The Bank of England stablecoin rules establish the UK’s final policy framework for sterling stablecoins used in retail payments. The new regime replaces proposed individual holding caps with a £40 billion issuance limit per stablecoin, adjusts reserve asset requirements, and strengthens UK stablecoin regulation to support innovation while safeguarding financial stability. The rules are expected to enable regulated sterling stablecoins to begin operating from 2027.

Key Overview

- The Bank of England published its final policy and draft rules for sterling stablecoins.

- Individual holding limits were replaced with a £40 billion issuance cap per stablecoin.

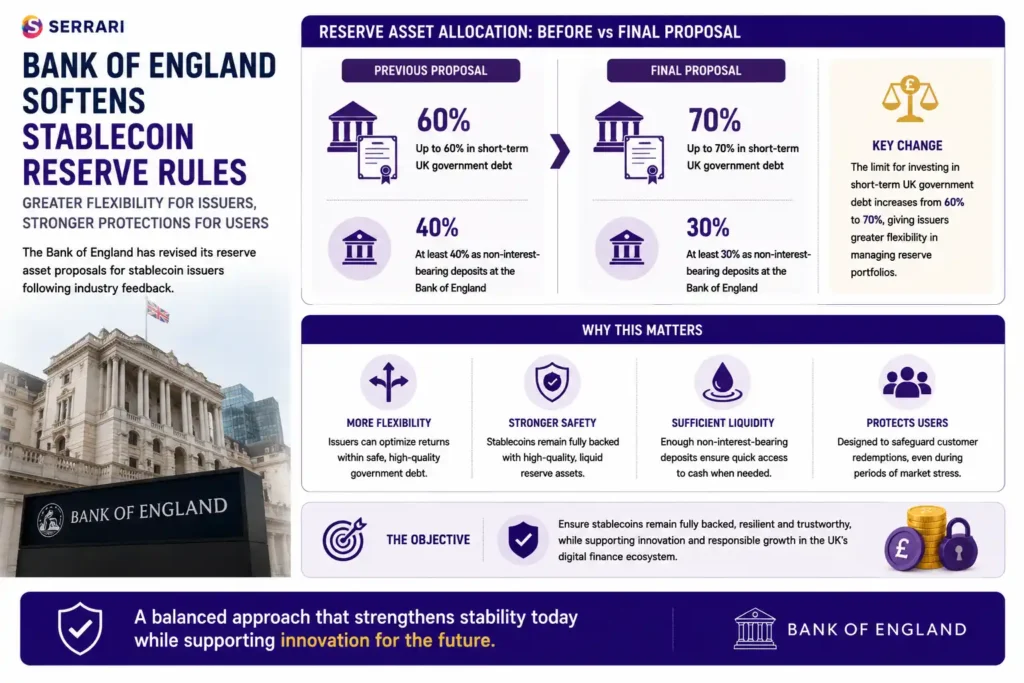

- Stablecoin issuers may invest up to 70% of reserves in short-term government debt.

- The remaining 30% of reserves must be held in non-interest-bearing Bank of England deposits.

- The framework is designed for sterling stablecoins used in retail payments.

- The Bank of England is accepting industry feedback until September 22.

- Regulated sterling stablecoins are expected to launch from 2027.

- Industry groups have raised concerns about the commercial competitiveness of the proposed framework.

Bank of England Stablecoin Rules Create New Framework for Digital Payments

The Bank of England stablecoin rules mark a major step toward establishing a regulated market for sterling-backed stablecoins in the United Kingdom. By publishing its final policy position alongside draft supervisory rules, the central bank has outlined how stablecoins can operate safely within the UK’s financial system while supporting innovation in digital payments.

The new framework is intended for sterling stablecoins that could become widely used for everyday retail payments. Rather than restricting how much individuals can own, the Bank of England has shifted its focus toward limiting the overall size of each stablecoin issuer, reflecting a more system-wide approach to managing financial risk.

Bank of England Replaces Holding Caps with Issuance Limits

One of the most significant changes under the new Bank of England stablecoin policy is the removal of proposed limits on individual holdings.

Earlier proposals considered restricting the amount of stablecoins that consumers could own. Following industry consultation, the Bank instead adopted an issuance-based approach.

Under the revised framework:

- Each regulated sterling stablecoin will initially be limited to £40 billion in total issuance.

- Individual users will not face restrictions on the amount of stablecoins they can hold.

- The issuance limit allows regulators to monitor systemic growth while maintaining flexibility for consumers and businesses.

This approach aims to balance innovation with effective risk management as stablecoin adoption expands across the UK economy.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Reserve Requirements Become More Flexible

The Bank of England also modified its reserve asset proposals following feedback from industry participants.

Previously, issuers would have been allowed to invest only 60% of reserve assets in short-term UK government debt.

The final proposal increases that limit to 70%, giving issuers greater flexibility in managing their reserve portfolios.

The remaining 30% of reserves must continue to be held as non-interest-bearing deposits at the Bank of England.

According to the central bank, this structure seeks to ensure that stablecoins remain fully backed while preserving sufficient liquidity to meet customer redemptions during periods of market stress.

Financial Stability Remains the Primary Objective

The updated stablecoin regulation UK framework places financial stability at the centre of the regulatory approach.

As stablecoins become increasingly integrated into payment systems, regulators want to ensure they do not create risks similar to those experienced during previous financial crises.

By requiring high-quality reserve assets and limiting overall issuance, the Bank aims to reduce the likelihood that stablecoin failures could disrupt payment systems or undermine confidence in digital money.

The framework also establishes supervisory expectations that allow regulators to monitor stablecoin issuers as they grow, helping identify emerging risks before they become systemic.

UK Seeks to Catch Up with Global Stablecoin Regulation

The publication of the final policy represents an important milestone in the UK’s broader digital asset regulation agenda.

Until now, stablecoins in the United Kingdom have largely been regulated through rules covering anti-money laundering, financial promotions and consumer protection.

By comparison, the European Union introduced its comprehensive Markets in Crypto-Assets (MiCA) framework in December 2024, creating a dedicated regulatory regime for stablecoin issuers across member states.

The Bank of England’s new framework brings the UK closer to international regulatory standards while tailoring the rules specifically to the country’s financial system.

Industry Raises Commercial Concerns

Despite welcoming greater regulatory certainty, several industry participants have expressed concerns about aspects of the proposed framework.

The primary issue relates to the requirement that 30% of reserve assets remain in non-interest-bearing deposits at the Bank of England.

Industry representatives argue that this portion of reserves generates no investment income, potentially reducing profitability for sterling stablecoin issuers compared with competitors operating under other regulatory regimes.

Some believe this could make UK-issued stablecoins less commercially attractive than US dollar or euro-denominated alternatives, particularly in international markets where issuers compete on efficiency and returns.

These concerns are likely to remain part of the consultation process before the framework is fully implemented.

Feedback Process Continues Before Implementation

Although the Bank has described its policy position as final, the regulatory process has not yet concluded.

The Bank of England is continuing to accept feedback from industry participants until 22 September, specifically requesting comments on any remaining implementation challenges.

This final consultation period allows payment firms, financial institutions and digital asset companies to highlight practical issues before the supervisory framework becomes operational.

The collaborative approach reflects the rapidly evolving nature of digital asset markets and the importance of ensuring regulations remain effective without unnecessarily restricting innovation.

Regulated Sterling Stablecoins Expected in 2027

The Bank of England expects the new UK stablecoin rules to support the launch of regulated sterling stablecoins from 2027.

Once implemented, the framework could enable banks, payment providers and financial technology companies to issue fully regulated digital pounds backed by high-quality reserve assets.

These stablecoins could improve payment efficiency, support faster settlements, reduce transaction costs and contribute to the UK’s broader digital finance strategy.

As global interest in stablecoins continues to accelerate, the UK’s regulatory framework positions the country to participate more actively in the growing digital payments ecosystem while maintaining a strong focus on financial stability.

Conclusion

The Bank of England stablecoin rules establish the UK’s first comprehensive framework for sterling stablecoins designed for retail payments. By replacing individual holding caps with issuance limits, revising reserve requirements and prioritising financial stability, the Bank seeks to balance innovation with effective risk management. While industry participants continue to debate the commercial impact of the reserve rules, the framework provides much-needed regulatory clarity ahead of the expected launch of regulated sterling stablecoins in 2027.

FAQs

1. What are the new Bank of England stablecoin rules?

The Bank of England stablecoin rules establish how sterling-backed stablecoins intended for widespread retail payments will be regulated in the UK. The framework replaces proposed limits on individual holdings with a £40 billion issuance cap for each stablecoin, while setting detailed reserve asset requirements designed to ensure issuers can meet redemption requests. The rules also strengthen supervisory oversight as part of the UK’s broader effort to create a secure and well-regulated digital asset ecosystem.

2. Why did the Bank of England remove individual holding caps?

The Bank decided that limiting the total size of each stablecoin would be more effective than restricting how much individual consumers could own. An issuance cap allows users and businesses to adopt stablecoins without personal ownership limits while enabling regulators to monitor systemic risks as the market grows. This approach is intended to encourage innovation and competition while preserving financial stability across the wider payments system.

3. How will stablecoin reserves be managed under the new rules?

Under the final UK stablecoin regulation, issuers will be permitted to invest up to 70% of their reserve assets in short-term UK government debt, an increase from the previously proposed 60% limit. The remaining 30% must be held in non-interest-bearing deposits at the Bank of England. These reserve requirements are designed to ensure that stablecoins remain fully backed by highly liquid assets, allowing issuers to honour redemption requests even during periods of market stress.

4. When will regulated sterling stablecoins become available in the UK?

The Bank of England expects regulated sterling stablecoins operating under the new framework to begin launching from 2027, subject to the completion of the regulatory process and industry readiness. Before implementation, the Bank is continuing to gather feedback from financial institutions, payment providers and digital asset firms until September 22. Once the framework is fully in place, regulated stablecoins could play a larger role in retail payments, digital commerce and the UK’s broader digital finance strategy.

Sources: Reuters, Yahoo Finance, The Star, Global Government Finance, Bank of England

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}