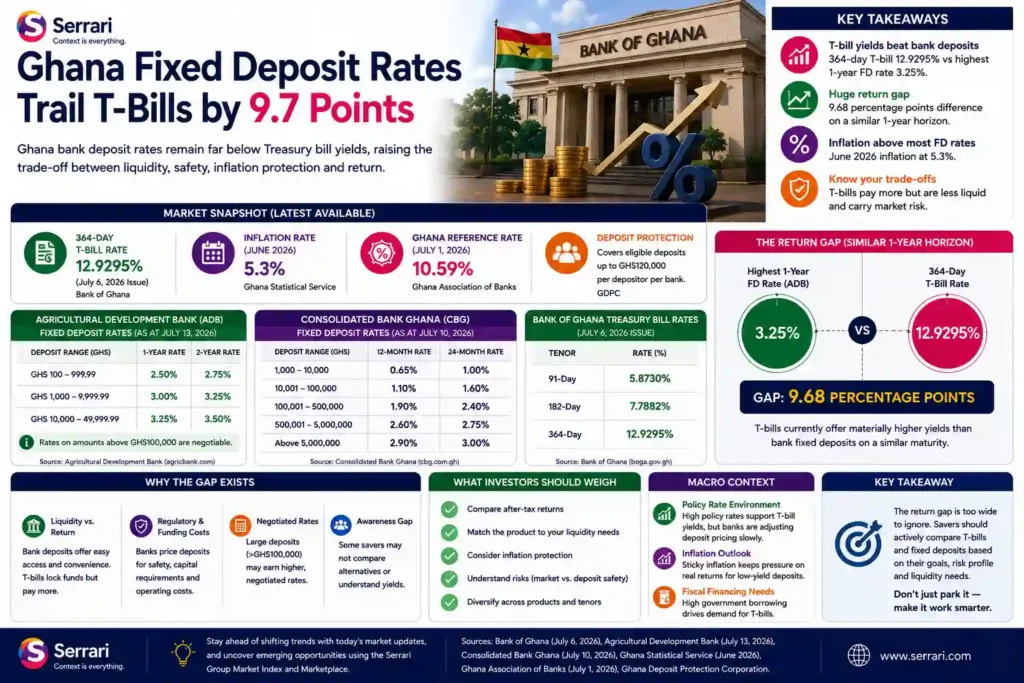

Ghana Treasury bill rates are currently far above the published fixed-deposit rates at selected banks, making the cedi cash-allocation decision more complicated. Bank of Ghana’s latest table shows the 364-day Treasury bill at 12.9295%, while ADB’s highest published one-year retail fixed-deposit rate below GHS50,000 is 3.25%. CBG’s highest published 12-month fixed-deposit rate is 2.90% for balances above GHS5 million. This does not mean Treasury bills are automatically better for every investor, because deposits and government securities differ in liquidity, protection, early-withdrawal treatment, taxation and risk structure. But the size of the gap forces savers to ask why they are accepting much lower bank deposit rates.

Key Overview

- ADB’s one-year fixed deposit rates range from 2.50% to 3.25% for deposits below GHS50,000.

- ADB says rates on amounts above GHS100,000 are negotiable.

- CBG’s 12-month fixed deposit rates range from 0.65% for GHS1,000–10,000 to 2.90% for balances above GHS5 million.

- Bank of Ghana’s latest Treasury bill table shows the 91-day bill at 5.8730%, the 182-day bill at 7.7882% and the 364-day bill at 12.9295%.

- Ghana’s June 2026 inflation rate stands at 5.3%, according to Ghana Statistical Service.

- The Ghana Reference Rate for July 1, 2026 is 10.59%, according to the Ghana Association of Banks.

Ghana Fixed Deposit Rates Trail T-Bills by 9.7 Points

ADB’s Published Rates Show the Gap

Agricultural Development Bank’s current-rates page shows fixed-deposit rates as of July 13, 2026. For deposits between GHS100 and GHS999.99, the one-year rate is 2.50%. For GHS1,000 to GHS9,999.99, it rises to 3.00%. For GHS10,000 to GHS49,999.99, the one-year rate is 3.25% under the ADB Ghana fixed deposit table. (agricbank.com)

Those rates are materially below Ghana’s Treasury bill curve. A depositor comparing ADB’s highest published one-year retail rate of 3.25% with the latest 364-day Treasury bill interest rate of 12.9295% is looking at a gap of 9.68 percentage points. That is too wide to ignore.

CBG Rates Are Even Lower

Consolidated Bank Ghana’s latest available banking-rate table, dated July 10, 2026, shows even lower 12-month fixed-deposit pricing. Its 12-month rate is 0.65% for GHS1,000 to GHS10,000, 1.90% for GHS100,001 to GHS500,000, and 2.90% for balances above GHS5 million. The maximum published 24-month rate is 3.00% under the CBG fixed deposit rates table. (CBG)

This matters because larger balances do not automatically close the gap in the published tables. Even at more than GHS5 million, CBG’s listed 12-month rate remains far below the latest 364-day Treasury bill yield.

Treasury Bills Offer a Sharper Benchmark

Bank of Ghana’s latest Treasury bill rates show the 91-day bill at 5.8730%, the 182-day bill at 7.7882% and the 364-day bill at 12.9295% for the July 6, 2026 issue. These rates create the benchmark against which Ghana savings interest rates should be compared under the Bank of Ghana Treasury bill rates. (Bureau of Ghanaian Affairs)

For investors, the key point is not simply that T-bills pay more. It is that the gap is largest where the maturities are closest: one-year deposits versus 364-day Treasury bills. That makes the comparison relevant for savers who can lock money away for roughly one year.

Inflation Raises the Real-Return Question

Ghana inflation 2026 adds another layer. Ghana Statistical Service shows June 2026 inflation at 5.3%, up 1.6 percentage points from May. That means ADB’s published one-year deposit rates below GHS50,000 sit below current inflation, while the latest 364-day Treasury bill yield sits above it under the Ghana Statistical Service inflation page. (Ghana Statistical Service)

This should not be turned into a simplistic real-return claim, because proper real returns depend on compounding, taxation and holding period. Still, the comparison is useful: low single-digit deposit rates offer limited inflation protection when consumer prices are rising faster.

Why Would Depositors Accept Lower Rates?

There are several possible reasons depositors may still accept fixed deposits. Some may value the simplicity of dealing with their bank. Others may need a product linked to a loan, overdraft, business relationship or cash-management arrangement. Some may not know the current Treasury bill rate, while others may prefer a bank deposit because of operational convenience.

There is also the negotiation factor. ADB explicitly says rates on amounts above GHS100,000 are negotiable. That means the published table may not reflect what large corporate, institutional or high-net-worth clients can secure privately.

Context is everything. Stay ahead of shifting trends with today’s market updates, and uncover emerging opportunities using the Serrari Group Market Index and Marketplace. Then, take control of your own financial future by exploring our Money & Life Reset Transformation Blueprint ™ to build stronger habits, create better systems, and design a path toward lasting wealth.

Deposit Protection Still Matters

Ghana deposit protection also shapes the decision. The Ghana Deposit Protection Corporation says the scheme was established under the Ghana Deposit Protection Act to protect small depositors from loss when an insured event occurs at a member institution under the Ghana Deposit Protection Corporation overview. (gdpc.gov.gh)

This does not mean every cedi is protected without limit, and investors should confirm current coverage rules before relying on protection. But it explains why some savers may value bank deposits differently from government securities, especially where cash access and bank relationships matter.

Reference Rate Highlights a Pricing Puzzle

The Ghana Association of Banks says the Ghana Reference Rate effective July 1, 2026 is 10.59%. The rate is used as a benchmark for bank lending, not as a deposit-rate promise. Still, it highlights a pricing puzzle: lending benchmarks are in double digits while many published fixed-deposit rates remain in low single digits under the Ghana Association of Banks reference rate. (gab.com.gh)

That spread is one reason savers should shop around, negotiate and compare alternatives before committing funds. It also explains why businesses and diaspora investors should treat idle cedi cash as an allocation decision, not just an account balance.

Fixed Deposits Are Not Treasury Bills

The yield difference should not be described as a guaranteed excess return. Treasury bills and fixed deposits differ in issuer, liquidity, access, early-withdrawal treatment, risk structure and possibly tax treatment. A fixed deposit may offer predictable bank-account administration, while a Treasury bill exposes the investor to government-security mechanics and reinvestment timing.

The better investor question is: what is the money for? Emergency cash may need liquidity. Working capital may need certainty and quick access. Longer-term cedi savings may justify comparing fixed deposits, Treasury bills, money market funds and negotiated bank placements.

What Investors Should Watch

Investors should watch whether banks update published deposit rates in response to Treasury bill yields and the Ghana Reference Rate. They should also monitor inflation, because a higher inflation print makes low fixed-deposit rates less attractive in purchasing-power terms.

The other key signal is negotiation. If large deposits are negotiable, the published tables may understate what stronger clients can achieve. Retail investors, however, must work with the published rates unless their bank offers a better negotiated deal.

Conclusion

Ghana Fixed Deposit Rates are trailing Treasury bill yields by a wide margin. ADB’s highest published one-year retail fixed-deposit rate below GHS50,000 is 3.25%, while the latest 364-day Treasury bill rate is 12.9295%. That creates a 9.68-percentage-point gap that savers should not overlook.

The answer is not automatically to abandon fixed deposits. Deposits and Treasury bills serve different needs. But for retail investors, businesses and diaspora clients holding cedi cash, the current gap demands a deliberate comparison of return, liquidity, protection, tax treatment, negotiation and inflation-adjusted purchasing power.

FAQs

1. What are Ghana Fixed Deposit Rates right now?

Published Ghana Fixed Deposit Rates vary by bank, amount and tenor. ADB’s current table shows one-year rates of 2.50% to 3.25% for deposits below GHS50,000, while CBG’s latest table shows 12-month rates from 0.65% to 2.90% depending on deposit size. Larger balances may attract negotiated rates, especially where a bank explicitly says rates are negotiable.

2. How do Ghana Treasury bill rates compare?

Ghana Treasury bill rates are much higher than the published fixed-deposit rates in the selected bank tables. Bank of Ghana’s latest Treasury bill table shows 5.8730% for the 91-day bill, 7.7882% for the 182-day bill and 12.9295% for the 364-day bill. The 364-day bill is 9.68 percentage points above ADB’s highest listed one-year retail deposit rate.

3. Why would someone still choose a fixed deposit?

Someone may choose a fixed deposit because it is simple, familiar and tied to an existing banking relationship. Fixed deposits may also suit customers who want predictable bank administration, loan collateral support or negotiated terms. However, investors should compare rates carefully and ask whether the convenience justifies the lower published return.

4. Are Treasury bills always better than fixed deposits?

No. Treasury bills and fixed deposits are different products. Treasury bills may offer higher yields, but they differ in liquidity, issuer, holding process, reinvestment timing, tax treatment and risk structure. Fixed deposits may be easier for some bank clients to manage, but they may also have early-withdrawal restrictions and lower published rates.

5. How does inflation affect Ghana deposit returns?

Inflation affects deposit returns by reducing purchasing power. If a fixed deposit pays 3.25% while inflation is 5.3%, the saver’s purchasing power may still decline before considering compounding or taxes. This does not replace a full real-return calculation, but it shows why investors should compare nominal rates with inflation.

Sources: ADB Ghana, CBG, Bank of Ghana, Ghana Statistical Service, GDPC Amendment Bill, Stanbic Bank Ghana

Your Financial future isn’t something you wait for—it’s something you build.

The real question is: when do you begin?

Move beyond simply staying informed.

Navigate the markets with clarity—track trends through the Serrari Group Market Index, uncover opportunities in the Serrari Marketplace, and build practical knowledge with our Curated Wealth Builder Platform.

Stay connected to what truly matters.

Get daily insights on macro trends and financial movements across Kenya, Africa, and global markets—delivered through the Serrari Newsletter.

Growth opens doors.

Advance your career through professional programs including ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟—designed to move you forward with confidence.

See where money is flowing—clearly and in real time.

Track Money Market Funds, Treasury Bills, Treasury Bonds, Green Bonds, and Fixed Deposits, alongside global and African indexes, key economic indicators, and the evolving Crypto and stablecoin landscape—all within Serrari’s Market Index.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}