The U.S. dollar tumbled to its lowest levels in over two months against major currencies on Tuesday, as investors positioned for the Federal Reserve’s first interest rate cut of 2025 scheduled for Wednesday’s policy meeting. The dollar index fell to 97.121, marking its weakest performance since July 7, as markets priced in a 25 basis point reduction with 96% probability according to the CME FedWatch tool.

The currency decline comes amid an extraordinary period of tension between the White House and Federal Reserve, with President Trump renewing calls for “bigger” cuts in monetary policy and launching an unprecedented pressure campaign that experts warn could fundamentally undermine the central bank’s independence.

Push boundaries, reach goals, achieve more. Whether it’s ACCA, HESI A2, ATI TEAS 7, HESI EXIT, NCLEX-RN, NCLEX-PN, or Financial Literacy, we’ve got the Online course to match your ambition. Start with Serrari Ed now.

Currency Markets Signal Shifting Economic Dynamics

The dollar’s weakness rippled across global currency markets, with sterling rising 0.2% to $1.3627 – its highest level since July 8 – and the euro advancing as much as 0.3% to $1.1797, a level not seen since July 3. The Australian dollar, after initially climbing to $0.6677 (its strongest level since November 8), settled slightly lower at $0.6666.

These currency movements reflect broader shifts in global monetary policy expectations and economic fundamentals. Recent UK employment data showed continued cooling in the jobs market, with payrolls falling for a seventh consecutive month and private sector wage growth slowing to 4.7% from 4.8%. This data potentially eases concerns at the Bank of England about persistent inflation pressures, though the central bank is expected to hold rates steady this week after cutting in August.

The yen weakened 0.3% against the dollar to 146.920 ahead of the Bank of Japan’s policy meeting on Friday, where money markets expect rates to remain at 0.5%. Japan’s political landscape adds another layer of uncertainty, with the farm minister and chief government spokesperson joining the race to replace outgoing Prime Minister Shigeru Ishiba.

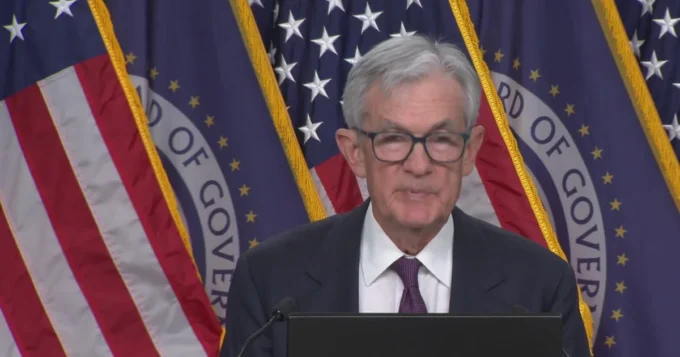

Fed Decision Carries Historical Significance

Wednesday’s Federal Open Market Committee meeting represents a pivotal moment for U.S. monetary policy, marking the Fed’s first rate cut since December 2024. The anticipated quarter-point reduction would lower the federal funds rate target range to 4.00%-4.25%, ending a period of restrictive monetary policy that has persisted through much of 2025.

The decision comes as economic data presents mixed signals. While GDP growth remains robust at above 5% nominally, the labor market shows increasing signs of stress. August employment data revealed just 22,000 jobs added, significantly below the 75,000 economists expected, with the unemployment rate rising to 4.3% from 4.2%.

Particularly concerning for policymakers has been the massive downward revision to previous employment figures, with May and June job numbers revised down by 258,000 positions. This revision suggests the labor market has been weaker than initially reported, adding urgency to calls for monetary easing.

Political Pressure Reaches Unprecedented Levels

The Fed’s deliberations occur against the backdrop of extraordinary political pressure from the Trump administration. In a recent social media post, President Trump called on Fed Chair Jerome Powell to enact more aggressive monetary easing, pointing specifically to challenges in the housing market.

This pressure campaign has taken multiple forms, including Trump’s installation of White House economic adviser Stephen Miran as a Fed governor and his attempted removal of Fed Governor Lisa Cook. Legal scholars and former Fed officials warn these actions represent the most serious challenge to central bank independence in modern history.

According to a recent CNBC survey of 29 top economists and money managers, 82% believe Trump’s actions are designed to limit or eliminate the Fed’s independence. Majorities predict these efforts will result in higher inflation (68%), increased unemployment (57%), and weaker economic growth (54%).

Historical Context and Independence Concerns

The current situation echoes troubling historical precedents. Experts point to President Nixon’s pressure on Fed Chair Arthur Burns in the early 1970s, which contributed to a decade-long inflationary cycle requiring two recessions to break. Nixon’s tactics included leaked threats to take over the Fed, ultimately leading to monetary policies that prioritized short-term political gains over long-term economic stability.

“History is full of episodes of governments that tried to ease monetary policy in exchange for a few months or a few years of lower unemployment and strong growth,” notes Joseph Gagnon, a former Fed economist. “But the trade-off is always inflation.”

The stakes extend beyond domestic policy. Fed independence is crucial for maintaining global confidence in U.S. institutions and supports the dollar’s role as the world’s reserve currency. Countries that have compromised central bank independence, from Turkey to Argentina, have experienced currency volatility, capital flight, and persistent inflation.

Build the future you deserve. Get started with our top-tier Online courses: ACCA, HESI A2, ATI TEAS 7, HESI EXIT, NCLEX-RN, NCLEX-PN, and Financial Literacy. Let Serrari Ed guide your path to success. Enroll today.

Market Implications and Investment Flows

The dollar’s weakness reflects broader shifts in global capital allocation. J.P. Morgan analysis shows that flows into U.S. equities have weakened significantly in 2025, with some months seeing outright selling by foreign investors. Non-U.S. domiciled ETFs investing in U.S. equities averaged net flows of just $5.7 billion in the first seven months of 2025, compared to $10.2 billion in the same period of 2024.

European investors, in particular, are reallocating to local assets, with European-focused ETFs receiving a record $42 billion in net flows. This rebalancing trend, following years of exceptional U.S. returns, continues to pressure the dollar.

The $7 trillion parked in money market funds represents another significant factor. These funds, accumulated during years of high interest rates, will likely seek higher-yielding alternatives as the Fed begins its cutting cycle, potentially driving investment flows toward international markets and further pressuring the dollar.

Global Economic Context and Central Bank Divergence

The Fed’s anticipated rate cut occurs within a broader context of diverging global monetary policies. While the European Central Bank and Bank of England have also been cutting rates, economic conditions vary significantly across major economies.

Global growth is expected to weaken to 2.3% in 2025, with the World Bank warning that this represents the slowest pace in 17 years outside of outright recessions. Rising trade barriers and heightened policy uncertainty contribute to this challenging outlook, with particular stress on trade-dependent regions like East Asia and Europe.

The Asia-Pacific region continues to play an increasingly important role in global currency markets. China’s economic performance remains crucial, with the yuan under pressure from both economic challenges and potential new U.S. tariffs. The People’s Bank of China continues intervening to slow yuan depreciation, but mounting challenges from the property sector collapse and trade tensions complicate these efforts.

Inflation Dynamics and Policy Dilemmas

The Fed faces a complex inflation picture that complicates rate-setting decisions. Core inflation remains at 2.9%, above the Fed’s 2% target, while average U.S. tariff rates have reached approximately 18.4% as of July 2025, contributing to price pressures.

This creates a policy dilemma: labor market weakness suggests the need for monetary easing, while inflation above target typically calls for restrictive policy. Fed Chair Powell has indicated that in such situations, policymakers would assess which mandate element is further from target and focus on whichever is in worse condition.

The Economic Policy Uncertainty Index hit a high of 243.7 in July 2025, reflecting the difficulty businesses and policymakers face in planning for the future. This elevated uncertainty itself becomes a factor in economic decision-making, potentially dampening investment and hiring even as monetary policy becomes more accommodative.

Technology and Market Structure Evolution

Currency markets are experiencing technological transformation that affects trading patterns and market efficiency. The integration of artificial intelligence and machine learning into trading platforms enables more sophisticated analysis and faster execution, while advanced platforms make foreign exchange markets increasingly accessible to individual traders.

CME Group’s upcoming FX Spot+ platform, scheduled for launch in March 2025, represents an innovative approach combining futures market liquidity with spot FX trading. This technological evolution occurs alongside fundamental shifts in global trade patterns and monetary policy frameworks.

Future Policy Trajectory and Market Expectations

Looking beyond Wednesday’s expected rate cut, market participants and economists are divided on the Fed’s likely path. Some analysts predict six consecutive rate cuts through early 2026, bringing the federal funds rate down to a range of 2.75% to 3% as the Fed searches for a neutral policy stance.

However, dissent within the Fed adds uncertainty to this outlook. Kansas City Fed President Jeff Schmid and Cleveland Fed President Beth Hammack have voiced preferences for standing pat in September, while Chicago Fed President Austan Goolsbee has expressed similar sentiments with less conviction.

The Fed’s quarterly Summary of Economic Projections, to be released alongside Wednesday’s decision, will provide crucial insight into policymakers’ longer-term rate expectations. Most analysts expect this to show targets for three rate cuts in 2025, though political pressure and economic uncertainty could alter this trajectory.

Global Financial Stability Implications

The current tensions between the White House and Federal Reserve carry implications far beyond U.S. borders. As the Atlantic Council notes, threats to Fed independence “carry real consequences” for global financial stability, given the dollar’s role as the world’s reserve currency.

International investors and central banks closely monitor U.S. monetary policy developments, as Fed decisions influence global capital flows, commodity prices, and emerging market financing conditions. A weakening of Fed credibility could prompt diversification away from dollar-denominated assets, potentially undermining decades of accumulated trust in U.S. financial institutions.

The broader question facing global markets is whether political pressures will fundamentally alter the Fed’s approach to monetary policy. As one analyst noted, “We are on a road that is going to lead to the erosion of central bank independence, and it would be incredibly costly for the long-term health of the economy for the Fed to lose the credibility that it has spent decades trying to build.”

As Wednesday’s Fed decision approaches, currency markets reflect not just expectations for monetary policy changes, but broader concerns about the institutional framework that has underpinned global financial stability for generations. The outcome will likely influence not only near-term exchange rates and investment flows, but the fundamental relationship between political power and monetary policy in the world’s largest economy.

Ready to take your career to the next level? Join our Online courses: ACCA, HESI A2, ATI TEAS 7 , HESI EXIT , NCLEX – RN and NCLEX – PN, Financial Literacy!🌟 Dive into a world of opportunities and empower yourself for success. Explore more at Serrari Ed and start your exciting journey today! ✨

Track GDP, Inflation and Central Bank rates for top African markets with Serrari’s comparator tool.

See today’s Treasury bonds and Money market funds movement across financial service providers in Kenya, using Serrari’s comparator tools.

photo source: Google

By: Montel Kamau

Serrari Financial Analyst

17th September, 2025

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}