60% — KSh 600,000 | 10% — KSh 100,000 | Steady income, lower volatility, limited downside |

| Balanced (KSh 1,000,000) | 50% — KSh 500,000 | 40% — KSh 400,000 | 10% — KSh 100,000 | Moderate growth with a meaningful income cushion |

| Growth (KSh 1,000,000) | 70% — KSh 700,000 | 25% — KSh 250,000 | 5% — KSh 50,000 | Higher long-run returns, larger drawdowns along the way |

There is no one-size-fits-all allocation. Your goals, horizon, income stability, and temperament decide the right mix — which is also why Serrari Advisory exists for investors who want a tailored plan.

What Is Portfolio Rebalancing?

Over time, your portfolio drifts away from its target weights. If stocks have a strong year, they might grow from 40% of the portfolio to 55%. That is good news for the account balance — but it also means you are now taking more risk than you originally planned. Rebalancing brings the portfolio back home.

Rebalancing means:

- Selling some of what grew too much

- Adding to what became smaller

- Returning to your original target mix

Done consistently, it forces you to sell high and buy low — the exact opposite of what most investors do on instinct. Think of it like realigning your car wheels: it keeps you on track and the ride smooth.

Drift in Action

| Asset | Target | After a Strong Year | Rebalancing Action |

| Stocks | 40% | 55% | Trim back toward 40% |

| Bonds | 50% | 38% | Top up toward 50% |

| Cash / MMF | 10% | 7% | Top up toward 10% |

Rebalancing can be calendar-based (once or twice a year) or threshold-based (whenever any asset drifts 5–10 percentage points from target). A yearly check, supported by a personal finance dashboard, is enough for most beginner investors.

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Serrari Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder Course turns these insights into a professional-grade strategy.

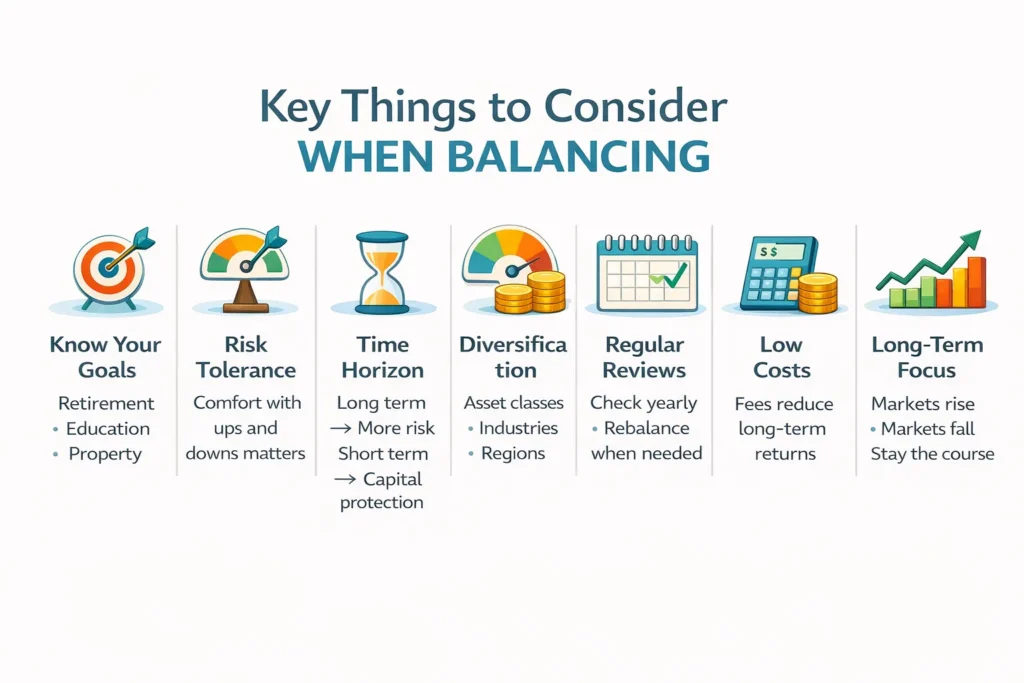

Key Things to Consider When Balancing

1. Know your goals

Retirement, a home deposit, education, financial independence — each has a different time horizon and different acceptable risk. Goals drive strategy, not the other way around. Anchor the whole plan in Serrari’s financial triangle framework.

2. Understand your risk tolerance

Can you hold through a 25% drawdown without selling? If the answer is no, your allocation is too aggressive. A plan you can stick with always beats an optimal plan you abandon at the bottom.

3. Think about time horizon

- Long horizon (10+ years): Can take more equity risk; drawdowns have time to heal

- Short horizon (< 3 years): Protect capital; favour bonds, MMFs, and fixed deposits

4. Diversify properly

Diversification is more than owning many stocks. Spread across:

- Asset classes — equities, fixed income, real estate, cash

- Industries — technology, financials, consumer, healthcare, energy

- Regions — Kenyan (NSE, T-Bonds), African, and global markets. For global exposure, see how to access global index funds from Kenya

Avoid over-concentration in any single company, sector, or country — including your employer’s stock.

5. Review regularly

Check the portfolio at least annually. Rebalance when target weights drift too far. Quarterly checks are a sensible upgrade once you have more than one account.

6. Keep costs low

High fees compound against you. Over 20–30 years, a 1% annual fee difference can erode a significant share of your final wealth. Compare expense ratios, trading costs, and platform fees before committing. The Kenya Money Market Funds yield comparator is a useful reference for the cash sleeve.

7. Stay long-term focused

Markets rise and fall. They have always risen more than they have fallen over meaningful time spans. Stick to the strategy. The timeless wealth lessons from Buffett, Munger, and Dalio all converge on this point.

Inflation, Interest Rates, and Real Returns

A balanced portfolio also has to earn a real return — above inflation. A 7% nominal return in a 4% inflation environment is only 3% in real terms. Two habits help:

- Track inflation versus your yields. The article on Fixed Deposit returns vs inflation is a useful read for savers and bond investors.

- Read the macro backdrop regularly via the Kenyan Economic & Market Outlook, the Global Markets Outlook, and commentary like Fed rate path & yields.

Why Balancing Matters

A balanced portfolio helps you:

- Reduce the impact of any single bad investment

- Control risk so you can stay invested during drawdowns

- Improve long-term return potential by forcing a sell-high, buy-low discipline

- Stay aligned with your financial goals as markets change

Balancing is not about eliminating risk — that is impossible. It is about managing risk intelligently so that time and compounding can do their work.

Final Takeaway: Balancing Is an Ongoing Process

Balancing your portfolio is not a one-time task — it is a habit. Diversify wisely, rebalance regularly, and stay disciplined, and you give yourself a far better chance of long-term financial success. Before you invest, make sure the basics are in place: a fully funded emergency fund, a robust financial safety net, and an automated pay yourself first system that funds your investments every month.

FAQ: Balancing Your Investment Portfolio

What does a balanced portfolio mean?

A balanced portfolio is a diversified mix of assets — typically stocks, bonds, real estate, and cash — structured to deliver steady growth while keeping risk in check. The classic profile is 60/40 (stocks/bonds), but the right mix depends on your goals and risk tolerance.

How often should I rebalance my portfolio?

Once or twice a year is enough for most investors, or whenever any asset class drifts more than 5–10 percentage points from its target. Use a personal finance dashboard to monitor drift without obsessing daily.

Does rebalancing cost me money?

It can incur trading fees or tax on realised gains, but the discipline of systematically selling high and buying low typically outweighs those costs over time. Rebalance inside tax-advantaged or zero-commission platforms where possible to minimise friction.

What is the difference between diversification and rebalancing?

Diversification is about what you own — spreading money across different assets. Rebalancing is about how you maintain those weights over time, trimming winners and topping up laggards so the portfolio stays true to plan.

How does inflation affect my balanced portfolio?

Inflation erodes purchasing power, so always compare nominal returns to the inflation rate. Real returns are what matter. See Serrari’s article on Fixed Deposit returns vs inflation for a worked example in the Kenyan context.

Can I rebalance automatically?

Many unit trusts, robo-advisors, and managed portfolios rebalance automatically on your behalf. If you prefer that hands-off approach, compare managed options on the Serrari Marketplace or consult Serrari Advisory.

Should I rebalance during a market crash?

Yes — and that is precisely when rebalancing hurts the most and helps the most. Buying more of what has fallen feels uncomfortable, but historically it has been the highest-return move. Staying disciplined through volatility is the real edge.

Stay Connected, Keep Growing

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the curated Wealth Builder Guide.

Stay connected to what truly matters. Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter on the Serrari Group homepage.

Growth opens doors. Advance your career through professional programs on Serrari Ed, including ACCA prep courses and the Financial Literacy special offer — designed to move you forward with confidence.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}