Ever wonder where your money really goes? If you have ever reached the end of the month feeling like your income simply evaporated, you are not alone — and you are not stuck. Personal wealth management is the practical discipline of earning, spending, saving, and growing your money so that every shilling, cedi, or naira you earn moves you closer to the life you want.

As Warren Buffett put it: “Do not save what is left after spending; instead spend what is left after saving.” In plain terms — pay yourself first. This guide walks Kenyan, African, and global beginner investors through the fundamentals: why wealth management matters, how to use the 50/30/20 budgeting rule, the real difference between saving and investing, and the smart habits that build lasting security.

Markets move fast; don’t get left behind. Pair the Serrari Group Market Index with a curated Serrari Marketplace and the comprehensive Wealth Builder Course to get the data — and the skills — you need to act on it.

What you’ll learn in this guide

- Why personal wealth management matters at every income level

- How to apply the 50/30/20 budgeting rule with confidence

- The real difference between saving and investing

- How to build smarter financial habits and make better money decisions

Why Personal Wealth Management Matters

Managing your money is not about being rich — it is about being ready. When your finances are organised, you stop reacting to emergencies and start directing your future.

- Handle emergencies such as medical bills, job loss, or urgent repairs without panic

- Maintain your lifestyle through both good and bad months

- Reduce financial stress and free up mental bandwidth for work and family

- Plan for retirement so you can stop working on your own terms

- Leave a legacy — for family, community, or causes you believe in

For the bigger-picture framework on how saving, investing, and insurance fit together, see Serrari’s guide on the financial triangle — the simplest decision framework for anyone starting out. And for advanced allocation, the deeper dive on wealth management, allocation and distribution shows how the pieces scale as your income grows.

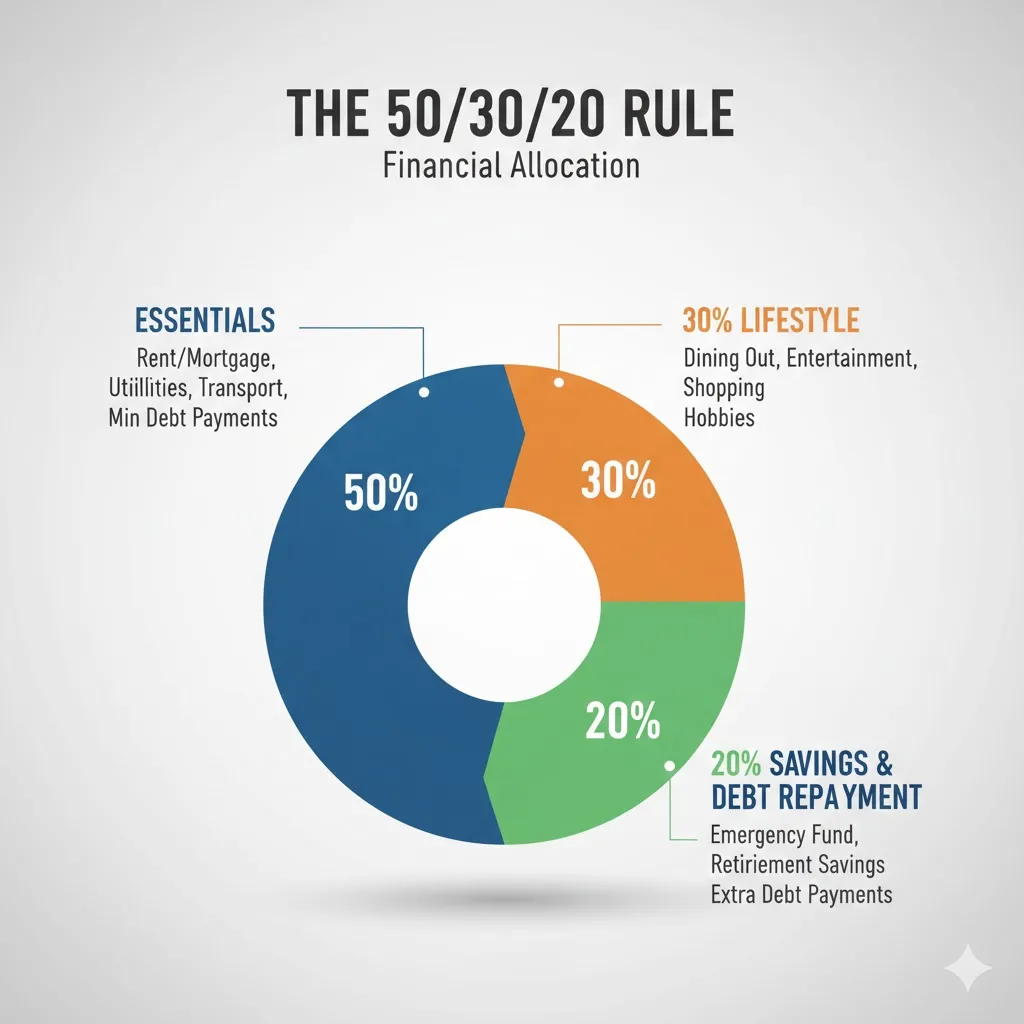

Budgeting Made Simple: The 50/30/20 Rule

Budgeting does not have to be complicated. The 50/30/20 rule splits every shilling of take-home pay into three buckets, so you always know where your money is going.

| Share | Category | What It Covers |

| 50% | Essentials (Needs) | Rent/mortgage, utilities, groceries, transport, insurance, minimum debt payments. |

| 30% | Lifestyle (Wants) | Dining out, entertainment, shopping, hobbies, travel and subscriptions. |

| 20% | Savings & Future | Emergency fund, investments, retirement contributions, extra debt repayment. |

50% — Essentials (Needs)

These are the costs you cannot avoid: rent or mortgage, utilities, groceries, transport, insurance, and the minimum payments on any debt. If your essentials consistently exceed 50% of take-home pay, that is a signal to renegotiate, relocate, or raise income — not to squeeze the other buckets permanently.

30% — Lifestyle (Wants)

Dining out, entertainment, shopping, hobbies, travel, subscriptions. Lifestyle spending matters — money is also a tool for enjoying life — but it is the bucket with the most leakage. Serrari’s breakdown of the 7 ways to stop silent money leaks is the fastest way to reclaim 2–5% of your income without feeling deprived.

20% — Savings and Future

This is where wealth is built: emergency fund, investments, retirement contributions, and extra debt repayment. Make this bucket automatic — a standing order on payday — so you never see the money in your current account. That is the mechanic behind paying yourself first, and why it works.

Context is everything. While you set up your budget, use the Serrari Group Market Index and the Serrari Marketplace to spot emerging shifts, and let the Wealth Builder Guide turn those insights into a professional-grade strategy.

Saving vs Investing: What’s the Difference?

Many people use the words saving and investing interchangeably — but they serve very different purposes. Getting the distinction right is one of the fastest upgrades you can make to your financial life. For a short, clear primer, Serrari’s guide to the difference between saving, investing, and insurance is a perfect companion to this section.

Saving = Safety

Saving means setting money aside in safe, easily accessible accounts. It is ideal for short-term goals (0–3 years) and for emergencies. Key traits:

- For emergencies: money set aside for the unexpected — accidents, medical bills, urgent repairs

- Short-term goals: a holiday, a laptop, a wedding, a deposit

- Low risk: your principal is protected and unlikely to lose value

- Easy access: you can get to the money within days, often same-day

Think: an emergency fund of 3–6 months of essential expenses, parked in a high-yield money market fund. Serrari’s emergency fund simple guide and the broader financial safety net show you exactly how to build it. Compare yields on the Kenya Money Market Funds comparator.

Investing = Growth

Investing means putting money into assets — stocks, bonds, unit trusts, real estate, ETFs — so that it grows over time. It is the engine behind every retirement plan, every property portfolio, and every long-term wealth story. Key traits:

- For long-term goals: retirement, buying a home, funding children’s education, financial independence

- Higher potential returns: over decades, diversified portfolios outpace savings accounts many times over

- More risk: prices fluctuate; in any single year you could be down

- Compounding: the longer you invest, the more powerful returns-on-returns become

New to investing? Start with Serrari’s Investing Explained: a beginner’s guide to growing wealth before picking any product.

Saving vs Investing at a Glance

| Dimension | Saving | Investing |

| Purpose | Protect money for short-term needs and emergencies | Grow wealth over long time horizons |

| Time Horizon | 0–3 years | 5+ years |

| Risk Level | Very low | Moderate to high (market-dependent) |

| Typical Return | Low (bank interest, MMF yields) | Higher potential returns, with volatility |

| Examples | Savings account, money market fund, fixed deposit | Stocks, bonds, unit trusts, real estate, ETFs |

Should You Save or Invest?

The honest answer: both — in the right order, at the right proportions. The right mix depends on four things:

- Your time horizon — when do you need the money?

- Your goals — emergency fund, home deposit, retirement, legacy?

- Your risk tolerance — how much volatility can you live with?

- Your financial situation — income stability, debt load, dependents

A simple, battle-tested sequence for beginners:

- 1. Build a starter emergency fund of one month’s essentials in a money market fund

- 2. Pay off high-interest debt (credit cards, mobile loans) aggressively

- 3. Grow the emergency fund to 3–6 months of essentials

- 4. Start investing for long-term goals — retirement, property, children’s education

- 5. Review and rebalance at least annually

Map this sequence onto a one-page view with Serrari’s guide on building a personal finance dashboard, and tie it to concrete milestones using the wealth goals & vision board framework.

Take Control of Your Financial Future

Personal wealth management is not about being wealthy today — it is about being prepared for tomorrow. When you budget wisely, save consistently, and invest strategically, you build security, confidence, and long-term financial freedom. These three habits compound faster than any hot tip ever will. The timeless wealth lessons from Buffett, Munger, and Dalio all point back to the same truth: consistent behaviour beats clever strategy.

If your situation is complex — multiple income streams, business interests, cross-border family — consider speaking with Serrari Advisory for guidance tailored to your goals.

FAQ: Personal Wealth Management for Beginners

What is personal wealth management in simple terms?

Personal wealth management is the ongoing process of planning, growing, and protecting your money so it supports the life you want. It covers budgeting, saving, investing, insurance, and long-term planning. For a beginner-friendly walkthrough, see the ABCs of Personal Finance on Serrari Ed.

How does the 50/30/20 rule work for Kenyan and African earners?

Take your monthly take-home pay and divide it into three buckets: 50% for essentials (rent, utilities, groceries, transport), 30% for wants, and 20% for savings and debt repayment. In high cost-of-living cities, essentials may briefly exceed 50% — treat that as a temporary setup and adjust by raising income, relocating costs, or trimming fixed expenses.

Should I save or invest first?

Save first — but only until you have a basic safety net. Build a 3–6 month emergency fund, pay off high-interest debt, and then channel long-term money into investments. Serrari’s financial triangle framework explains why the order matters.

Where should I keep my emergency fund?

Keep it somewhere safe, liquid, and productive — typically a money market fund (MMF), which in Kenya often yields 12–16% annually while remaining accessible within 1–3 business days. Compare yields and fees on the Kenya Money Market Fund comparator and the Serrari Marketplace.

How much should I invest as a beginner?

Start with what you can sustain — even 5–10% of take-home pay is a strong beginning if it is consistent. Increase the amount by 1–2 percentage points each year or with every pay rise. The habit is worth more than the amount in year one.

What if I can’t save 20% right now?

Start smaller. Save 5% automatically, then raise the rate by 1% each quarter. Meanwhile, plug the silent money leaks that quietly drain your budget — that alone usually unlocks another 3–5%.

When should I talk to a financial advisor?

Consider professional advice when you have a complicated income structure, are starting or selling a business, receive a windfall, or feel stuck despite saving. Serrari Advisory offers personalised guidance for African and Kenyan investors.

Stay Connected, Keep Growing

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the curated Wealth Builder Guide.

Stay connected to what truly matters. Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter on the Serrari Group homepage.

Growth opens doors. Advance your career through professional programs on Serrari Ed, including ACCA prep courses and the Financial Literacy special offer — designed to move you forward with confidence.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}