Introduction

Investing is one of the most powerful decisions you can make for your financial future but only if you place your money in the right vehicle. With dozens of investment tools available across Kenya, Africa, and global markets, understanding how each one works, what yield it offers, and how much risk it carries is the difference between building wealth and losing it.

This guide breaks down the most common investment tools from stocks and bonds to money market funds, treasury bills, and real estate and compares them side by side so you can make an informed, confident decision. Whether you are a first-time investor in Nairobi or a seasoned portfolio manager in Lagos, this resource is built to help you match each tool to your financial goals.

Markets move fast, and staying ahead requires more than intuition. The Serrari Group Market Index tracks live yields, rates, and market movements across Kenya, Africa, and global markets daily. Pair that data with the Serrari Wealth Builder Marketplace — where you can compare over 160 investment products — and the comprehensive Wealth Builder platform to turn insight into action.

What You Will Learn

By the end of this guide, you will understand the most common investment tools available in Kenya and across Africa, how yield differs between each of them, the relationship between risk and return explained in plain language, and how to choose the right investment based on your personal financial goals and time horizon.

What Is Yield? Understanding Investment Returns

Yield is the return you earn on your investment over a specific period of time, typically expressed as an annual percentage. If you invest KES 100,000 and earn 10% in a year, your yield is KES 10,000.

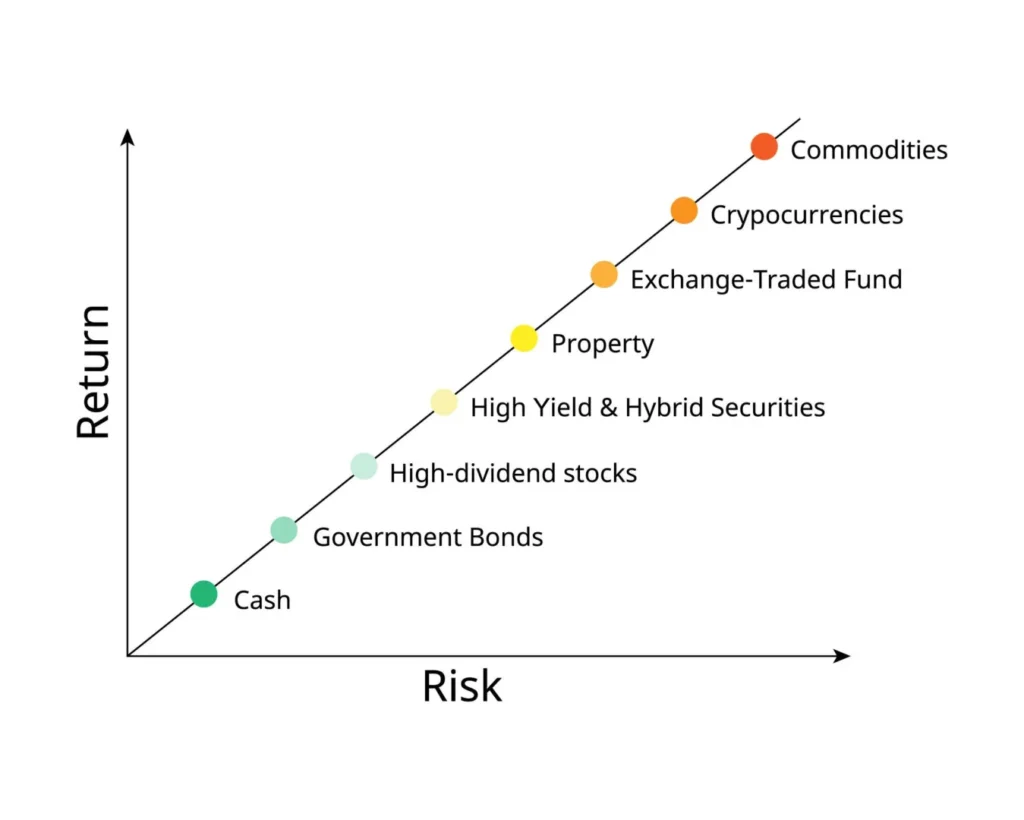

Here is the critical principle every investor should understand: higher yield almost always comes with higher risk. The goal of smart investing is not chasing the highest possible return it is finding the right balance between growth potential and the level of risk you can tolerate.

The best investment strategy is one that aligns your risk appetite with your time horizon and financial objectives — not one that simply promises the highest number.

If you are new to investing and want a foundational understanding of how returns work, the guide Investing Explained: A Beginner’s Guide to Growing Wealth is an excellent starting point.

Common Investment Tools Explained

1. Stocks (Equities)

What they are: When you buy a stock, you purchase an ownership share in a publicly traded company. Your returns come from capital appreciation (the stock price rising) and dividends (profit distributions).

Yield: Potentially the highest among all asset classes over the long term, but returns are volatile and not guaranteed in any given year.

Risk: High. Stock prices fluctuate daily based on company performance, market sentiment, and macroeconomic conditions. You can lose a significant portion of your investment in the short term.

Best for: Long-term wealth building with a horizon of five years or more. Investors who can tolerate short-term volatility in exchange for higher long-term growth potential.

To stay informed on equity market movements across Kenya and Africa, follow the latest investment news and track live index data on the Serrari Market Index.

2. Bonds

What they are: When you buy a bond, you are lending money to a government or corporation in exchange for regular interest payments (coupons) and the return of your principal at maturity.

Yield: Moderate and more predictable than stocks. Government bonds in Kenya typically offer competitive rates that adjust with the Central Bank Rate.

Risk: Lower than equities, but not zero. Bond prices can fall when interest rates rise, and corporate bonds carry the additional risk of default.

Best for: Investors seeking income stability and portfolio diversification, particularly those in or approaching retirement, or anyone who wants a more predictable return stream.

3. Money Market Funds (MMFs)

What they are: Money market funds are professionally managed, low-risk pooled investment vehicles that invest in short-term debt instruments such as treasury bills, commercial paper, and bank deposits.

Yield: Higher than traditional savings accounts but lower than equities. In Kenya, the average MMF yield tracked by the Serrari Market Index currently sits around 8–12% annually depending on the fund.

Risk: Low. These funds are designed for capital preservation with modest growth.

Best for: Short-term investing, emergency fund parking, and investors who need high liquidity — the ability to withdraw funds quickly without penalties.

Wondering whether money market funds are the right fit for you? Read Are Money Market Funds Safe in Kenya? What You Need to Know for a detailed breakdown. You can also compare all available MMFs side by side in the Serrari Wealth Builder Marketplace.

4. Treasury Bills and Treasury Bonds

What they are: Treasury bills (T-Bills) and treasury bonds (T-Bonds) are government-backed securities issued by the Central Bank of Kenya. T-Bills are short-term instruments (91, 182, or 364 days), while T-Bonds have longer maturities ranging from 2 to 30 years.

Yield: Competitive and directly tied to prevailing interest rates. T-Bill rates fluctuate with each auction based on demand and monetary policy.

Risk: Very low. These instruments are backed by the full faith and credit of the government, making them among the safest investment options available.

Best for: Structured short-to-medium-term investing for risk-averse investors, and as a fixed-income anchor in a diversified portfolio.

If you are deciding between treasury instruments and bank deposits, the guide Are Treasury Bills Better Than Fixed Deposits in Kenya? provides a clear comparison to help you decide.

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder platform turns these insights into a professional-grade strategy.

5. Real Estate

What they are: Real estate investments involve purchasing property — residential, commercial, or land — for rental income, capital appreciation, or both. In Kenya’s growing urban centres, property has historically been one of the most popular wealth-building tools.

Yield: Returns come from two sources: recurring rental income and long-term property value appreciation. Net rental yields in Nairobi typically range from 5–8% annually, with additional upside from capital gains.

Risk: Medium to high. Real estate carries market risk (property values can decline), liquidity risk (selling property takes time), and operational risk (management costs, vacancies, and maintenance).

Best for: Long-term wealth builders with capital to deploy and patience to wait for appreciation. Real estate is also a strong hedge against inflation.

Investment Yield Comparison Table

The following table provides a high-level comparison of the five most common investment tools. Use it as a starting framework, and then dive deeper into each category using the resources linked throughout this guide.

| Investment Tool | Risk Level | Liquidity | Potential Yield | Ideal Time Horizon |

|---|---|---|---|---|

| Stocks (Equities) | High | High | High (volatile) | Long-term (5+ years) |

| Bonds | Medium | Medium | Moderate | Medium to Long-term |

| Money Market Funds | Low | High | Moderate (8–12% in Kenya) | Short to Medium-term |

| Treasury Bills & Bonds | Low | Locked until maturity | Moderate (rate-dependent) | Short to Medium-term |

| Real Estate | Medium–High | Low | Moderate to High | Long-term (7+ years) |

Important note: Yields change depending on economic conditions, monetary policy, inflation, and global market dynamics. Always verify current rates using the Serrari Market Index before making investment decisions.

Risk vs. Yield: The Fundamental Truth

The relationship between risk and yield is the single most important concept in investing. Lower-risk instruments like treasury bills and money market funds offer more predictable but modest returns. Higher-risk assets like stocks and real estate offer greater growth potential but come with the possibility of significant short-term losses.

Smart investing is not about chasing the highest yield — it is about aligning risk with your time horizon. If you need money in six months, high-volatility stocks are not appropriate. If you are investing for retirement in 20 years, parking everything in a savings account means you are likely losing purchasing power to inflation. The guide Why Leaving Money in a Savings Account Is Now Costing You explains this dynamic in detail.

How to Choose the Right Investment Tool

Before selecting an investment, ask yourself four key questions:

How long can I leave this money invested? Short-term goals (under 2 years) call for lower-risk, high-liquidity tools like money market funds or treasury bills. Long-term goals (5+ years) allow for higher-growth assets like equities and real estate.

Can I handle fluctuations? If watching your portfolio drop 15% in a bad month would cause you to sell in a panic, you need a more conservative allocation. Emotional resilience is a real factor in investment success.

Do I need steady income or long-term growth? Bonds and MMFs generate more predictable income streams. Stocks and real estate are better for long-term capital appreciation.

Is diversification part of my plan? The most resilient portfolios are not built on a single asset class. Spreading investments across different tools — each with different risk and return profiles — reduces overall portfolio risk.

For a practical framework on matching your savings tools to specific goals, read Which Saving Tool Fits Your Goal? A Practical Guide.

Common Investment Comparison Mistakes to Avoid

Even experienced investors fall into these traps. Comparing yields across different investment tools without accounting for their vastly different risk profiles is misleading. Ignoring fees — management charges, transaction costs, and early withdrawal penalties — can silently erode your real returns over time.

Focusing exclusively on past performance is another common error. A fund that returned 15% last year is not guaranteed to repeat that performance. Investing without diversification exposes you to concentrated risk, and reacting emotionally to short-term market volatility is one of the most expensive mistakes retail investors make.

Yield must always be evaluated alongside stability, fees, and your broader investment strategy.

The Smart Investment Allocation Approach

Rather than placing all your capital into a single investment tool, build a diversified portfolio that includes growth assets like stocks for long-term capital appreciation, stability assets like bonds for predictable income and lower volatility, liquidity tools like money market funds for emergency access and short-term needs, and structured return instruments like treasury bills and bonds for government-backed security.

This balanced approach reduces the impact of any single market shock on your overall portfolio. The Financial Triangle framework is one model that helps investors structure their allocation across protection, savings, and growth.

If you are just starting and wondering how much to set aside, the guide How Much Should I Invest Monthly in Kenya? provides actionable benchmarks for beginners.

Start Building Your Investment System Today

Investing is not about choosing one tool and hoping for the best. It is about building a system — one that balances growth, manages risk, and is reviewed at least annually as your goals and market conditions evolve.

Your financial future is not something you wait for. It is something you build. The real question is: when do you begin?

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the Wealth Builder platform.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter.

Growth opens doors beyond investing. Advance your career and financial knowledge through professional programs including ACCA, HESI A2, ATI TEAS 7, HESI EXIT, NCLEX-RN, NCLEX-PN, and Financial Literacy — all available through Serrari Online Learning.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto landscape — all within the Serrari Market Index.

Frequently Asked Questions (FAQ)

What is the safest investment tool in Kenya?

Treasury bills and treasury bonds are considered the safest investment tools in Kenya because they are backed by the government. Money market funds are also low-risk options that offer higher returns than traditional savings accounts while maintaining high liquidity. You can compare available options in the Serrari Marketplace.

Which investment gives the highest yield in Kenya?

Stocks (equities) and real estate have the highest long-term yield potential in Kenya, though both carry higher risk and volatility. Among lower-risk options, some special funds tracked on the Serrari Market Index offer yields above 15% annually. The right choice depends on your risk tolerance and time horizon.

Are money market funds better than savings accounts?

In most cases, yes. Money market funds in Kenya typically yield 8–12% annually, significantly outperforming traditional savings accounts that often offer 2–5%. MMFs also provide daily liquidity. Read Are Money Market Funds Safe in Kenya? for a complete analysis.

How do I start investing with a small amount in Kenya?

Many money market funds in Kenya accept minimum investments as low as KES 100 to KES 1,000. Treasury bills require a minimum of KES 100,000 at auction. The guide Best Investments in Kenya 2026: A Beginner’s Guide covers all entry-level options and how to get started.

What is the difference between treasury bills and fixed deposits?

Treasury bills are government-backed securities sold through Central Bank auctions, while fixed deposits are offered by commercial banks. T-Bills often offer higher yields and carry sovereign risk (very low), whereas fixed deposit rates vary by bank and are subject to institutional risk. See the detailed comparison in Are Treasury Bills Better Than Fixed Deposits in Kenya?

How do I compare investment products in Kenya?

The Serrari Wealth Builder Marketplace allows you to compare over 160 investment products across money market funds, treasury instruments, fixed deposits, savings accounts, and more — with live yields, fees, and provider details updated daily.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}