Writing a will can feel uncomfortable — but it is one of the most important financial and personal decisions you will ever make. A will turns your wishes into legal instructions, so that your assets, your responsibilities, and the people you care about are handled exactly the way you intend. Without one, the law decides how your estate is distributed, and the outcome rarely matches the life you actually lived.

This guide demystifies will writing for Kenyan, African, and global investors. It covers why a will matters, what to include, how to review and update it, and when to bring in professional help. For the wider framework on how a will sits inside a complete money plan, see Serrari’s pieces on wealth management, allocation and distribution and the financial triangle.

Markets move fast; don’t get left behind. Pair the Serrari Group Market Index with a curated Serrari Marketplace and the comprehensive Wealth Builder Course to make sure you have the data — and the skills — to act on what you see.

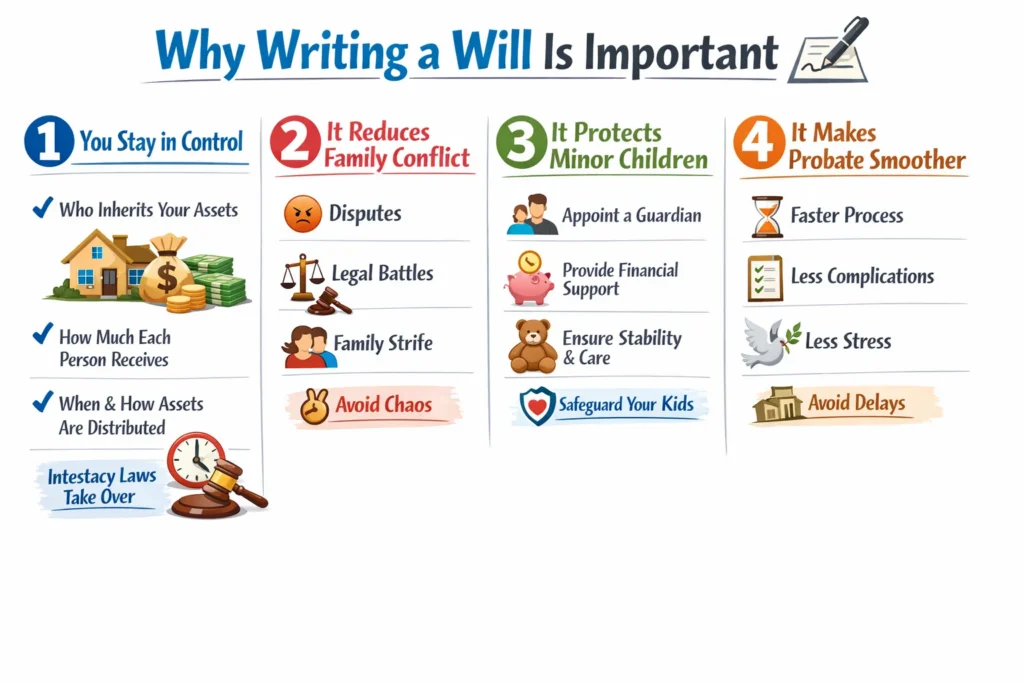

Why Writing a Will Is Important

1. You stay in control

A will lets you decide who inherits your assets, how much each person receives, and when or how the distribution happens. Without one, intestacy laws determine everything — often splitting estates in ways that ignore blended families, dependants you personally supported, or causes you wanted to fund.

2. It reduces family conflict

Most inheritance disputes are the product of ambiguity, not bad faith. A clear will prevents the confusion that leads to arguments, legal battles, and damaged relationships. Serrari’s broader guide on risk management tools is worth reading alongside this: will writing is estate-level risk management.

3. It protects minor children

If you have young children, a will is the only place you can formally appoint a guardian and outline financial support structures for their care. It is often the single biggest reason parents draft a will.

4. It makes probate smoother

Probate is the legal process of validating a will and distributing assets. A well-drafted will speeds up the process, reduces administrative complications, and minimises stress for the people you love. If someone dies without a will in Kenya, the court issues Letters of Administration and the estate is distributed according to statutory rules — usually slower and often at odds with the deceased’s real intentions.

With a Will vs Without a Will

| Dimension | With a Valid Will | Without a Will (Intestate) |

| Who decides distribution | You do — through your written instructions | The law decides, via statutory inheritance rules |

| Speed of asset transfer | Faster probate and clearer execution | Slower — court issues Letters of Administration |

| Guardianship of children | You appoint the guardian you trust | Court decides — often with family disputes |

| Family conflict risk | Low when wishes are clearly written | High — ambiguity fuels disputes |

| Tax and liability efficiency | Can be planned to reduce taxes and delays | Default outcome — often less efficient |

| Business continuity | Shares and roles transfer according to plan | Business can stall or be forced into sale |

Context is everything. While you follow today’s updates, use the Serrari Group Market Index and the Serrari Marketplace to spot emerging shifts. Need to sharpen your edge? The Wealth Builder Course turns these insights into a professional-grade strategy.

What to Include in Your Will

Choose an Executor

Your executor is the person who will administer your estate. Choose someone trustworthy, organised, and financially literate — or a professional executor for complex estates. Their responsibilities typically include:

- Handling paperwork and applying for probate

- Paying outstanding debts, duties, and any taxes

- Distributing assets according to your instructions

- Ensuring every wish in the will is carried out

Clearly Identify Beneficiaries

Vague language breeds disputes. Instead of writing “my assets” or “my money,” state exact amounts, specific properties, named accounts, and named individuals or organisations. If you want charitable giving, name the charity and the purpose. If you want to exclude someone, consider saying so explicitly so the document cannot be easily contested.

Address Special Situations

Complex situations need extra thought (and usually professional help):

- Dependents with special needs — special-needs trusts preserve eligibility for support while providing income

- Business ownership — align your will with shareholder or partnership agreements. See Serrari’s business financial planning and financial risk management for context

- Shared property — joint tenancy vs. tenancy-in-common has very different estate consequences

- Complex financial assets — REITs, global index funds, T-Bonds, pensions, insurance policies and digital assets each require explicit treatment. See Treasury Bonds in Kenya, Kenya’s REIT surge, and best private pension fund in Kenya for product context

Plan for Taxes and Liabilities

A well-drafted will can reduce unnecessary estate taxes, plan for orderly debt settlement, and avoid delays in asset transfer. Life insurance is a powerful tool here because it creates immediate, tax-efficient liquidity for heirs. See Serrari’s insurance and risk protection guide.

Full Will-Writing Checklist

| Element | What to Include |

| Executor | Trustworthy, organised, financially literate person (or professional) who will handle paperwork, pay debts and taxes, and distribute assets |

| Beneficiaries | Named individuals or organisations with specific assets or amounts — avoid vague phrases like “my assets” |

| Guardians | Guardian and backup guardian for minor children; financial arrangements for their care and education |

| Specific bequests | Named properties, vehicles, shareholdings, collections, and heirloom items |

| Residuary clause | Who receives anything not specifically named (a catch-all to avoid gaps) |

| Special situations | Dependents with special needs, business ownership, shared property, cross-border assets, complex financial instruments |

| Debts and taxes | Instructions on how debts, duties, and any estate taxes should be settled |

| Witnesses and signatures | Legally required witness signatures (typically two) and clear dating |

| Safe storage | Original in a safe place; executor and family know where to find it |

A simple asset register — every account, property, policy, investment, and password your executor will need — makes a will hugely more actionable. Keep it alongside your personal finance dashboard and update both every time your finances change.

Review and Update Your Will Regularly

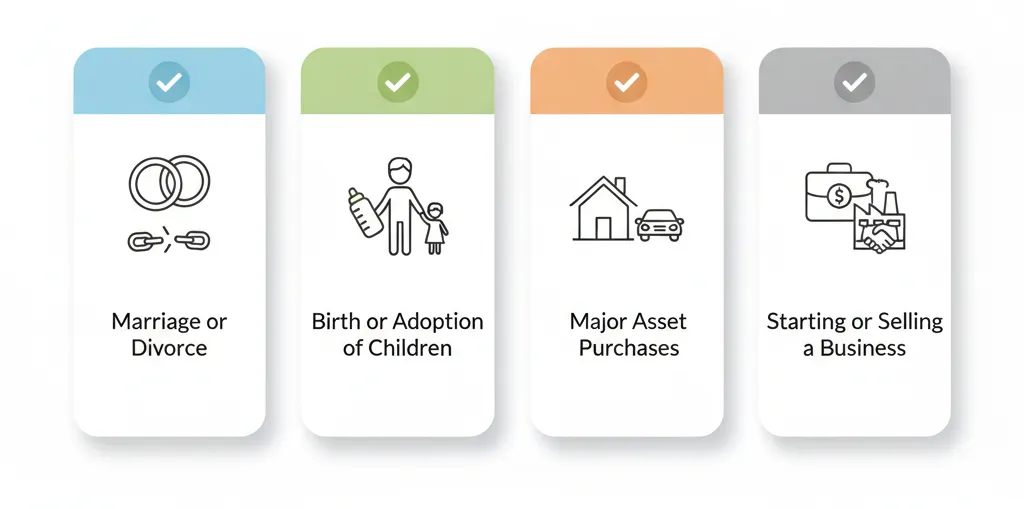

Life changes; your will should too. Update it after any of these events:

- Marriage or divorce

- Birth or adoption of children

- Death of a named beneficiary or executor

- Major asset purchases or sales (a home, business, significant investment)

- Starting, acquiring, or selling a business

- Relocation — especially across borders where inheritance laws differ

A best-practice cadence is a full review every one to two years, in the same way you would review your personal finance plan. Outdated wills can be worse than no will at all, because they may distribute assets to people or entities that no longer exist.

When Professional Guidance Is Worth It

Simple wills can be drafted independently using reputable templates, but some situations almost always benefit from professional advice:

- Blended families, minor children, or dependants with special needs

- Significant business interests or shareholder agreements

- Cross-border assets or foreign beneficiaries

- Potential estate-tax exposure

- Complex trust structures or charitable bequests

Professional drafting ensures legal validity, clear execution, and reduced risk of disputes. Serrari Advisory can coordinate with qualified legal and tax counsel, and help align your will with the wider For Individuals and For Small Business framework.

How a Will Connects to the Rest of Your Money

A will is a legal document, but it does not stand alone. It works best as part of a complete money plan:

- A financial safety net and a 3–6 month emergency fund keep the family afloat during probate delays

- Consistent allocation through Pay Yourself First is what actually builds the estate the will then distributes

- Thoughtful investment and capital allocation determines how much value there is to transfer

- Insurance — understood through Serrari’s insurance and risk protection — provides the immediate liquidity your will needs to work smoothly

The timeless wealth lessons and surprising golden rule of wealth both keep returning to the same point: consistent behaviour over decades is what builds legacies — a will simply makes sure the legacy lands where you want it to.

The Bigger Picture: Will Writing Is About Love, Not Death

Writing a will is not about expecting the worst. It is about protecting the people you love, preserving the wealth you have worked to build, and ensuring your legacy is honoured the way you intend. A well-prepared will gives you four things that money alone cannot:

- Control over who inherits what and when

- Clarity for the people left to interpret your wishes

- Protection for dependants, minors, and special-needs beneficiaries

- Peace of mind for you, today

It is one of the strongest financial decisions you can make for those you care about most.

FAQ: Will Writing

What happens if I die without a will in Kenya?

Your estate is treated as intestate, and the court issues Letters of Administration to appointed administrators. Assets are distributed under the statutory rules of succession, which may not reflect your personal wishes — particularly for blended families, unmarried partners, business interests, and dependants you supported informally.

At what age should I write a will?

As soon as you have dependants, significant assets, a business, or specific wishes about who should receive what. For most working adults, that means “as soon as possible.” A simple, valid will today is far better than a perfect will you never write.

Can I write my own will?

Yes — a handwritten or template-based will can be valid if it meets local legal requirements (typically including being in writing, signed, and witnessed). For anything involving minor children, business interests, multiple properties, or cross-border assets, professional drafting is strongly recommended.

How often should I update my will?

Review it every one to two years, and update it after any major life event — marriage, divorce, birth, death of a beneficiary or executor, significant asset changes, or relocation.

What is the difference between a will and a trust?

A will takes effect after your death and is validated through probate. A trust can take effect during your lifetime, avoid probate, provide privacy, and give you ongoing control over how assets are used. Many estates use both together. See Serrari’s wealth management, allocation and distribution for more on how trusts fit in.

Who should I choose as my executor?

Someone trustworthy, organised, and financially literate — often a close family member or trusted friend. For complex estates, consider a professional executor (lawyer, accountant, or trust company), or at least a co-executor pairing a family member with a professional.

Does a will reduce taxes on my estate?

A well-drafted will, combined with tools like life insurance, trusts, and thoughtful ownership structuring, can reduce unnecessary taxes and costs. Serrari Advisory can coordinate with qualified tax and legal advisors to design an efficient structure for your situation.

Stay Connected, Keep Growing

Your financial future is not something you wait for — it is something you build. The real question is: when do you begin?

Move beyond simply staying informed. Navigate the markets with clarity — track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with the curated Wealth Builder Guide.

Stay connected to what truly matters. Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets — delivered through the Serrari Newsletter on the Serrari Group homepage.

Growth opens doors. Advance your career through professional programs on Serrari Ed, including ACCA prep courses and the Financial Literacy special offer — designed to move you forward with confidence.

See where money is flowing — clearly and in real time. Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving crypto and stablecoin landscape — all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}