Rising California home insurance rates are expected to deliver the largest premium increases in the United States during 2026. According to projections, homeowners in the state will face a 16% increase in premiums as insurers respond to growing losses from natural disasters, particularly the devastating wildfires that struck Southern California in 2025.

Key Overview

- California homeowners are projected to face a 16% increase in insurance premiums in 2026.

- The increase is the largest among all U.S. states.

- The national average increase is estimated at 4%.

- Average annual premiums in California are projected to reach $2,843.

- FAIR Plan premiums are expected to rise by 29%.

- Wildfires in Southern California caused more than $250 billion in damage during 2025.

- California policies typically provide $488,000 in coverage.

- Median home prices in California stand at $854,000.

- Around 11% of California homeowners have no insurance coverage.

- Severe weather caused over $52 billion in insured losses across the U.S. during 2025.

California Home Insurance Costs Expected to Rise Sharply in 2026

The outlook for California home insurance costs points to another challenging year for property owners as insurers adjust pricing to reflect mounting risks and escalating claims.

Industry projections indicate that California homeowners will experience the largest premium increase in the country during 2026, with average insurance costs expected to climb by 16%.

The increase is four times higher than the national average rise of approximately 4%, highlighting the growing pressure facing the state’s insurance market.

Years of catastrophic weather events and rising property losses have contributed to higher costs, with the destructive Southern California wildfires of 2025 representing the latest and most significant example.

As insurers reassess risk exposure, homeowners are increasingly confronting higher premiums and reduced coverage options.

California Home Insurance Rates Rising Faster Than National Average

Projected California home insurance rates are increasing at a much faster pace than those seen across most other states.

The expected 16% increase places California at the top of the national ranking for premium growth.

By comparison, Nebraska is projected to experience a 13% increase, followed by New Mexico at 11% and Georgia at 10%.

Some states are even expected to see lower insurance costs.

Premiums are forecast to decline by approximately 2% in Hawaii and Massachusetts, while Maine could experience a 1% decrease.

The divergence reflects the different risk profiles faced by insurers in various regions.

California’s growing exposure to wildfire losses and rising reconstruction costs continues to place upward pressure on insurance pricing.

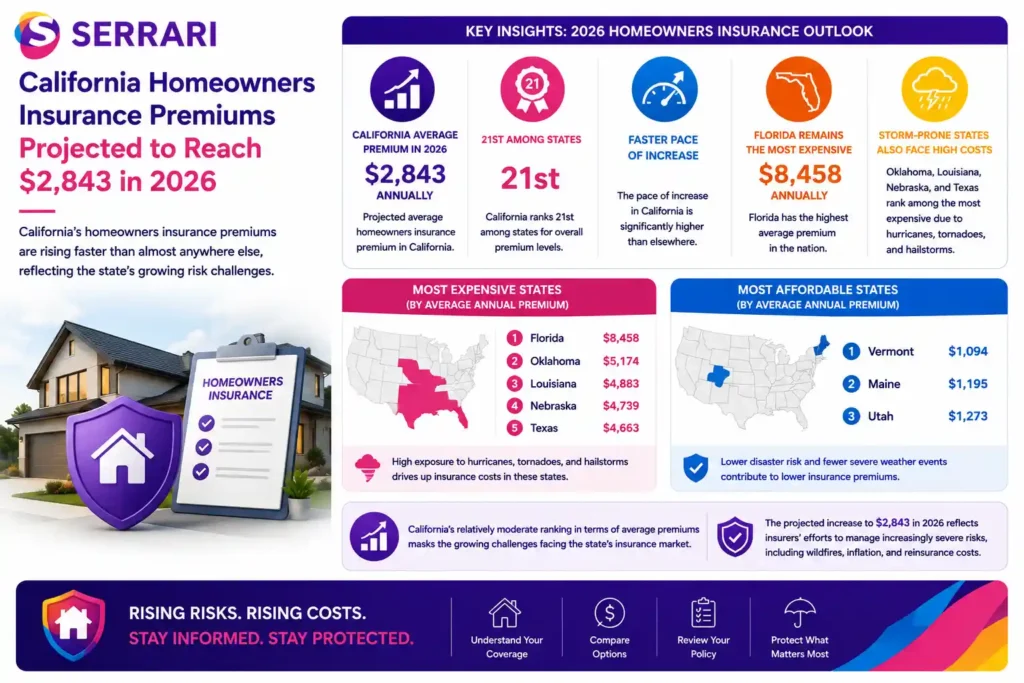

Homeowners Insurance California Premiums Reach $2,843

Average homeowners insurance California premiums are projected to reach $2,843 annually during 2026.

Although this places California only 21st among states in terms of overall premium levels, the pace of increase is significantly higher than elsewhere.

Florida remains the most expensive state for homeowners insurance, with annual premiums averaging $8,458.

Oklahoma, Louisiana, Nebraska, and Texas also rank among the most expensive markets because of their exposure to hurricanes, tornadoes, and hailstorms.

At the opposite end of the spectrum, Vermont has the lowest average premium at $1,094, followed by Maine and Utah.

California’s relatively moderate ranking in terms of average premiums masks the growing challenges facing the state’s insurance market.

The latest increase reflects insurers’ efforts to manage increasingly severe risks.

Home Insurance Premiums Face Pressure From Wildfires

The rise in home insurance premiums has been heavily influenced by natural disasters.

Wildfires across Southern California in 2025 caused more than $250 billion in damage, creating enormous financial losses for insurers and property owners.

These events added to years of escalating claims linked to climate-related risks and rising rebuilding costs.

Across the United States, severe convective storms—including tornadoes, hailstorms, and wind events—generated more than $52 billion in insured losses during 2025.

That figure represented the third-highest total ever recorded.

The increasing frequency and severity of catastrophic events have forced insurers to reprice risk and reevaluate their exposure in vulnerable regions.

For California, wildfire risks remain one of the primary drivers behind rising premiums.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

California Insurance Market Faces Growing Challenges

The broader California insurance market continues to face structural pressures.

Some property owners are struggling to obtain coverage from traditional insurers as companies reduce exposure or limit new policies in high-risk areas.

As a result, more homeowners are turning to California’s FAIR Plan, which serves as an insurer of last resort.

Premiums within the FAIR Plan are projected to increase by 29% next year, significantly exceeding the average market increase.

The growing reliance on the FAIR Plan highlights concerns about coverage availability and affordability.

Regulators and industry participants continue seeking solutions that balance consumer protection with insurers’ ability to operate sustainably.

However, rising climate risks and rebuilding costs continue to complicate these efforts.

Property Insurance Costs Reflect High Home Values

Rising property insurance costs are also influenced by California’s exceptionally high property values.

The state has the highest median home price in the country at approximately $854,000, exceeding Hawaii—the second-most expensive market—by around $80,000.

Higher home values translate into larger replacement costs and greater insured exposure.

According to Insurify, California homeowners typically carry policies covering approximately $488,000 in repairs, the second-highest level nationally after Hawaii.

This figure is 43% above the national average of $342,000.

Despite higher coverage levels, Californians pay roughly 0.6% of the insured value in premiums, below the national average ratio of 0.9%.

This suggests that premium increases partly reflect the high cost of protecting valuable assets.

Homeowners Insurance Premiums and Coverage Gaps

Growing homeowners insurance premiums have contributed to concerns about underinsurance and uninsured properties.

According to LendingTree estimates, approximately 11% of California homeowners do not carry insurance coverage.

Although this figure is below the national average of 14%, it still represents a significant number of uninsured homes.

The absence of coverage creates financial risks for homeowners, particularly in regions vulnerable to wildfires and natural disasters.

West Virginia records the highest share of uninsured homeowners at 24%, followed by New Mexico and Louisiana.

States such as Colorado, Oregon, and New Hampshire report the lowest rates of uninsured properties.

The data highlights the importance of maintaining adequate protection despite rising costs.

Why Insurance Costs Are Rising

Several factors are contributing to higher premiums in California.

Catastrophic wildfires remain the most visible challenge, but broader economic factors also play a role.

Rising construction costs, labor shortages, inflation, and elevated electricity prices all contribute to increased rebuilding expenses.

California’s electricity prices have remained among the highest in the country for decades, according to the Public Policy Institute of California.

Combined with soaring property values, these factors increase the cost of replacing damaged homes and drive higher insurance claims.

Insurers are adjusting premiums accordingly to ensure long-term financial sustainability.

Conclusion

The outlook for California home insurance costs highlights the growing financial challenges facing homeowners. With premiums projected to increase by 16% in 2026—the largest increase in the United States—property owners are confronting the combined effects of wildfire risks, rising home values, and escalating rebuilding costs.

While California’s average premium levels remain below those of several disaster-prone states, the pace of increase underscores the mounting pressures within the insurance market. As climate risks continue evolving, homeowners, insurers, and regulators will need to adapt to a landscape characterized by higher costs and greater uncertainty.

FAQs

1. Why are California home insurance costs rising so quickly?

California home insurance costs are rising primarily because of increasing wildfire risks, higher rebuilding expenses, and growing claims related to natural disasters. The devastating Southern California wildfires of 2025 caused more than $250 billion in damage, adding further pressure to insurers and contributing to higher premiums.

2. How much will homeowners insurance cost in California in 2026?

According to projections, the average annual homeowners insurance premium in California will reach approximately $2,843 in 2026. Although this is not the highest premium level in the country, California is expected to experience the largest percentage increase among all states.

3. What is the California FAIR Plan?

The California FAIR Plan provides insurance coverage to homeowners who are unable to obtain policies from traditional insurers. It serves as an insurer of last resort and has become increasingly important as some insurers reduce their exposure in high-risk areas. FAIR Plan premiums are expected to increase by 29% next year.

4. Are California homeowners paying more relative to coverage?

Despite rising premiums, Californians still pay a relatively low premium-to-coverage ratio compared with the national average. Typical policies provide approximately $488,000 in coverage, while premiums represent around 0.6% of insured value, which is below the national average ratio of 0.9%.

Source: Yahoo Finance, San Diego Union Tribune, The Hill, The Orange County Register

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}