Kenya residential property prices increased 4.8% year-on-year in the first quarter of 2026, according to the KNBS House Price Index. The Kenya real estate market continued to expand, although growth varied across property types. Strong demand for standalone homes drove overall property price growth, while apartment prices declined in parts of Nairobi, reflecting changing housing demand and evolving Kenya property trends.

Key Overview

- Property prices rose 4.8% year-on-year.

- KNBS RPPI reached 118.4.

- Quarterly growth was 0.6%.

- Standalone homes gained 8.5%.

- Nairobi apartment prices declined.

- Regional apartment prices increased.

- Mortgage values eased in 2024.

- Housing demand favoured detached homes.

Kenya Residential Property Prices Rise 4.8% as Standalone Homes Outperform Apartments

Kenya residential property prices continued their upward trend during the first quarter of 2026, with the latest KNBS data showing that the House Price Index rose 4.8% year-on-year. While the broader Kenya real estate market remained resilient, performance differed significantly between standalone houses and apartments, highlighting changing buyer preferences and varying supply conditions across the country.

The latest figures indicate that detached homes continued to command strong demand, while apartment prices softened in several parts of Nairobi, creating a two-speed residential property market.

KNBS House Price Index Shows Continued Growth

According to the Kenya National Bureau of Statistics (KNBS), the Residential Property Price Index (RPPI) increased from 113.0 in the first quarter of 2025 to 118.4 during the same period in 2026.

Compared with the fourth quarter of 2025, the index recorded a modest quarterly increase of 0.6%, indicating that although annual price growth remained positive, momentum slowed slightly at the start of the year.

The figures demonstrate that Kenya’s residential market continues to expand despite broader economic pressures affecting household finances and borrowing costs.

Standalone Houses Lead Property Price Growth

The strongest contributor to overall property price growth was the standalone housing segment.

The index for detached homes climbed from 123.2 in the first quarter of 2025 to 133.6 in the first quarter of 2026, representing an annual increase of 8.5%.

The robust performance reflects continued demand for larger homes, coupled with relatively limited supply. Industry experts note that standalone developments require larger parcels of land and significantly higher development costs, limiting the number of new projects entering the market.

This imbalance between demand and supply continues to support higher property values.

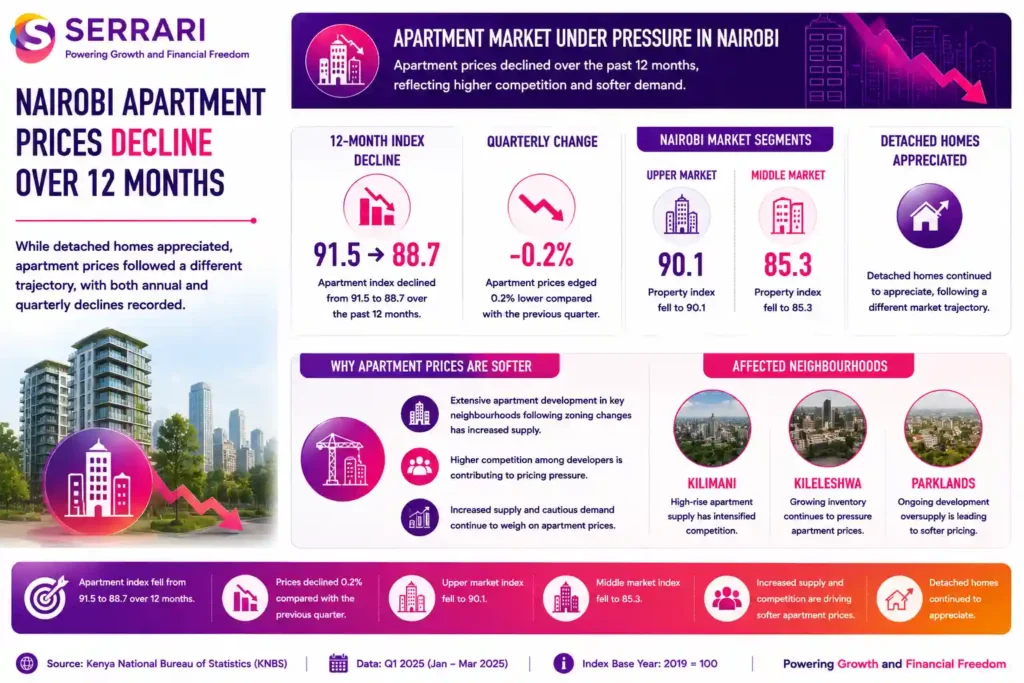

Nairobi Apartment Market Continues to Adjust

While detached homes appreciated, apartment prices followed a different trajectory.

The apartment index declined from 91.5 to 88.7 over the twelve-month period, while prices also edged 0.2% lower compared with the previous quarter.

Within Nairobi, the declines were most evident in the Upper and Middle market segments, where property indices fell to 90.1 and 85.3, respectively.

Neighbourhoods such as Kilimani, Kileleshwa and Parklands, which have experienced extensive apartment development following zoning changes, continue to experience increased competition among developers, contributing to softer pricing.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Regional Markets Continue to Perform Better

Outside Nairobi, apartment prices continued to strengthen.

KNBS data shows apartment indices rose to 106.9 across regions beyond the capital, while several other Nairobi locations also recorded price increases.

Overall, apartment prices outside Nairobi increased by 7.5% year-on-year, suggesting that the current correction remains largely concentrated within the capital city’s oversupplied apartment market.

Growing urban centres across Kenya continue attracting residential investment as infrastructure improves and population growth supports housing demand.

Lower Apartment Prices Influence Mortgage Market

The moderation in apartment prices has also affected Kenya’s mortgage market.

According to data from the Central Bank of Kenya (CBK), the average mortgage size declined to approximately KSh9 million during 2024 from KSh9.4 million the previous year, marking the first decline in seven years.

Despite the lower average mortgage value, the number of active mortgage accounts increased by 756, reaching 30,016.

The combination suggests that more affordable apartment prices may be encouraging first-time homebuyers to enter the market even as overall housing affordability remains challenging.

Buyer Preferences Continue Shifting

Consumer preferences continue favouring larger residential properties.

A KNBS survey found that 63.1% of aspiring homeowners would prefer purchasing or building a bungalow if given the opportunity. Around 23% preferred maisonettes, while only 9.5% selected apartments as their preferred housing option.

These preferences help explain the stronger performance of standalone houses despite generally higher purchase prices.

Developers may increasingly need to balance growing demand for detached homes with land availability and construction costs.

Real Estate Investment Outlook

The latest Kenya property trends highlight a market increasingly segmented by housing type.

Standalone houses continue benefiting from structural supply shortages and strong demand, while apartments face pricing pressure in areas experiencing significant new supply.

For investors, the data suggests that location, property type and local market dynamics remain critical factors when evaluating opportunities within the Kenya real estate market.

As infrastructure development continues and urban expansion spreads beyond Nairobi, regional residential markets may offer increasing opportunities for long-term real estate investment.

Conclusion

The latest KNBS House Price Index shows that Kenya residential property prices remain on a positive growth trajectory, rising 4.8% during the first quarter of 2026. However, the market is becoming increasingly divided, with standalone homes recording strong appreciation while apartment prices soften in parts of Nairobi. As housing demand continues evolving alongside changing buyer preferences, property developers and investors will need to adapt to an increasingly differentiated residential market.

FAQs

Why did Kenya residential property prices increase in Q1 2026?

Kenya residential property prices rose mainly because of strong demand for standalone homes, which experienced limited supply despite growing buyer interest. Urbanisation, infrastructure improvements and long-term investment demand also continued supporting overall price growth across the residential market.

Why are apartment prices falling in some parts of Nairobi?

Apartment prices have declined in several Nairobi neighbourhoods due to increased supply following years of rapid construction. Areas such as Kilimani, Kileleshwa and Parklands have seen significant apartment development, creating greater competition among sellers and moderating price growth despite continued housing demand.

What does the KNBS House Price Index measure?

The KNBS House Price Index measures changes in residential property prices across selected housing segments in Kenya. It tracks movements in both standalone houses and apartments, helping investors, policymakers and market participants understand trends within the country’s residential property market over time.

What do the latest property trends mean for real estate investors?

The latest Kenya property trends suggest investors should carefully consider both property type and location before investing. Standalone homes continue delivering stronger capital appreciation due to limited supply, while apartment markets vary significantly depending on regional demand and the level of new housing development.

Sources: KNBS, Eastleigh Voice, Mjengo Hub

Your financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}