The two-year Treasury yield is one of the most important signals for expected Federal Reserve policy. When the two-year yield rises sharply, it usually means investors are pricing higher short-term rates or a longer period of restrictive policy. On 13 July, the two-year Treasury yield moved as high as 4.276%, its highest intraday level in nearly 18 months, ahead of June CPI and Kevin Warsh testimony. For Treasury investors, this creates a split outcome: existing short-duration bond holders may face price pressure, while investors with maturing Treasury bills, money market cash or expiring CDs may be able to reinvest at more attractive yields.

Key Overview

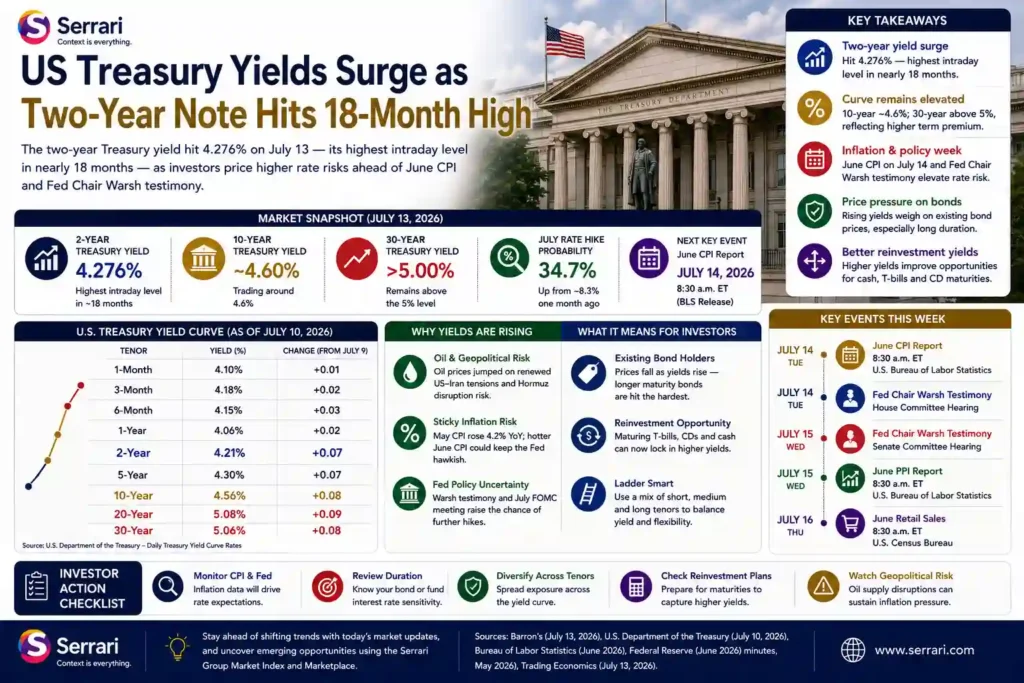

- The two-year Treasury yield rose as high as 4.276% on 13 July, its highest intraday level in nearly 18 months.

- The 10-year Treasury yield traded around 4.6%, while the 30-year Treasury yield remained above 5%.

- Barron’s reported the probability of a July rate increase near 34.7%, up from about 8.3% one month earlier.

- The official 10 July Treasury curve showed the one-year at 4.06%, two-year at 4.21%, five-year at 4.30%, 10-year at 4.56%, 20-year at 5.08% and 30-year at 5.06%.

- BLS is scheduled to publish June CPI on 14 July at 8:30 a.m. ET.

- Rising yields pressure existing bond prices but can improve reinvestment opportunities for investors with maturing cash.

US Treasury Yields Surge as Two-Year Note Hits 18-Month High

Two-Year Yield Becomes the Policy Signal

The two-year Treasury yield is the cleanest part of the curve for reading Federal Reserve expectations. Barron’s reported that investors pushed the two-year yield to 4.276%, its highest level in almost 18 months, as the market priced a greater chance that the Fed could raise rates again under the Barron’s two-year Treasury yield report.

That matters because the two-year sits close enough to Fed policy expectations to respond quickly to inflation, jobs data and central-bank language. A move higher does not only affect professional bond desks. It feeds into money market yields, Treasury ladders, CD competition, floating-rate debt and short-duration bond funds.

Official Curve Was Already Elevated

The official Treasury curve already showed pressure before the 13 July intraday move. The U.S. Treasury’s 10 July daily curve listed the one-year at 4.06%, the two-year at 4.21%, the five-year at 4.30%, the 10-year at 4.56%, the 20-year at 5.08% and the 30-year at 5.06% under the US Treasury daily rates table.

The shape matters. The short end is now high enough to compete with cash and deposits, while the long end above 5% shows investors still demand a premium for long-duration government exposure. This is a yield curve that rewards selectivity, not passive extension.

CPI Is the Next Test

The next catalyst is June CPI. The Bureau of Labor Statistics schedule lists the Consumer Price Index for June 2026 for Tuesday, 14 July at 8:30 a.m. Eastern under the BLS July 2026 release calendar.

The inflation context remains sensitive. BLS said the all-items CPI rose 4.2% over the year ended May 2026, the largest 12-month increase since April 2023, under the BLS May inflation summary. A hotter June print could push short yields higher. A cooler print could reduce the pressure, but not necessarily erase the repricing already visible in the two-year note.

Warsh Testimony Adds Policy Risk

Kevin Warsh’s testimony adds a second fixed-income catalyst. The Federal Reserve says Warsh took office as Chair of the Board of Governors on 22 May 2026 and also serves as Chair of the FOMC under the Federal Reserve Kevin Warsh biography.

Barron’s reported that Warsh is scheduled to address the House on Tuesday and the Senate on Wednesday, the same week CPI and PPI arrive. That sequencing matters for bond investors because the inflation data and Warsh’s interpretation of it could shape expectations for the 28–29 July FOMC meeting.

Existing Bond Holders Face Price Pressure

The Treasury bond selloff is negative for existing holders because bond prices move inversely to yields. When yields rise, the market value of older bonds with lower coupons generally falls. The effect is strongest for longer-duration bonds and bond funds because their cash flows sit further in the future.

That is why a two-year yield move matters even for conservative investors. A short-duration Treasury fund may have less price sensitivity than a long-bond fund, but it is not immune. Investors using Treasury funds instead of directly held bills should check duration, maturity profile and whether the fund can absorb further yield shocks.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Reinvestment Becomes More Attractive

The same move creates an opportunity for investors with cash, maturing Treasury bills or short bond ladders. Higher yields mean new money can be reinvested at better rates than were available earlier in the year.

This is the positive side of the selloff. Existing holders may feel price pressure, but investors who have kept maturities short may benefit. A laddered Treasury strategy can use this by allowing portions of the portfolio to mature regularly and roll into higher-yielding securities if rates keep rising.

The Long End Still Carries Duration Risk

The long end should not be ignored. The official Treasury curve showed the 20-year at 5.08% and the 30-year at 5.06% on 10 July. A 30-year yield above 5% can look attractive for income, but it carries heavy duration risk.

Long Treasuries can rise sharply in price if yields fall, but they can also fall meaningfully if inflation or term premium keeps pushing yields higher. For investors deciding between cash, two-year notes and 30-year bonds, the key question is whether they want income certainty, price stability or capital-gain optionality.

Cash and Deposits Stay Competitive

Short Treasury yields also affect money market funds and bank deposits. When the two-year rises, banks, brokers and cash funds may face more pressure to keep yields competitive. This matters for savers comparing CDs, high-yield savings accounts, Treasury bills and short-duration bond funds.

The decision is not simply “cash versus bonds.” It is about matching liquidity needs to maturity risk. Emergency funds may belong in liquid cash or money market products. Planned future expenses may fit Treasury bills or short notes. Longer-term portfolios can take duration, but only if investors can tolerate price volatility.

What Investors Should Watch

The first number to watch is June CPI. If inflation runs hotter than expected, the short end could reprice again. The second is Warsh’s testimony, especially whether he validates the market’s rate-hike pricing or pushes back against it.

The third is the PPI release on 15 July. Producer-price pressure can influence inflation expectations and corporate margins. The fourth is the FOMC meeting on 28–29 July, where investors will look for whether the Fed treats the yield surge as justified by inflation risk or as an overreaction.

Conclusion

US Treasury Yields have moved back to the centre of fixed-income decision-making. The two-year note’s rise to an 18-month high shows that investors are taking the possibility of another Fed rate increase seriously before June CPI and Warsh testimony.

For investors, the message is two-sided. Existing Treasury holders face price pressure as yields rise. But investors with maturing cash, short ladders or money market balances may get better reinvestment opportunities. The key is not to treat higher yields as uniformly good or bad. They are good for new money and challenging for existing duration.

FAQs

1. Why did US Treasury yields surge?

US Treasury yields surged because investors increased the probability of another Federal Reserve rate increase ahead of June CPI and Kevin Warsh’s congressional testimony. The two-year Treasury yield, which is especially sensitive to Fed policy expectations, rose as high as 4.276% on 13 July, its highest level in nearly 18 months.

2. Why does the two-year Treasury yield matter?

The two-year Treasury yield matters because it is closely tied to expected Federal Reserve policy over the next several meetings. When the two-year yield rises, it suggests markets expect higher short-term rates or a longer period of tight policy. It also affects Treasury ladders, short-duration bond funds, money market competition and reinvestment decisions.

3. What happens to bond prices when yields rise?

When yields rise, existing bond prices usually fall. This happens because older bonds with lower coupons become less attractive compared with newly issued securities offering higher yields. The price impact is larger for longer-duration bonds, which is why Treasury duration risk matters when the 10-year and 30-year yields move higher.

4. Are higher Treasury yields good for investors?

Higher Treasury yields are good for investors putting new money to work because they can earn more income on new purchases. But they are negative for existing bond holders if prices fall. The effect depends on whether the investor is reinvesting cash, holding bonds to maturity, or marking a bond fund to market.

5. What should Treasury investors watch next?

Treasury investors should watch June CPI, Warsh’s House and Senate testimony, the June PPI report, Treasury auction demand and the 28–29 July FOMC meeting. The key question is whether inflation data supports the market’s rate-hike pricing or gives the Fed room to stay on hold.

Sources: US Treasury Daily Rate, Barron’s Report, BLS July, Federal Reserve, TreasuryDirect Auction

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}