In the pursuit of financial stability and long-term prosperity, the principles of earning, spending, and saving play crucial roles. Renowned investor Warren Buffett once wisely advised, “Do not save what is left after spending; instead spend what is left after saving ‘’. This statement resonates strongly with individuals in their mid-20s and early 30s who are seeking to establish a solid foundation for personal wealth management. This article aims to provide valuable insights, tips, and strategies for effectively managing your personal finances and achieving financial success.

Importance of Personal Wealth Management

Effective wealth management allows individuals to build a safety net and protect themselves against unforeseen events such as medical emergencies, job loss, or economic downturns. By saving and investing wisely, individuals can create a financial cushion that provides stability and peace of mind. Managing personal wealth ensures that individuals can maintain their desired lifestyle in the present and the future. By budgeting, tracking expenses, and making informed financial decisions, individuals can enjoy their desired standard of living without compromising their financial well-being. Wealth management also encompasses financial planning for the future beyond one’s lifetime. It involves creating an estate plan, including wills, trusts, and beneficiary designations, to ensure a smooth transfer of assets and minimize tax implications. Through effective legacy planning, individuals can leave a lasting impact on their loved ones and charitable causes.

Budgeting and the 50/20/30 rule

Budgeting is an essential part of managing your money effectively and ensuring financial stability. It involves creating a plan that outlines how you will allocate your income, track your expenses, and prioritize your savings. By adopting a budgeting mindset, you gain control over your financial situation and make informed decisions that align with your goals and values. Budgeting provides a clear roadmap for managing your finances, enabling you to navigate through the complexities of personal financial management with confidence and purpose.

The 50/30/20 rule is a popular guideline for budgeting that can help you manage your finances in a balanced way. It suggests dividing your after-tax income into three categories:

1. Essential Expenses (50%): Allocate around 50% of your income to cover essential expenses such as housing, utilities, groceries, transportation, and minimum debt payments. These are the necessary expenses you need to maintain your basic needs nor wants and a stable lifestyle.

2. Discretionary Spending (30%): Allocate about 30% of your income to discretionary spending, which includes non-essential expenses like dining out, entertainment, shopping, and hobbies. This category allows you to enjoy life’s extras and have some flexibility in your spending.

3. Savings and Debt Repayment (20%): Reserve approximately 20% of your income for savings, investments, and debt repayment. This portion helps you build an emergency fund, save for future goals, invest for your long-term financial security, and pay off any outstanding debts faster.

By following this rule, you ensure that your essential needs are covered, have room for enjoyable extras, and prioritize saving and debt reduction. It provides a simple framework to allocate your income effectively, achieve financial balance, and work towards your financial goals. Remember that the percentages can be adjusted based on your individual circumstances and priorities.

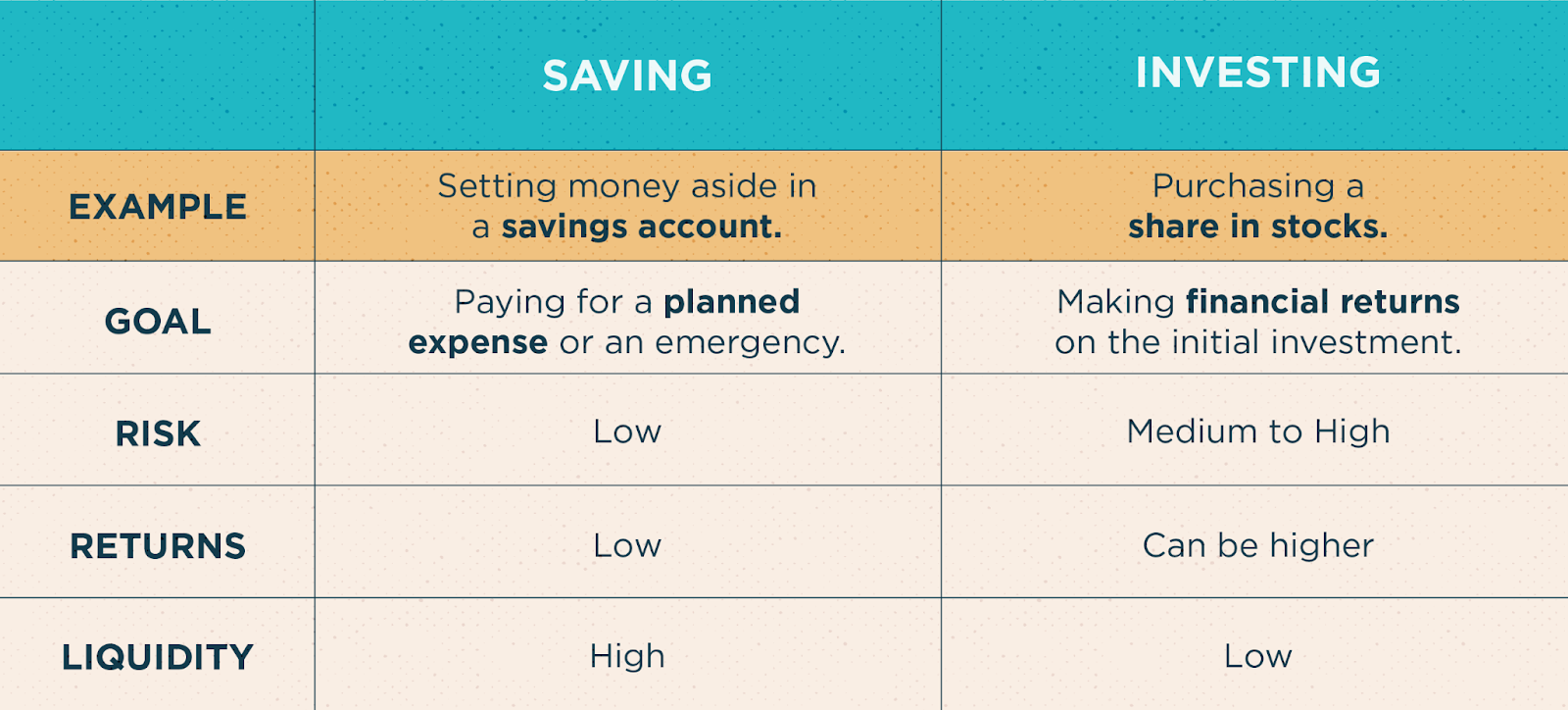

Savings vs Investing: Understanding the Difference

Saving vs Investing

When it comes to managing your finances, it’s important to differentiate between savings and investing. Savings serve as a safety net for short-term goals and emergencies, providing readily accessible funds to cover unexpected expenses. Held in low-risk accounts, savings prioritize capital preservation rather than substantial growth, with relatively modest returns. On the other hand, investing is focused on long-term goals and potentially higher returns. It involves allocating money across different asset classes like stocks, bonds, and real estate, with the aim of generating growth over an extended period. Investing carries varying levels of risk, and diversification is key to mitigating potential losses. While savings offer liquidity and stability, investing allows for potential compounding returns and is more suited for long-term goals. By understanding the distinctions between savings and investing, you can develop a financial strategy that balances short-term needs and long-term growth, aligning with your unique financial objectives.

Sources:https://mint.intuit.com/blog/investments/saving-vs-investing-3485/

Should You Invest or Save Your Money?

Deciding whether to invest or save your money depends on various factors, including your financial goals, time horizon, risk tolerance, and current financial situation. Saving involves setting aside money in safe and easily accessible accounts, providing stability and low-risk preservation of capital. It is suitable for short-term goals and emergencies. On the other hand, investing entails putting money into assets with the aim of generating long-term returns. While investments offer higher potential returns, they also carry greater risk. Investing is suitable for long-term goals such as retirement or wealth accumulation. It’s important to consider factors like time horizon, risk tolerance, financial goals, diversification, and the establishment of an emergency fund. Ultimately, a balanced approach that combines saving and investing is often recommended, and consulting a financial advisor can provide personalized guidance based on your unique circumstances.

In conclusion

personal wealth management plays a critical role in achieving financial stability and long-term prosperity. By effectively managing your finances, you can build a safety net, maintain your desired lifestyle, and plan for the future. Budgeting and the 50/20/30 rule provide a structured approach to allocate your income wisely, ensuring that essential needs are met, discretionary spending is enjoyed, and savings and debt reduction are prioritized. Understanding the distinction between saving and investing is crucial. Savings provide liquidity and stability for short-term needs, while investing offers the potential for long-term growth and higher returns. Striking a balance between saving and investing, based on your financial goals, time horizon, and risk tolerance, can help you make informed decisions and maximize your financial well-being.

Seeking guidance from a financial advisor can provide personalized advice tailored to your specific circumstances, helping you navigate the complex world of personal wealth management with confidence and clarity. Remember, by taking proactive steps toward effective personal wealth management, you pave the way for a secure and prosperous financial future.

Article, Financial and News Disclaimer

The Value of a Financial Advisor

While this article offers valuable insights, it is essential to recognize that personal finance can be highly complex and unique to each individual. A financial advisor provides professional expertise and personalized guidance to help you make well-informed decisions tailored to your specific circumstances and goals.

Beyond offering knowledge, a financial advisor serves as a trusted partner to help you stay disciplined, avoid common pitfalls, and remain focused on your long-term objectives. Their perspective and experience can complement your own efforts, enhancing your financial well-being and ensuring a more confident approach to managing your finances.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Readers are encouraged to consult a licensed financial advisor to obtain guidance specific to their financial situation.

Article and News Disclaimer

The information provided on www.serrarigroup.com is for general informational purposes only. While we strive to keep the information up to date and accurate, we make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the website or the information, products, services, or related graphics contained on the website for any purpose. Any reliance you place on such information is therefore strictly at your own risk.

www.serrarigroup.com is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information on the website is provided on an as-is basis, with no guarantee of completeness, accuracy, timeliness, or of the results obtained from the use of this information, and without warranty of any kind, express or implied, including but not limited to warranties of performance, merchantability, and fitness for a particular purpose.

In no event will www.serrarigroup.com be liable to you or anyone else for any decision made or action taken in reliance on the information provided on the website or for any consequential, special, or similar damages, even if advised of the possibility of such damages.

The articles, news, and information presented on www.serrarigroup.com reflect the opinions of the respective authors and contributors and do not necessarily represent the views of the website or its management. Any views or opinions expressed are solely those of the individual authors and do not represent the website's views or opinions as a whole.

The content on www.serrarigroup.com may include links to external websites, which are provided for convenience and informational purposes only. We have no control over the nature, content, and availability of those sites. The inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them.

Every effort is made to keep the website up and running smoothly. However, www.serrarigroup.com takes no responsibility for, and will not be liable for, the website being temporarily unavailable due to technical issues beyond our control.

Please note that laws, regulations, and information can change rapidly, and we advise you to conduct further research and seek professional advice when necessary.

By using www.serrarigroup.com, you agree to this disclaimer and its terms. If you do not agree with this disclaimer, please do not use the website.

www.serrarigroup.com, reserves the right to update, modify, or remove any part of this disclaimer without prior notice. It is your responsibility to review this disclaimer periodically for changes.

Serrari Group 2025