Introduction

Not every investment should serve the same purpose — and that is exactly where most investors go wrong. Investing for retirement is fundamentally different from investing for a house deposit, and using the same tool for both often leads to disappointing outcomes. The most common mistake? Choosing investment products based on popularity or what a friend recommended, rather than matching the tool to the specific goal it needs to achieve.

Smart investing is goal-aligned. It starts with understanding what you want your money to do, how long you can leave it invested, and how much risk that timeline allows. This guide walks you through exactly how to match investment tools to five distinct financial purposes — from short-term capital preservation to aggressive long-term wealth growth.

Markets move fast, and acting on the right information at the right time is what separates intentional investors from reactive ones. The Serrari Group Market Index tracks live yields, interest rates, and market movements across Kenya, Africa, and global markets daily. Pair that real-time data with the Serrari Wealth Builder Marketplace — where you can compare over 160 investment products side by side — and the Wealth Builder platform to build a strategy backed by data, not guesswork.

What You Will Learn

By the end of this guide you will understand which investment tools are best suited for short-term, medium-term, and long-term goals, how your time horizon fundamentally changes your investment strategy, how to balance growth and stability within a single portfolio, and how to use a layered investment model that protects your capital while still building wealth.

Investing for Short-Term Goals (0–2 Years)

When You Need Your Money Soon

Examples: A wedding fund, business startup capital, a car purchase, a travel fund, or an emergency savings buffer.

Best investment tools: Money market funds, treasury bills, and short-term bonds. These instruments are designed for capital preservation — your primary concern over a short horizon is not high growth, but making sure the money is there when you need it, with modest returns that at minimum outpace inflation.

Money market funds in Kenya currently yield between 8–12% annually, significantly more than a standard savings account, while still allowing you to withdraw your funds within one to three business days. Treasury bills (91-day, 182-day, or 364-day) offer government-backed returns with virtually zero default risk, though your capital is locked until maturity.

What to avoid: Stocks, equity funds, or any high-volatility asset. A market downturn in the wrong month could wipe out 15–20% of your short-term fund right when you need it most.

If you are weighing your short-term options, the guide Which Saving Tool Fits Your Goal? provides a practical framework for matching specific saving tools to specific timelines. You can also compare every money market fund available in Kenya — with live yields, fees, and minimum investments — in the Serrari Marketplace.

Investing for Medium-Term Goals (2–5 Years)

When You Can Afford to Wait — But Not Too Long

Examples: A home deposit, business expansion capital, a child’s secondary school or university education fund, or building a major purchase fund.

Best investment tools: Balanced mutual funds, government and corporate bonds, and diversified portfolios that combine fixed-income instruments with a measured equity allocation. The goal here is moderate growth with controlled risk — you want your money to grow faster than inflation, but you cannot afford a catastrophic loss two years before you need it.

Bonds provide predictable coupon payments and return your principal at maturity, making them an anchor for medium-term portfolios. Balanced funds add a growth component through partial equity exposure while keeping overall volatility manageable.

What to avoid: Extremely volatile investments, including speculative stocks, cryptocurrency without a hedging strategy, or illiquid real estate where you cannot exit on your timeline.

If you are choosing between treasury instruments and bank-offered products for this timeframe, the comparison Are Treasury Bills Better Than Fixed Deposits in Kenya? lays out the differences clearly.

Investing for Long-Term Goals (5+ Years)

When Time Is on Your Side

Examples: Retirement planning, generational wealth building, financial independence, or a child’s university fund started early.

Best investment tools: Stocks (equities), equity-focused mutual funds, real estate, and diversified long-term portfolios. With a horizon of five years or more, you have the single most powerful advantage in investing — time. Time allows you to absorb short-term market volatility, and it is what makes the power of compounding work in your favour.

Historically, equity markets deliver the highest long-term returns among all asset classes, though individual years can swing dramatically. Real estate in Kenya’s growing urban centres offers dual returns through rental income and property appreciation, though it requires more capital upfront and is inherently illiquid.

The key principle is this: the longer your time horizon, the more risk you can afford to take, because short-term losses have time to recover. An investor saving for retirement in 20 years should not have the same portfolio as someone saving for a wedding in 18 months.

For a comprehensive overview of every investment option available in Kenya today, including entry-level amounts and expected returns, read Best Investments in Kenya 2026: A Beginner’s Guide.

Investing for Income Generation

When You Need Regular Cash Flow

Goal: Generate consistent, recurring income from your portfolio — whether to supplement a salary, fund living expenses in retirement, or create a passive income stream.

Best investment tools: Dividend-paying stocks, government and corporate bonds, real estate rental income, and dedicated income funds. Each of these instruments is designed to produce regular distributions — quarterly dividends, semi-annual coupon payments, or monthly rental income — rather than relying solely on capital appreciation.

The focus here is on stability and recurring returns. You want predictable cash flow, not dramatic growth swings. Bonds are the classic income-generation tool — they pay fixed interest on a known schedule. Dividend stocks from established companies offer growth potential alongside regular payouts. Rental property provides monthly income, though it comes with management responsibilities and liquidity constraints.

If you are not yet sure whether your savings should focus on income or growth, the guide Why Leaving Money in a Savings Account Is Now Costing You explains the real cost of inaction — and why even conservative investors need to move beyond savings accounts.

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder platform turns these insights into a professional-grade strategy.

Investing for Aggressive Wealth Growth

When You Want Maximum Long-Term Capital Appreciation

Goal: Maximize the growth of your portfolio over time, accepting higher volatility in exchange for higher potential returns.

Best investment tools: Individual equities, growth-focused equity funds, and emerging market investments. These instruments prioritise capital appreciation over income generation or capital preservation. They are appropriate when your investment horizon is long, your risk tolerance is high, and you are building wealth rather than drawing from it.

Critical prerequisites before pursuing an aggressive strategy: This approach is only suitable if you already have an adequate emergency fund in place (three to six months of living expenses in a liquid, low-risk account), your essential insurance coverage exists (health, life, and property at minimum), and you have a long enough time horizon — typically seven years or more — to ride out inevitable downturns.

Without these foundations, an aggressive growth strategy becomes reckless speculation. The guide How to Build an Essential Insurance Plan Before It’s Too Late covers the protection layer you should have in place before making aggressive investment moves.

The Time Horizon Rule

Your investment timeline is the single most important variable in determining which tools belong in your portfolio. The principle is straightforward:

| Time Horizon | Primary Objective | Appropriate Risk Level | Best-Fit Tools |

|---|---|---|---|

| Short-term (0–2 years) | Protect capital | Low | MMFs, T-Bills, short-term bonds |

| Medium-term (2–5 years) | Balance risk and growth | Moderate | Balanced funds, bonds, diversified portfolios |

| Long-term (5+ years) | Embrace growth | Higher | Equities, real estate, growth funds |

Time is your most powerful investment tool. The longer your horizon, the more volatility you can absorb, the more compounding works in your favour, and the wider your range of suitable investment options becomes. For a deeper exploration of how to match your tools to your timeline, read How to Choose the Right Investment Tool in Kenya 2026.

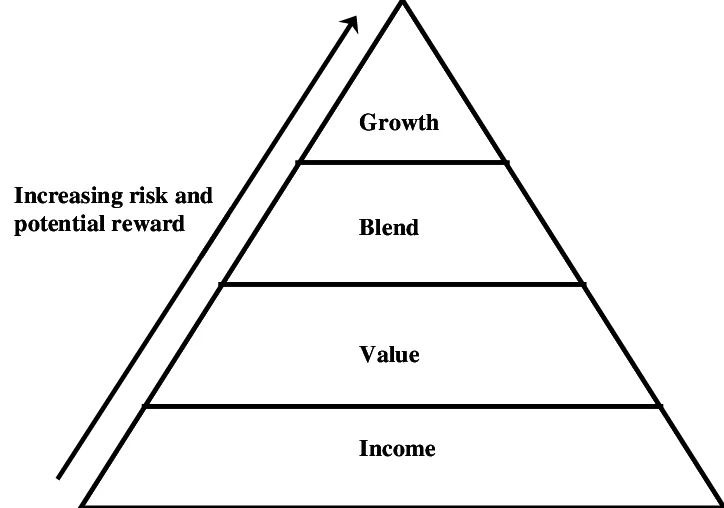

The Layered Investment Model

Rather than placing all your money into a single investment type, the most resilient portfolios are built in layers — each serving a distinct purpose. This is the model that experienced wealth builders and financial advisors across Kenya and Africa use to balance protection, stability, growth, and opportunity.

Layer 1: Liquidity

Tools: Money market funds, high-yield savings accounts, cash equivalents.

Purpose: Immediate access to funds for emergencies and short-term needs. This layer should cover three to six months of essential living expenses. It is not designed to generate high returns — it is designed to be there when you need it. Learn more about building this foundation in Build Your Financial Safety Net: A Simple Guide to Savings.

Layer 2: Stability

Tools: Government bonds, treasury bills, treasury bonds, fixed deposits, and income funds.

Purpose: Predictable, low-volatility returns that anchor your portfolio. This layer generates steady income and protects against market shocks. It is the backbone of a diversified investment plan. Check how safety and returns compare in Are Money Market Funds Safe in Kenya?

Layer 3: Growth

Tools: Stocks, equity mutual funds, exchange-traded funds (ETFs), and balanced growth portfolios.

Purpose: Long-term capital appreciation. This layer is where compounding does its most powerful work, but it requires patience and a tolerance for short-term price swings. It should only be funded with money you will not need for five or more years.

Layer 4: Expansion

Tools: Real estate, business ventures, alternative investments, and emerging market opportunities.

Purpose: Wealth multiplication through higher-risk, higher-reward opportunities. This layer is for capital you can afford to tie up for extended periods — and potentially lose — in pursuit of outsized returns.

Each layer has a role. The Financial Triangle framework is a complementary model that helps investors visualise how protection, savings, and growth work together as three sides of a single wealth-building structure.

Common Purpose Mismatches to Avoid

Many investors underperform not because they choose bad investments, but because they choose the wrong investment for the wrong purpose. Investing short-term funds in volatile stocks is one of the most common and costly errors — a 20% market correction right before you need that money can set your goal back by years.

Equally damaging is keeping long-term funds in low-yield savings accounts. While it feels safe, inflation silently erodes your purchasing power every year. A savings account yielding 3% when inflation runs at 5% means you are losing 2% of your money’s real value annually. Ignoring diversification concentrates all your risk in a single asset class, and choosing tools based on hype or social media trends rather than your personal financial plan leads to impulsive decisions you will likely regret.

Purpose determines placement. Every shilling in your portfolio should have a job description. If you are wondering how much you should be allocating monthly toward your investment goals, the guide How Much Should I Invest Monthly in Kenya? provides clear, practical benchmarks.

Quick Self-Assessment: Is Your Money in the Right Place?

Before committing to any investment tool, answer four questions. First, what is this investment meant to achieve? If you cannot articulate the specific goal, you are investing without direction. Second, when will you need the money? The answer determines your risk tolerance more than any other factor. Third, can you tolerate fluctuations? If a 10% drop in value would cause you to sell in a panic, you need a more conservative allocation. Fourth, does this choice align with your broader financial plan? A single investment should not exist in isolation — it should fit into a structured framework alongside your other financial goals.

If the purpose is not clear, reconsider the tool. And if you are just getting started and need a foundational understanding of how investing works, begin with Investing Explained: A Beginner’s Guide to Growing Wealth.

The Serrari Strategic Investment Formula

Intentional wealth building follows a repeatable process. Start with a clear goal — define exactly what you want the money to do and when. Select the correct tool that matches your goal’s risk and return requirements. Ensure time alignment between your investment horizon and the instrument’s characteristics. Build in diversification so no single market event can derail your plan. And commit to an annual review to rebalance, adjust for life changes, and confirm your strategy still fits your evolving circumstances.

Clear Goal + Correct Tool + Time Alignment + Diversification + Annual Review = Intelligent Wealth Growth

Start Building With Purpose Today

Investing is not about chasing returns. It is about placing your money where it serves a clear, defined purpose. Align your tools with your goals. Allocate with discipline. Review annually. Grow intentionally.

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the Wealth Builder platform.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter.

Growth opens doors beyond investing. Advance your career and sharpen your financial knowledge through professional programs including ACCA, HESI A2, ATI TEAS 7, HESI EXIT, NCLEX-RN, NCLEX-PN, and Financial Literacy — all available through Serrari Online Learning.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within the Serrari Market Index.

Frequently Asked Questions (FAQ)

What is the best investment for a short-term goal in Kenya?

For goals within 0–2 years, money market funds and treasury bills are the best options. They offer higher yields than savings accounts (typically 8–12% for MMFs in Kenya) while preserving your capital and maintaining high liquidity. Compare all available options in the Serrari Marketplace.

How do I invest for retirement in Kenya?

Retirement is a long-term goal (typically 10–30+ years), which means you can afford higher-risk, higher-growth instruments like equities, equity funds, and real estate. The key is to start early, diversify across asset classes, and reduce your equity allocation gradually as you approach retirement age. The Wealth Builder platform helps you track and manage this long-term strategy.

Can I start investing with a small amount in Kenya?

Yes. Many money market funds in Kenya accept minimum investments as low as KES 100 to KES 1,000. You do not need a large sum to begin building wealth. The guide Investing with KSh 500 in Kenya explains exactly how to get started with a small amount.

What is the layered investment model?

The layered model structures your portfolio into four tiers: liquidity (emergency funds in MMFs or cash), stability (bonds and treasury instruments), growth (stocks and equity funds), and expansion (real estate and business ventures). Each layer serves a different purpose, and together they create a resilient, diversified portfolio.

Should I invest in stocks or bonds for a 3-year goal?

For a 3-year horizon, bonds and balanced mutual funds are generally more appropriate than pure equity exposure. Stocks can lose significant value in the short term, and three years may not be enough time to recover from a major downturn. A balanced approach with a heavier weighting toward fixed income is the safer strategy for this timeframe.

How often should I review my investment portfolio?

At minimum, review your portfolio once a year. Life changes (marriage, children, career shifts) and market conditions both warrant reassessment. The annual review is your opportunity to rebalance allocations, confirm your strategy still matches your goals, and adjust for any changes in your risk tolerance or timeline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}